SBP refinancings a success? Take my word for it

Letting the market choose winners was not as bright an idea as SBP wants us to believe

State Bank of Pakistan is patting itself on the back and getting praises for the refinancing facilities provided in the aftermath of corona crisis. The refinancing numbers reported by SBP are staggering.

“Total liquidity injected (through such schemes) over the last one year through a combination of all monetary measures...comes to around 5% of GDP (over Rs2 trillion),” he said.

The elected officials and the government can only dream about distributing this quantum of largesse and that too so quickly without raising the ire of NAB, opposition, and critics in general. In my earlier post What they didn't teach me at the business school about SBP's Magic Money Tree, we had arrived at the following conclusion with respect to refinancings/subsidies provided by SBP:

[subsidized financings provided by SBP] do not appear as subsidies in the national budget rather appear as income in SBP books. This income is eventually paid to GoP as a dividend.

Ironic isn't it? Whereas fiscal subsidies appear as expenses in the government accounts, quasi-fiscal activities (despite being subsidies in nature) translate into income in government accounts when SBP pays dividends to GoP.

When elected officials decide to direct subsidies or incentives to a particular sector, there are questions about cost-benefit analysis, efficiency, how to measure the impact, whether to use Randomized Control Trials (RCTs) or are we using “Evidenced Based Policymaking”. SBP has opened the spillways of liquidity and subsidies, yet there have been no questions. Everyone is parroting what SBP is reporting.

The ready acceptance of whatever is coming out of SBP is driven by the dogma that the government (including the central bank) should not pick winners i.e. which sector or industry to direct the subsidies to and let the market forces decide where to direct the incentives. In the case of SBP refinance facilities, SBP had decided to make the commercial banks the arbiter of who gets the subsidies. The same commercial banks that derive their major income from investing in PIBs, ripping vulnerable consumers off with bancassurance products and having negligible exposure to the SME sector.

SMEs

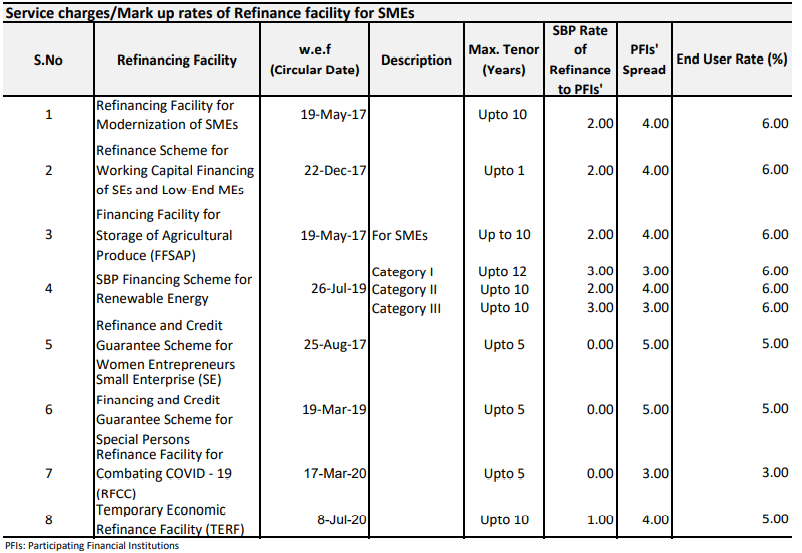

Below is the list of refinance facilities (subsidies) of SBP. If you go by the name of facilities, majority of facilities are for the SME sector.

However, as we are allowing the market (read commercial banks) to decide where to allocate credit, the larger number of facilities do not translate into SMEs getting much financing. The below table is from HBL's 1Q 2021 report (other banks will also have a similar breakdown) of the refinancings availed from SBP under various facilities.

Of the total Rs.128 billion of refinancing provided by SBP to HBL, share of SMEs is less than Rs.1 billion. If you are wondering, those four lines sum up to Rs.784 million.

SMEs constitute nearly 90% of all the enterprises in Pakistan; employ 80% of the non-agricultural labor force; and their share in the annual GDP is 40%, approximately.

Allowing the market to determine who gets subsidized financing results in only 0.6% of the refinancing flows to SMEs, the sector which employs 80% of non-agricultural labor force. Is it a right decision to allow the market/commercial banks to decide who gets the subsidized when the the market is truly broken?

TERF

If CFA Society of Pakistan was awarding prizes for best refinance facility, TERF would have won that award hands down. This facility has been praised by SBP and financial press extensively.

TERF can help expand manufacturing base in Pakistan. The risk to lend is borne by banks. The decision to select sector is of private sector.

When it comes to large and long-term projects (TERF is a 10-year tenor facility) banks do not lend to anyone except to their blue-chip clients__ the very clients that do not have any shortage of funding as the banks are falling over each other to lend to their projects. True to form, the funding flowed to the same old industries that it has already been flowing:

SBP Deputy Governor Sima Kamil has said in a TV interview that 40 percent of the investment is in textile, followed by building materials and many other industries. Some 25 percent of the projects are greenfield.

The same textile sector which has been hogging export refinancing for decades is the majority recipient of TERF. Unlike ERF which is also availed by smaller enterprises, TERF on account of being a 10-year loan would have been provided only to largest of the textile conglomerates followed by cement sector. If the objective is to get the market (ie commercial banks) to diversify the industrial base, it is a failure. The market is doubling down on what it already knows.

RFCC

If you need an example of how it doesn't cost a penny to SBP to create these facilities, no better example than Refinancing Facility to Combat Covid (RFCC). SBP is providing this refinancing at 0%.

The name is a misnomer. Initially it was only for setting up Covid19 wards, where commercial banks were required to ensure that financing is strictly being used for Covid purposes. Treating Covid19 is a loss-making provision so there wasn't much pick up. The facility was later revised for development of all healthcare facilities, however, the name of the facility wasn’t changed. Rs. 12.6 billion has since been provided under RFCC.

On the one hand, we should be pleased that in a country that lacks adequate healthcare and where spending on healthcare is negligible, subsidized financing is being provided to build health care centres. On the other hand, we should inquire what type of healthcare facilities are being built: will the hospitals built using this facility treat a wide strata of society or just treat the elite as banks only feel comfortable lending to hospitals that treat cash rich elite patients?

If it is the latter, we are providing extremely subsidized financing to build healthcare facilities to treat the rich.

Rozgar Scheme

This was a good scheme where SBP provided cheap refinancing to pay salaries. The amount is to be credited directly to the accounts of employees.

Theoretically, the facility was to be used by the entities that were facing challenges in paying employees due to economic slowdown. However, there is nothing preventing a shrewd employer, who is facing no issues in paying wages, from using this as a cheap method to finance working capital. If the employer traditionally used working capital financing from the bank to pay salaries, now they will not draw on the expensive line and use this cheap line to pay salaries despite the fact they don't need it. Why let a cheap financing opportunity go to waste?

The companies that were the richest and could afford to pay wages even without utilizing these facilities were getting their employees to sign pre-printed resignation letters stating that we are resigning due to domestic issues.

Artistic Milliners (one of the largest exporters in the country) and DESCON cut the wages of their employees by 30%-50%.

What if despite cutting the wages of their employees (which would have made them sustainable), DESCON and Artistic Milliner used the rozgar facility to pay the reduced salaries i.e., use the refinancing as cheap working capital? This wasn’t the intention of the facility.

There is 60% backstop by federal government i.e., if this loan goes into default, federal government will absorb 60% of the loss. Banks will still have to take a 40% loss. Most of the times, banks will lend to the customers where they don't expect a loss.

Meanwhile, SBP is counting every salary paid as a job saved. It may be reasonable assumption for SMEs but to include employees of larger businesses in that calculation appears to be case of statistical manipulation. I have covered in my earlier post that Naya SBP manipulates statistics freely and without remorse.

It is the most popular refinance scheme of SBP which has helped to prevent layoff of 1,848,945 employees of 3,331 businesses till end September 2020. Out of these, 313,599 employees are of 1512 SMEs and small corporates

SME employees comprise 16% of the total number of the jobs saved. The salaries of SME employees would be lower than the ones are larger businesses. This means in terms of size of the loan, share of SMEs in the facility will be significantly lower than 16%. Should the scheme be considered successful when one considers that SMEs employee 80% of the non-farm labour yet received even less than 16% of financing to pay wages of their employees?

It doesn't cost anything to SBP to provide the refinancing beyond spending a few minutes typing the circulars. The risk is being shifted to the commercial bank.

“We provided banks with limits (financing targets) and liquidity. Banks were, however, given a free hand to take credit allocation decisions.”

Banks decided which business idea should be financed and which should be rejected considering the feasibility and workability of the idea and the potential of a company to generate revenue and repay the loan.

“We told banks that we will hold them accountable through their asset quality indicators (like the ideas contribute to banks’ profitability or result in losses),” the governor said.

Thus all the credit is being taken by SBP while all the risk is borne by the commercial bank. Reminds me of my stock broker when he used to give advice to me in which stock market shares to invest "tips meri, risk aap ka". I find it amusing that SBP considers it a brilliant idea that they shifted all the risk to the commercial banks. The effect of this shift has been majority of the refinancing was provided to large and existing clients.

The current programs were designed on the fly, in the midst of a crisis, so it is understandable that not everything would have been gotten right. However, unless we have data that shows and is verifiable that the loans actually helped diversify the industrial base, added to the healthcare facilities, and saved jobs, all we have is SBP's word for it.

When everyone is praising these facilities, no one will try to improve upon them for the next incarnation or to make them more targeted for when a crisis takes place next time. Now that "six sigma events" and "hundred-year floods" are happening every decade, we should be thinking of incorporating such facilities as automatic stabilizers. But there has been no discussion with the exception of SBP patting itself, financial press patting SBP as the facilities are brought to a closed and Mission Accomplished has been declared.

The first step should be for SBP to release the name of the recepients of the facilities.

US

In US, Propublica does a great job of compiling all the data of who got what from the stimulus or bailout funds. This is the page for $1 billion received by Ritholtz Wealth Management (for those of you who listen to Barry's Master in Business Podcast). It caused a controversy “The Ritholtz PPP loan mystery” as Barry (CEO of Ritholtz Wealth Management) had earlier written a book Bailout Nation where he criticized the Obama era bailouts to banks.

You can navigate the Pro Publica page and find other recipients by industry, state, or entity.

UK

Similarly UK had two facilities one of which is for Corporates called Covid Corporate Financing Facility (CCFF). You can find the details on the recipients at Covid Corporate Financing Facility (CCFF): Borrowers and recipients list.

Biggest Beneficiary of U.K. Virus Aid Plan Is German Chemicals

The chemicals giant received 1 billion pounds, the maximum allowed by the BOE’s Covid Corporate Financing Facility, the central bank said in a statement Thursday. Other big borrowers include Bayer, the maker of Roundup weedkiller, and a unit of U.S. oil services company Baker Hughes.

The program, designed to help firms making what the government calls a “material contribution” to the U.K., is providing more money to firms controlled outside the country than to their domestic counterparts, the figures show.

That may stir controversy over whether the U.K. is imposing strict enough conditions on companies seeking state help. German aid rules prevent borrowers from paying dividends, while British Chancellor of the Exchequer Rishi Sunak has only asked them to exercise “restraint” on dividends and senior pay.

BASF said in April it wouldn’t draw on help available from Germany’s development bank. It still intends to increase its annual dividend, which last year cost almost 3 billion euros ($3.4 billion). A spokesman said the company has eight production sites and 834 employees in the U.K. as of December.

“These operations benefit the U.K. by providing employment; significant sales inside and outside the U.K.; investment in innovation and R&D in universities and institutions,” the company said in a statement.

Bayer spokesman Tino Andresen said the company had 880 full-time employees in the U.K. at the end of last year and generated 1 billion pounds of revenue in the country.

The press can cover the issues in UK and US as the names of the recipients have been disclosed. We are just relying on SBP's word that it has added to economic activity or saved jobs. SBP should be disclosing the name of the recipients of the facilities as well as letting us know how they are calculating the jobs saved and economic activity contributed. Without the transparency, there is no way to gauge if the SBP programs are working as promised.

This is what businesses are saying as per Business Recorder about the SBP facilities:

In terms of effectiveness of government support, a large majority of exporters felt that measures like reduced interest rate, refinancing schemes, relief package and tax-related facilitation at federal and provincial levels had “no impact” on their business. This runs contrary to statements made by doyens at SBP and FinMin on how their respective relief lines have rescued businesses. Rather, the areas of support which exporters found somewhat effective were non-monetary in nature, including continuity of financial system, public information/education during pandemic, and digital payment facilitation. Relatively more satisfaction with such measures suggests that exporters value facilitation more than financial relief.

When asked how the government could improve the design of current modes of facilitation, the top-five areas were concentrated mostly around facilitation in taxation-related matters. To be specific, exporters mostly want facilitation on direct taxes, GST on goods, electricity bills, customs duties, and tax compliance costs. The survey shows that larger firms are more vocal about demanding an improvement in facilitation measures than smaller firms. Perhaps the government can better segment and target its crisis intervention next time.

We also need to move beyond making the commercial banks gatekeepers of who gets the funds. Commercial banks are making most of their profits from PIBs and non-fee income by scamming consumers on bancassurance. They have no capacity or even willingness to diversify industrial base or reach out to SMEs.

Is Evidenced Based policy making only to be used when providing support to low income groups? When it comes to SBP refinancings, is mere utilization of the facility be deemed a success?