Since most of my posts are about SBP, I have renamed the blog to SBP Watch (and other hot takes). The first post after renaming, however, isn’t about SBP. The irony.

The below is an extract from the Budget 2021-2022 speech about Kamyab Pakistan Program (KPP).

Ignoring all the fluff and the sycophancy of the PM’s vision, KPP offers the following for the 4 to 6 million low-income households:

Every urban household gets up to Rs.500,000 interest-free loan.

Every farmer household to get i) an interest-free loan of Rs.150,000 per crop and ii) Rs.200,000 for tractor and machinery.

All the aforementioned households to get Rs.2,000,000 low cost (read subsidized interest) loans towards low-cost housing.

Every household to be provided a health card.

One person per household to free technical training.

I will focus on point number 3.

The maximum number of low-income households is 6 million as per the budget document and each household can get up to a maximum of Rs.2 million mortgage loan. This translates into an upper limit of Rs.12 trillion of mortgages. Let’s halve it. That makes it Rs. 6 trillion. Halving it again makes it Rs. 3 trillion (one-fourth of the upper limit) which I think will be a realistic, rather conservative, size of mortgage loans outstanding if the vision is realized.

The size of total mortgage loan outstanding used to hover around Rs.200 billion. It has started increasing since July 2020 after the discount rate was dropped and Reza Baqir has started pushing house loans. The major increase is coming from mortgages given to bank employees, as we had discussed in our earlier post. Share of the bank employees is 60%. Regardless, mortgages are increasing. The total outstanding right now (bank employees and consumers) is Rs.232 billion. It may reach Rs.300 billion by year end assuming the banks don’t run out of bank employees to provide mortgages to.

Realizing the vision means that mortgage loans need to increase by 10x, i.e. from Rs. 300billion by year end to Rs.3 trillion.

When I compare to the total borrowing by private sector businesses which stand at Rs.5.5 trillion inclusive of all the refinancing schemes such as ERF, TERF, RFCC, Renewal Energy etc., Rs.3 trillion of mortgages outstanding appears unrealistic to me.

PTI government’s Naya Pakistan Housing Program envisaged 5 million houses. The government hasn’t been able to make visible progress towards it despite setting up an agency, Naya Pakistan Housing Development Authority (NAPHDA) headed by a retired army general. PHATA, which earlier announced many projects throughout Punjab, has also gone quiet. Below are some announcements under the Naya Pakistan Housing vision.

This shows the magnitude of the challenge. The government has been unable to provide even a few thousand units in three years despite all levels of government i.e. Federal, Provincial, Municipal, and private sector players and associations involved in it.

The government is now hoping that by giving Rs. 2M to low-income groups, it can will 4 to 6 million houses into construction.

GoP needs to arrange funds to subsidize the interest rate on the mortgages. The government has budgeted a subsidy of Rs.36 billion. As covered in earlier post, this Rs. 36 billion can provide subsidies for around 20 to 25 thousand houses.

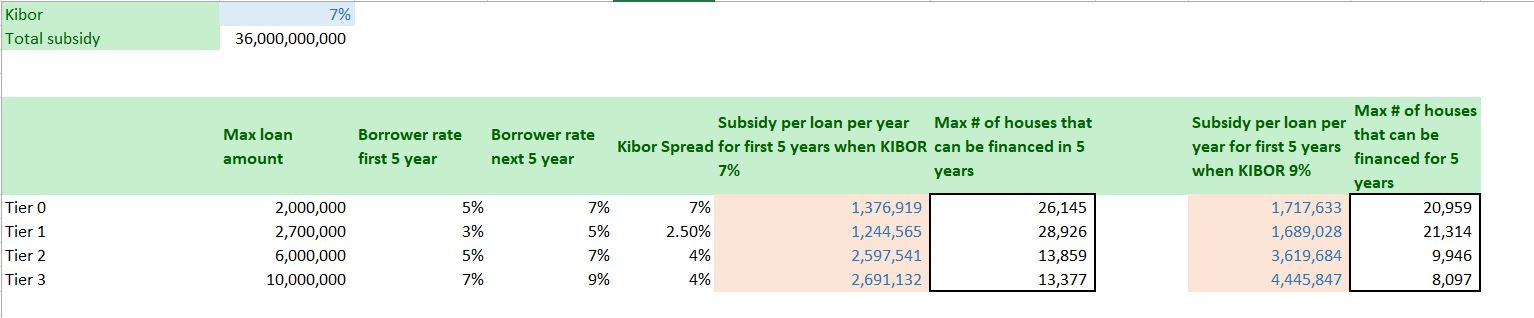

SBP issued a circular on March 25, 2021, with respect to housing finance that there is Rs.36 billion available to subsidize interest rate charged to borrowers on housing finance.

The below table details the mark-up subsidy that will be provided to borrowers.

Let’s take the first line. The borrower will be charged 5% while the bank will book the income at KIBOR+700bps. Let's assume a mortgage of Rs.2 million and KIBOR of 7%. For the first month, the bank will book an interest income of Rs. 23,333 i.e. Rs.2 million x 14% (7% KIBOR + 700bps) / 12 months. The bank can only charge the customer Rs. 8,333 (i.e Rs.2 million x 5%/12 months). Thus, the borrower will be provided a subsidy of Rs.15,000 (Rs.23,333 - Rs.8,333) in the first month.

It hasn't been stated but the subsidy will continue till Rs.36 billion runs out. How many houses can this subsidy finance? If the KIBOR remains 7%, this Rs.36 billion can subsidize 26,145 houses for 5 years (if their loan amortization period is 20 years) in Tier 0. If the KIBOR increases to 9%, this can finance only 20,959 Tier 0 houses.

If instead of Rs.36 billion for 5 years, we assume a yearly subsidy of Rs.36 billion (unreasonable assumption), the subsidy will only be sufficient to finance 130 thousand houses. Needless to mention, this assumes a KIBOR of 7%. If the KIBOR is 9%, the total number of Tier 0 houses that can be financed with an annual subsidy comes down to 100,000.

How does GoP expect to subsidize interest on 40x to 60x number of houses (100,000 units to 4M housing units) than it has budgeted for?

I don’t know if in urban areas of major cities there is anything that can be purchased with a mortgage of Rs.2 million. If there are some patches of cheap land available, I do not think it is large enough to accommodate more than a couple of hundred houses.

The easiest way to develop a large low-cost housing in urban areas would have been to build mid-rise or high-rise apartments. By themselves, ow income households do not have the resources and capabilities to manage a mid-rise i.e. even if they have the capabilities, they do not have access to resources to finance the construction. The best way would have been to make it part of the longest running money laundering scheme in the country, i.e. every project that is registered under the amnesty should deliver at least 10% or 20% of area as a low-cost unit.

But the PM is surrounded and advised by sycophants and real estate encroachers when it comes to real estate who have no interest in playing their part in realizing his vision. All they are interested in is maximizing their profit in the name of 40 related industries. Hence, such common sense ideas as inclusionary zoning or mandatory targets were not even suggested in the amnesty scheme.

The last three years have shown that GoP doesn’t have the capacity to deliver housing on a timely basis. Developments in Naya Nazimabad, Fazaia Housing, Bahria Town Karachi, and ARY Laguna, etc made it evident that even the private sector does not have the capacity to deliver on time and as per promise especially projects targeting middle class. The main challenge is cashflows. The developer does not want to invest money in purchasing land and building apartments before he gets a major chunk of money from the buyers. In the absence of mortgages, the buyer has to arrange the full price of the apartment from his cashflows. Not many buyers can arrange tens of millions (cost of the apartment) in the few years within which the builder has promised to complete the building. Unless the builder is constructing the building from his own resources or has investors backing him, the unpredictable cashflows results in construction delays of a few years beyond the promised timeline.

For a contrast, see the below project, which is launched under the amnesty scheme. There is a high likelihood that this project can be completed in 3 years. As Habib Islamic is providing mortgages, it can also provide construction finance to the builder. Construction financing will be repaid from the mortgages as soon as the building is complete. The cashflow problem we were talking about in the above paragraph is now resolved. However, this is targeted to high income group.

For timely provision of low-cost housing, the government needs to come up with a similar arrangement where all the prequalified buyers of low-cost housing will be allotted a unit against the approved mortgage. This will enable the builder to arrange construction financing to deliver low-cost housing on a timely basis.

Just handing over Rs.2 million to low income groups will not solve the housing challenge in urban areas.

The country is about to embark on consumption financed growth. GoP isn’t saying this outright, but we may be looking at larger deficits in the next two years. Consequently, liquidity will be tight in the banking sector i.e., after purchasing PIBs and financing businesses, banks will not have enough funds to provide Rs.1 trillion much less Rs. 3 trillion of mortgages.

However, this is one area that I am not concern about. If this thing takes off (very low probability because of the issues highlighted above), I have complete confidence that my favourite central banker Reza Baqir will come up with a refinancing scheme that will provide the necessary liquidity to carry this market.