SBP should reduce the policy rate to below 7%

The central bank should never go full populist, but now that it has, it should not hold back.

One of the goals of this substack (apart from my vanity of continuing to have a substack) is to try to unpack the decisions which earlier I used to accept unquestionably because IMF or IMF trained management of SBP had proposed them. This wasn't the goal of this substack initially. SBP Governor Reza Baqir had been instrumental in this substack taking this turn. Initially, he was solely focused on keeping the discount rate at 13.25% to attract hot money. One can only write one or two posts critiquing that policy. But then he took a turn towards populism. That along with his love of PR provides me with enough new material to continue writing this substack. As a result, this substack has pivoted to “SBP-watch” with occasional diversions into other topics. Reza has been a gift that keeps on giving. From the feedback, I know people at SBP read this substack. If anyone at SBP reading this has access to Reza, please convey my gratitude to him. (Also I am running out of new current photos of him so more PR please).

When I started this substack at the beginning of this year, I expected to run out of ideas after 4-5 posts with half of the posts dedicated to real estate. Every post that I write, I believe is the last or second last post. Then some announcement comes from Reza which plants a seed that germinates into another post, or a tweet by SBP sparks an interest that sends me down a rabbit hole of research, or someone reaches out to me on email/WhatsApp/comments and points out an error or a shortcoming in my post compelling me to write another post to admit and rectify my mistake (a post is in the works with respect to this point).

Mostly I write for selfish reasons. There may be gaps in my understanding of financial matters or my way of thinking may be erroneous, so I publish in the hope that it may invite pushback in the comments or on Twitter or email. This has been an illuminating journey as my understanding of finance has improved considerably (I like to think) dispelling the mystique surrounding central banking. I have been able to confidently question the wisdom of SBP’s decisions when it came to inflation targeting, drafting of the SBP amendment act, and statistical manipulation.

Not all of my posts have been good but some, in my personal opinion, have been great. This is the 29th post since I started. My thanks to those who continue to read my ramblings and also to those who provide feedback.

You can reach out to me on Twitter at @2paisay or by email at 2paisay at gmail dot com.

Let’s get right down to it. SBP should reduce the policy rate from 7%.

We have already established over multiple posts including in revolution at SBP and inflation targeting continues to be the party line amongst economists that SBP cannot control inflation.

It boggles the mind that why price stability (inflation targeting) has been made the primary objective of SBP when SBP doesn’t have the capability to control inflation. The fault isn’t with SBP. The economy of Pakistan with low credit penetration, low contribution of private credit to GDP, negligible (0.2%) mortgage penetration, large undocumented economy, and significant control of pricing in the hands of cartels and mafias, is just not suited for the central bank to manage inflation.

The below meme conveys it best.

Businesses have been asking for a reduction in the policy rate. That is what businesses do: ask, ask, and then ask, ask again and then ask for some more.

انگلی پکڑاو، ہاتھ پکڑ لیتے ہیں

At one point, reportedly the PM also wanted the rate to be reduced to 5%. Economists, however, citing inflation numbers are opposed to a further reduction in the policy rate, if one goes by their op-eds and tweets. SBP's thinking is the same. Earlier I agreed with SBP's stance. Lately based on the steps taken by SBP, I am coming to the conclusion that SBP should decrease the policy rate.

When SBP increases or decreases the discount rate, it translates into a corresponding change in KIBOR, which is the benchmark used by commercial banks to lend to borrowers. By reducing the policy rate, SBP doesn’t directly increase the money supply i.e. SBP isn't printing money. An increase in money supply, if any, will be if commercial banks decide to extend more credit at lower rates. However, when SBP does refinance, it is directly increasing the money supply by printing money as we have already established in an earlier post.

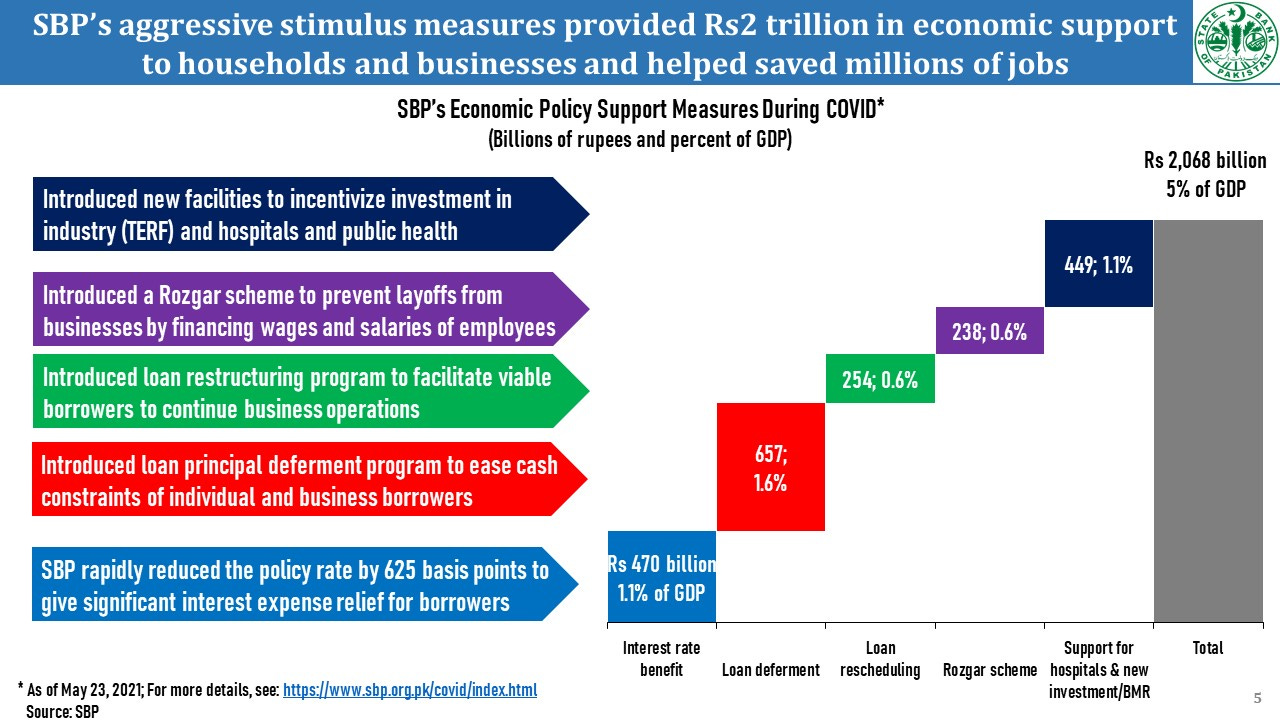

See the below slide from SBP about "aggressive stimulus" of Rs. 2 trillion (SBP's own words).

SBP has measured the impact of the decrease in policy rate at 1.1% of GDP and impact of money printing i.e. TERF and Rozgar scheme etc. at 1.7%. Thus refinance has a higher impact than the reduction in the policy rate.

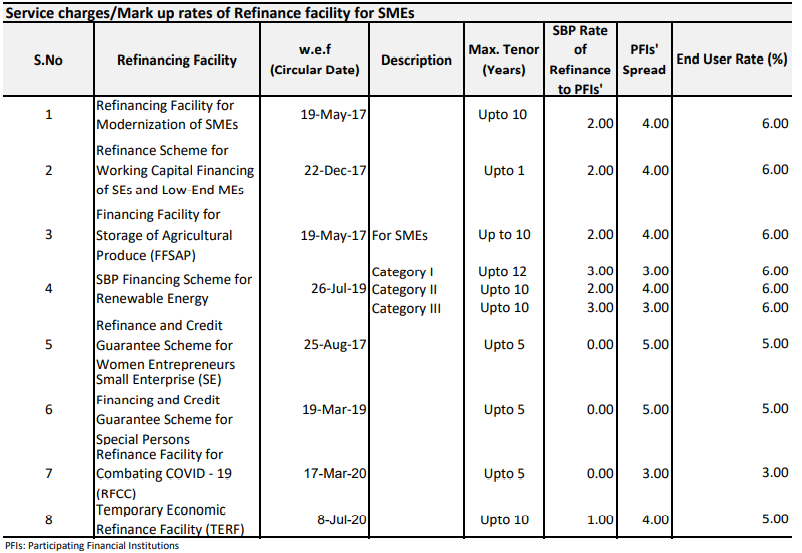

Below is the alphabet of soup of existing refinancing facilities. Except for renewable energy refinancing, the SBP rate of refinancing on all is between 0 to 2%.

Below are the loan figures of Habib Bank Limited, the largest private commercial bank. If we look at the last two columns, the total advances increased by Rs.80 billion for the year ended Dec 31, 2020.

Out of those Rs.80 billion, Rs. 63 billion of borrowing is refinanced with SBP. Thus, 78% of the additional borrowing is on account of refinancing.

If we look at the Q1 2021 financials of HBL, the advances have decreased by Rs.33 billion whereas refinancing has increased by Rs.3 billion. It appears KIBOR (read discount rate) based loans are being paid down while borrowers are taking more of refinancing loans.

I presume loan figures of other commercial banks will be similar.

In addition to eight already existing refinancing facilities, in May 2021 SBP has announced another refinancing facility called "Refinance and Credit Guarantee Scheme For Collateral Free Lending to SMEs" (a mouthful, I know) where SBP will be providing refinancing to commercial banks at 1%. More money printing.

SBP wasn't wrong when it said "aggressive stimulus" because the SBP’s money printer is really going Brrrr under Reza Baqir.

Why am I focusing on refinancing? When SBP reduces the discount rate, it is just a reduction in the discount rate. But when SBP announces a new refinancing product, SBP is not only engaging in money printing but doing it at a rate that is less than half of the discount rate.

Makes you wonder why is SBP keeping the interest rate at 7% when it is introducing all this refinancing at a rate that is less than half the discount rate and additional borrowing is on account of refinancing.

That is not all. SBP is also managing housing finance under Naya Pakistan Housing where the end-user rate will be 3% to 7% for the first 5 years.

The housing finance facility is a subsidized facility, not a refinancing facility. Here GoP is subsidizing the interest rates of the end-users. GoP has a fixed budget for the subsidy where subsidy is calculated as the difference between fixed-rate and the bank pricing. For example in Tier 1, the customer pricing is 3% whereas the bank pricing (assuming KIBOR is equal to the discount rate - not an unreasonable assumption) will translate into a rate of 9.5%. Thus, GoP will be subsidizing the interest on the loan to the tune of 6.5%. GoP has a fixed budget of Rs.36 billion for the interest subsidy. Higher the KIBOR, the higher the subsidy amount, the lesser the number of mortgages that will be subsidized. A lower KIBOR means that GoP's subsidy will have a longer runway i.e., it can provide subsidized mortgages to a larger number of house buyers.

A skeptical me in my last post wondered if Unilever really needed the refinancing facility to go for renewable energy or is it the SBP governor not letting an opportunity for PR go to waste.

SBP published a press release on its website on May 4 and was reported in the newspapers on the following day that State Bank gives Rs36bn financing for renewable energy adoption.

The State Bank of Pakistan (SBP) has been providing financing on a large scale to promote renewable energy that helped Unilever Pakistan run its 30 per cent plants on renewable energy, central bank governor Dr Reza Baqir said on Tuesday.

As part of this financing scheme, Unilever availed a loan of PKR 833 million through Standard Chartered Bank to set up 8.85 MW of renewable energy production facilities across four factories in Punjab. This effort isin line with Unilever’s global mission for carbon neutrality and sustainability in its manufacturing process.

The press release goes on to state

The SBP issued its Financing Scheme for Renewable Energy in 2016 and based on positive feedback the scheme was revised in July 2019. SBP also introduced a Shariah compliant version of this Scheme in August 2019.

The impression I got was that without SBP refinancing Unilever would not have gone for renewable energy. But Unilever has the mandate to convert to carbon-neutral as part of their strategy. I would presume they would have gone for it with or without refinancing

This effort is in line with Unilever’s global mission for carbon neutrality and sustainability in its manufacturing process. Unilever has committed to remove carbon emissions from operations by 2030, as well as net zero emissions from their products by 2039, which will be 11 years ahead of the 2050 Paris Agreement.However, some one who works in this space stated that without this facility, Unilever would not have gone for renewable.

Someone who works in this space stated that without this facility, Unilever would not have gone for renewable.

I didn't think that SBP could be any more populist considering this is the same SBP that didn't want to engage in quasi-fiscal activities as per its own proposed amendment in the SBP act. On April 29, SBP introduced Roshan Apni Car scheme.

A reasonable assumption would be that with a 3-month KIBOR at 7.25% and minimum tenor of the facility around 3 years, the rate on the facility should be in double digits. As per SBP's ad, the markup rate is 7%.

I could not find any circular on SBP's website on how this facility will be managed i.e. whether SBP will be refinancing it or will it be a GoP subsidy like housing finance or if the commercial banks are playing their part in nation-building by providing very cheap financing. Regardless, the rate on this facility is 7%, which again would imply that the policy rate should be less than 7%.

To summarize,

The majority of the incremental borrowing continues to be in refinancing which is financed by SBP at a rate less than half of the discount rate.

SBP introduced another new refinancing facility again at a rate that is less than half the discount rate. Let's not beat around the bush. The refinancing rate on this facility is 1%.

The housing finance facility, which is a subsidized facility, will be providing 5-year financing at rates ranging from 3% to 7% (a rate less than or equal to the policy rate).

Finally, SBP has gone full populist by pushing car financing which will be providing 3-year loans at 7%.

The question then becomes why do the SBP, oped writing economists and financial press continue to maintain the charade that 7% is the appropriate discount rate? There is no scientific basis for a 7% discount rate. The real rate is already negative at this level.

All the aforementioned steps taken by SBP show that SBP knows that if the country has to embark on a growth journey, the discount rate should be lower than 7%.