Unwind the stimulus? What stimulus?

Should it be called a stimulus when the central bank is revisiting its disastrous policies?

Business Recorder published a relatively long editorial where they requested SBP to unwind some stimuli (emphasis mine).

The State Bank of Pakistan (SBP) Governor Dr Reza Baqir commented in a recent interview to a foreign publication that one of the two factors for higher-than-expected GDP growth in FY21 is the aggressive monetary stimulus provided by the Pakistan’s central bank which is equivalent to 5 percent of GDP and largely reliant on quantitative measures.

... And a supplementary question is for how long will the stimuli continue as SBP is still running an accommodative monetary policy?

It increasingly appears that the stimuli are not likely to be withdrawn anytime soon as the prevalent view seems to be that it may be more risky to withdraw the stimulus too soon rather than too late given the uncertainties pertaining to the Covid-19. The real test will be when the C/A starts slipping and how SBP will react to it. It’s better to unwind some stimuli gradually before a bigger crisis hits.

If the editors had identified which of the SBP stimuli they want to be unwound, this post could have been shorter. Now I will have to go through each of the stimuli to see which one can be unwound.

The below tweet from SBP shows the stimuli being harped by SBP.

Let’s go over them one by one.

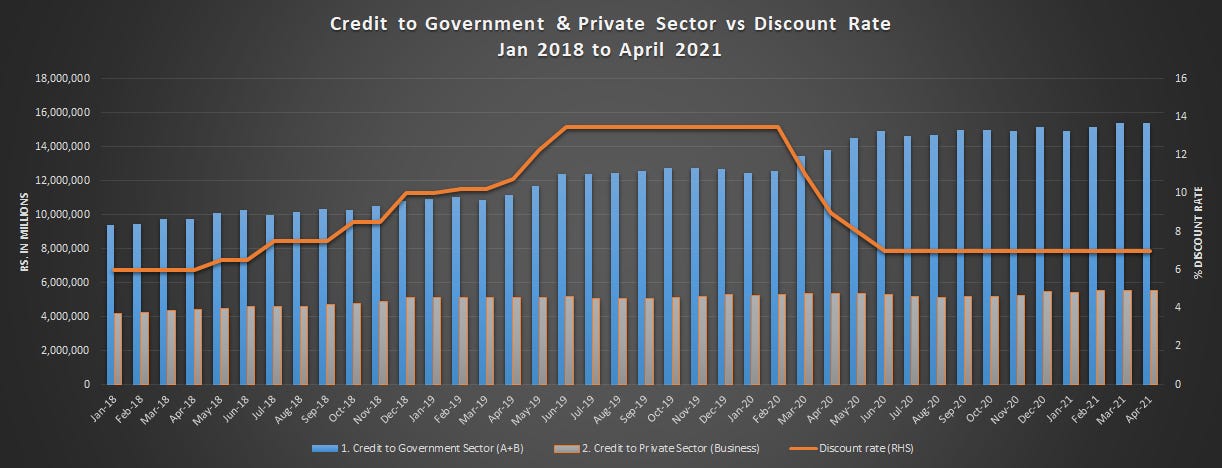

"Rapid reduction" of policy rate by 625 basis points.

Before we review this, I found it interesting that the editorial didn't consider it a rapid reduction. Au contraire, the editorial describes the move as (emphasis mine)

When the pandemic hit, stabilization economic policies in Pakistan were at full throttle. The SBP took its sweet time to react, reducing the policy rate from 13.25 percent to 7 percent after ten long weeks.

The first time I read the editorial, I had missed the slight jab but on second reading for writing this post, I noticed it and enjoyed it. What SBP considers "rapid reduction", the editorial deems it taking its sweet time to react and after ten long weeks.

For what it’s worth, I agree with the editors on this one. To begin with, I considered the high discount rate a disastrous policy.

Coming back to the argument, is the editorial asking for increasing the discount rate? If that is the case, they should be explicit about it and list their reasons.

Loan principal deferment

This facility allowed deferment of principal payments up to 12 months for the borrower. The borrower was expected to continue servicing the interest on a regular basis as per the terms of the agreement. This facility ended on Sep 30, 2020. No more deferrals are being offered after the last date. Thus, this facility has already ended. There is no need to wind it down.

Loan restructuring program

This facility allowed for the loan principal to be deferred for more than 12 months as well as relaxation in interest repayment terms. However, the term of this facility ended on March 31, 2021. Thus, there is no need to wind this down either.

I am conflicted by calling 2 and 3 as stimuli. On the one hand, I understand that this allowed borrowers to delay their outflows, which is technically an inflow. On the other hand, when a stimulus is mentioned, the perception is that cash flowed from the central bank or the government to the borrower, which didn't happen in this case. However, I will go with the former definition and consider these two facilities as stimuli.

There needs to be a bigger discussion with SBP’s marketing of the aforementioned three steps as stimuli.

Is walking back on a disastrous policy a stimulus? The rate was 6% in April 2018. Reza Baqir took it up to 13.25% to attract hot money and damaged the industry along the way.

Changing the discount rate didn’t bring down borrowing. It just made it extremely expensive to service the debt for both government and private sector. What if this ludicrously high discount rate forced the borrowers to go for the loan principal deferment and loan restructuring facilities when Covid-19 struck. First SBP made the catastrophic decision to increase the discount rate bringing hardship to local industry, and when it became clear that the policy was misguided, reduced the discount rate to the previous level and offered deferment and restructuring facilities to alleviate the suffering of the borrowers.

SBP under Reza Baqir loves to give a positive spin to everything, hence these are marketed as stimuli.¯\_(ツ_/¯

These account for 3.3% of GDP as per the chart in the SBP tweet. If we take these out, the actual stimulus was 1.7% of the GDP. Hence, SBP is claiming three times the size. ¯\_(ツ_/¯

The next two are quasi-fiscal activities and are stimuli in the true sense of the word as actual money flows from SBP to borrowers in their case.

Rozgar Scheme

This scheme provided cheap refinancing from SBP to pay salaries and wages for employees for six months. However, we don't know if it really prevented job losses

SBP is counting every salary paid as a job saved. It may be reasonable assumption for SMEs but to include employees of larger businesses in that calculation appears to be case of statistical manipulation.

[16% of the jobs saved under this facility were at SMEs.] Should the scheme be considered successful when one considers that SMEs employee 80% of the non-farm labour yet received even less than 16% of financing to pay wages of their employees?

Regardless this facility expired in September 2020.

TERF and RFCC

TERF allowed 10 year financing for BMR activity. RFCC allowed 5-year financing for setting up health care facilities. RFCC is expiring on June 30, 2021. TERF expired on March 31, 2021.

There you have it. All the stimuli that SBP provided have expired except for RFCC which isn't a significant stimulus anyway in the larger scheme of things. Which stimulus does the editorial want to be wound down?

SBP, on the contrary, is about to introduce a new quasi-fiscal stimulus for SME Financing. In addition, in my last post, I requested SBP to reduce the discount rate to 6%.

To summarize,

The majority of the incremental borrowing continues to be in refinancing which is financed by SBP at a rate less than half of the discount rate.

SBP introduced another new refinancing facility again at a rate that is less than half the discount rate. Let's not beat around the bush. The refinancing rate on this facility is 1%.

The housing finance facility, which is a subsidized facility, will be providing 5-year financing at rates ranging from 3% to 7% (a rate less than or equal to the policy rate).

Finally, SBP has gone full populist by pushing car financing which will be providing 3-year loans at 7%.

The question then becomes why do the SBP, oped writing economists and financial press continue to maintain the charade that 7% is the appropriate discount rate? There is no scientific basis for a 7% discount rate. The real rate is already negative at this level.

All the aforementioned steps taken by SBP show that SBP knows that if the country has to embark on a growth journey, the discount rate should be lower than 7%.