Refinancing galore at SBP

SBP continues to promote Quasi Fiscal Activities and Development Finance Activities despite the fact the new SBP Act prohibits SBP from engaging in such activities.

Like a broken record, I keep bringing attention to the fact that SBP's WhatsApp leaked SBP Amendment Act that was proposed by none other than SBP's own IMF-returned management and under the guidance/direction of IMF prohibits Quasi Fiscal Activities (QFAs) and Development Finance Activities(DFAs), yet SBP continues to celebrate those activities. It is as if SBP has gone populist.

If you are reading this substack for the first time, you can read the comprehensive coverage of the topic in What they didn't teach me at the business school about SBP's Magic Money Tree where I explain the relevant clauses of the SBP Amendment Act, how QFAs and DFAs are defined, why it doesn't cost SBP a penny to engage in QFAs, and while commercial banks take the risks and GoP bears the costs, it is SBP that takes all the credit.

When it comes to fiscal subsidies, the government has to arrange the resources for it, negotiate it with IMF, and get it approved in the budget from the parliament.

When it comes to quasi-fiscal subsidies, SBP has to just announce it by issuing the circular unelected technocrats wielding powers that the elected government ministers and even the prime minister can only dream of.

Deep in the throes of the Covid-19 crisis, these refinancings also provided SBP governor an opportunity to promote himself. No other central banker in the world has promoted himself as much as Reza Baqir during this crisis.

In a subsequent post SBP refinancings a success? Take my word for it, I wrote that we don't have any way to measure if these QFAs have been successful and the mere utilization of these facilities is being celebrated as a mark of success.

Thus all the credit is being taken by SBP while all the risk is borne by the commercial banks. Reminds me of my stock broker when he used to give advice to me in which stock market shares to invest "tips meri, risk aap ka". I find it amusing that SBP considers it a brilliant idea that they shifted all the risk to the commercial banks. The effect of this shift has been majority of the refinancing was provided to large and existing clients.

We also need to move beyond making the commercial banks gatekeepers of who gets the funds. Commercial banks are making most of their profits from PIBs and non-fee income by scamming consumers on bancassurance. They have no capacity or even willingness to diversify industrial base or reach out to SMEs.

Is Evidenced Based policy making only to be used when providing support to low income groups? When it comes to SBP refinancings, is mere utilization of the facility be deemed a success?

I had wondered on Twitter if this populist bent of SBP governor is because he is targeting PM position in a future election cycle. Much fun was had.

In this post, I cover two recent developments.

SME Financing

Another QFA by SBP as per Business Recorder today

SMEs likely to get Rs60bn collateral-free lending

The State Bank of Pakistan (SBP) drafted a scheme titled “refinance and credit guarantee scheme for collateral free lending to SMEs’’ to facilitate SMEs which do not have collateral to get financing from banks. The scheme involves risk sharing subsidy from the Government of Pakistan.

State Bank of Pakistan (SBP) is likely to provide refinancing of Rs 60 billion to Small and Medium Enter prises (SMEs) in three years under refinance and credit guarantee scheme for collateral-free lending, sources in Finance Ministry told Business Recorder.

In order to address this issue, SBP after extensive deliberations with the relevant stakeholders, including banks, developed a scheme titled “refinance and credit guarantee scheme for collateral free lending to SMEs.” The scheme envisages partnering with selected banks through a transparent procedure to enable them to offer collateral-free financing to SMEs.

Under the scheme, SBP will provide refinancing of around Rs. 60 billion in three years at 1% which will be used by the partner banks for extending financing to SMEs at 9%, thereby providing a spread of 8% to banks. This will encourage banks to justify their initial investment in systems and personnel.

Maximum loan size under the scheme will be of Rs 10 million. One of the attractive features of the scheme is the provision of up to 60% risk coverage by the GoP to banks on their financing to SMEs.

The total financial impact of the proposed risk sharing facility to the GoP has been worked out to the tune of Rs.25.84 billion to be provided to SBP for onward payments to banks over four years as per following details: (i) FY 2020-21, no allocation required; (ii) FY 2021-22 Rs 1.19 billion; (iii) FY 2022-23 Rs 6.24 billion; (iv) FY2023-24, Rs 11.06 billion; and (v) FY 2024-25 Rs 7.35 billion.

Let's break it down.

Zero cost money creation by SBP

As we have discussed in earlier posts, SBP creates money with a click of a button at zero cost. Assume Basheer approaches BOP for the loan. BOP asks SBP for the money. SBP creates money and lends it to BOP at 1%. BOP lends to Basheer at 9%. This is how the T-accounts will appear. The 1% SBP is charging is pure income for SBP.

Embarrassingly exorbitant spread to Commercial Banks

The commercial banks raked in the moolah by investing in PIBs and made record profits during the Covid-19 pandemic. It is absurd that they require an 8% spread to justify the initial investment in systems and personnel. It will be better to give this cheap money to the loan sharks i.e. micro-finance institutions. They already have the personnel and systems in place to rapidly deploy this money. They provide financings at double-digit interest rates due to the high cost of funds. By providing financing at 9%, they can have an immediate and noticeable impact on the growth of the SME sector.

It will be even better if some portion of refinancing is reserved for “fintech” startups i.e. allow fintech startups to provide loans to SMEs. This may result in the birth and growth of startups that can challenge the lazy incumbent rent-seeking PIB-investing commercial banks.

Loss sharing by GoP

If the 8% spread wasn't enough for commercial banks to ramp up their systems and hire/train their personnel, and to build loss reserves, the Government of Pakistan is also providing a risk-sharing facility of 40%. The total refinancing size is about Rs.60 billion. 40% translates into Rs.24 billion.

This is what I had written concerning SBP’s Rozgar scheme

It should be noted that SBP isn't taking any risk in any of the refinancing facilities. It is just creating free money and taking all the credit. The credit risk is on the books of commercial banks. If there is any risk-sharing, Federal Government is on the hook for it through fiscal measures.

Comparison with the housing subsidy

In the Naya Pakistan Housing interest rate subsidy, GoP is providing a subsidy of Rs.36 billion to subsidize the interest rate while SBP is just managing the allocation of the interest rate subsidy. Thus housing finance subsidy is a DFA. Moreover, it appeared as if the entire Rs.36 billion was allocated to the 2020-2021 budget. As per my earlier post

GoP will be making the payment. As per the SBP press release

Government of Pakistan has increased the total funding allocation to Rs36 billion on account of markup subsidy payment for financing over a period of 10 years and has assured continuity of the facility.

This Rs.36 billion would have been allocated and will be appearing in the budget of GoP 2021. Thus, when the federal government provides a subsidy, it is a fiscal activity and it appears in the budget of the government as a fiscal expense.

Needless to mention SBP can't even engage in this activity anymore as SBP is prohibited from development finance activities (DFAs) under the revised section 20 where DFAs are defined as "ANY ACTIVITY undertaken to promote any priority sector such as housing etc" as here SBP is promoting housing.

In contrast, SME collateral-free financing is a QFA as here it is SBP that is providing subsidized financing. In addition, Rs.60 billion is allocated over four years instead of allocating it only in the 2020-2021 budget.

The total financial impact of the proposed risk-sharing facility to the GoP has been worked out to the tune of Rs.25.84 billion to be provided to SBP for onward payments to banks over four years as per following details: (i) FY 2020-21, no allocation required; (ii) FY 2021-22 Rs 1.19 billion; (iii) FY 2022-23 Rs 6.24 billion; (iv) FY2023-24, Rs 11.06 billion; and (v) FY 2024-25 Rs 7.35 billion.

Renewable Energy Refinancing

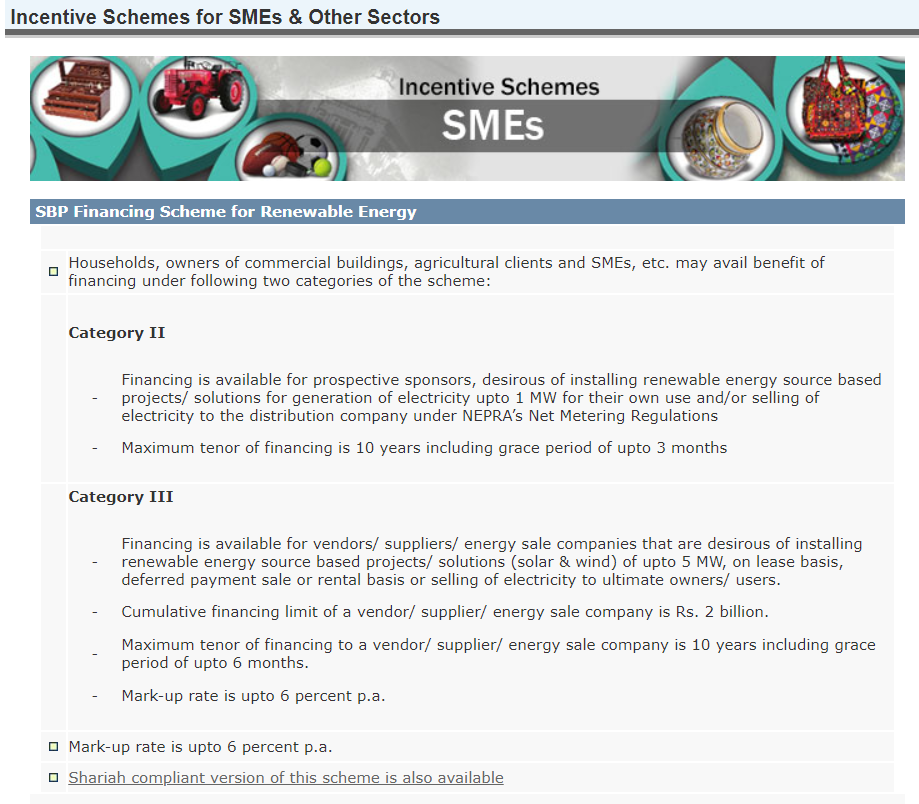

SBP published a press release on its website on May 4 and was reported in the newspapers on the following day that State Bank gives Rs36bn financing for renewable energy adoption.

The State Bank of Pakistan (SBP) has been providing financing on a large scale to promote renewable energy that helped Unilever Pakistan run its 30 per cent plants on renewable energy, central bank governor Dr Reza Baqir said on Tuesday.

As part of this financing scheme, Unilever availed a loan of PKR 833 million through Standard Chartered Bank to set up 8.85 MW of renewable energy production facilities across four factories in Punjab. This effort isin line with Unilever’s global mission for carbon neutrality and sustainability in its manufacturing process.

The press release goes on to state

The SBP issued its Financing Scheme for Renewable Energy in 2016 and based on positive feedback the scheme was revised in July 2019. SBP also introduced a Shariah compliant version of this Scheme in August 2019.

The impression I got was that without SBP refinancing Unilever would not have gone for renewable energy. But Unilever has the mandate to convert to carbon-neutral as part of their strategy. I would presume they would have gone for it with or without refinancing

This effort is in line with Unilever’s global mission for carbon neutrality and sustainability in its manufacturing process. Unilever has committed to remove carbon emissions from operations by 2030, as well as net zero emissions from their products by 2039, which will be 11 years ahead of the 2050 Paris Agreement.

From the REON Energy website

Reon’s partnership with Unilever began in 2015 when the multinational approached the renewable energy expert for a 30kW pilot project at their Tea factory site in Khanewal. The motive behind this installation was to implement their green energy leadership vision. After commissioning and upon evaluation the pilot project proved to be a success in achieving what the brand had sought – a significant reduction of 28 tonnes in the carbon footprint during the first year. This led Unilever to sign for a 100 kW extension on the same site in the following year alongwith 3 more projects sizing 200, 100 and 40 kW at their factories located in Karachi, Lahore and Phoolnagar respectively.

The success of these projects has won Reon a continuing partnership with Unilever with 4 additional sites in Punjab sizing up to a whooping 8.85 MW in 2020.

From the press release again

The renewable energy solution was implemented by Reon Energy Limited, producing 13 million KW units of energy per year, resulting in annual savings of PKR 182 million.

This translates into a payback period of approximately 5 years. This brings me back to the point I raised in my earlier post

majority of the refinancing was provided to large and existing clients.

Though the facility is for everyone, SBP's website reports the facility under SMEs

Yet the major celebration of the facility is when it is taken by a multinational company (though with Pakistani employees and Pakistani manufacturing setup) and financed by a multinational bank.

It would have been better if an example of a business such as below had been used. The majority of the businesses may not even approach their banks for this facility as they would presume it is only for such sophisticated entities as Standard Chartered and Unilever. The local commercial banks are making money in PIBs. Don’t think they have any incentive to reach out to medium and small businesses to market this refinancing.