SBP Amendment Act #15: Reza Baqir's Cloak and Dagger Act 2021

SBP knew that it was laying the groundwork for the recently imposed IMF conditions but feigned ignorance

I had hoped that my previous post #14 on the Act would be the last one.

Moreover, as the SBP Amendment Bill is making its way to the Senate tomorrow where it is expected to sail through, hopefully, this is the last post on the topic.

Unfortunately, the latest news about IMF report has me revisiting the topic once again.

I will try to keep this short as I am sure you, dear reader, are also getting tired of this broken record on the Quasi Fiscal Activities (QFAs) and Development Finance Activities (DFAs).

Unwind the QFAs an DFAs

Usman brought it to my attention.

The key sentences in the news report for the purpose of this post are

The IMF has also imposed the condition that by April, the Ministry of Finance and State Bank of Pakistan (SBP) will establish a Development Finance Institution to support the eventual phasing out of SBP refinance facilities.

The new institution will take responsibility for the SBP refinancing scheme, assess the Export Refinancing Scheme (EFS) by February-end and take needed actions to improve its effectiveness.

The IMF said that as of September 2021, the outstanding amount for all the SBP facilities was Rs1.22 trillion. The “staff warned that this expansion, if not temporary, would undermine the SBP’s efforts to credibly implement monetary policy, achieve its primary objective, and improve monetary policy transmission channels”.

If you have been following my tweets on QFAs and DFAs, the aforementioned addresses QFAs. Dawn also had a report on it, and it touched upon the DFAs.

IMF wants SBP to roll back housing finance measures

The International Monetary Fund (IMF) has asked the State Bank of Pakistan (SBP) to “unwind” the two key measures for the promotion of housing and construction activities.

In July 2020, the SBP made it mandatory for banks to increase their share of lending portfolios for housing and construction sectors to five per cent by December 2021. In addition, the SBP changed capital adequacy regulations in June 2021 to lower the applicable risk weight to 100pc from 200pc on banks’ investments in REITs or real estate investment trusts.

The staff report, which the IMF released along with the $1 billion tranche under the resumed loan programme, said the international lender “urged” the central bank to wind down these measures “out of concerns for financial stability”.

“Banks’ housing lending targets could present risks to financial stability and entail a misallocation of credit,” it said.

I told you so

Don’t want to blow my horn. Oh heck, why not. This request from IMF didn’t come out of the blue. There was a reason for introducing the prohibition of QFAs and DFAs in Section 20 as I have been saying since March 2021.

I wrote a blog post No more export refinance and Naya Pakistan Housing from SBP. If the below conversation is to be believed, it caused quite a stir.

To calm the market, MoF released a slide deck.

In the subsequent blog post Unsubstantiated claims in MoF slide deck, I addressed the above MoF claim

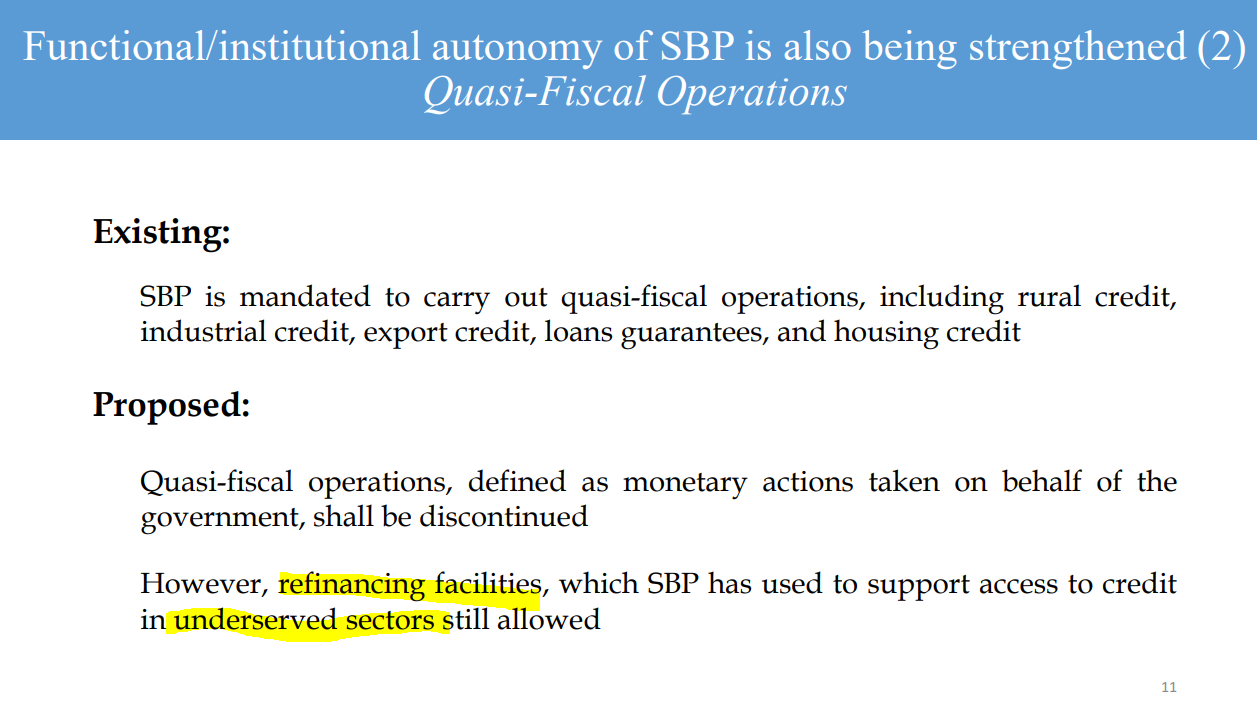

…. the MoF finance slide deck states that refinance activities to support underserved sectors will still be allowed.

The “underserved sector” isn’t defined anywhere in the Act pages we have seen. Will the export sector and industrial sector that are availing the maximum refinance (Rs.400 billion and Rs.100 billion respectively as per SBP 2020 Annual Report) be deemed as underserved? I don’t think so. Thus we can safely assume that export refinance, LTF, TERF, RFCC will not be provided by SBP as per the amended Act.

I had written this too.

At the end of the day, it is a policy decision whether SBP wants to engage in export refinancing or TERF. If SBP doesn’t want to do refinancing, fine with me. Just let’s not fool people by making wrong claims in a slide deck about what is allowed or not as per the Act.

The math doesn’t work for the new DFI

IMF says that the total refinance outstanding is Rs.1.22 trillion. SBP has multiple refinance facilities as listed below.

As per SBP’s Dec 2021 report, Rs.660 billion is outstanding in ERF and Rs.520 billion in LTFF/TERF. Thus, ERF and LTFF/TERF comprise the majority of the refinancing outstanding.

IMF is asking SBP to establish a development finance institution (DFI) by April end to eventually take over SBP’s refinancing activities. This is a very short timeline, and such a thing is only possible if an institution is already in the works. A DFI by the name of EXIM Bank of Pakistan already exists on paper and, as per LinkedIn, staffing is in progress. But EXIM Bank can only take over export refinance (ERF) facilities, as the name EXport IMport Bank implies. The government will have to establish another institution to take over LTFF/TERF.

The TERF/LTFF may eventually wind down over a period of 10 years (the term of TERF loans). ERF, however, has become permanent finance. Rs.660 billion of ERF is a large amount to shift to EXIM Bank. There are four options. As I want to keep this post brief, I will just mention them and not explain.

Option 1: If EXIM bank is to refinance commercial banks like SBP, EXIM Bank has to be capitalized with Rs.660 billion. Don’t think that will happen.

Option 2: GoP subsidizes the loan that commercial banks provide for exports. EXIM Bank acts as the bank that manages the subsidy (this activity is DFA and SBP can’t engage in DFA anymore). This will require GoP to budget Rs.33 billion subsidies for FY2021-2022 alone (5% subsidy between ERF and KIBOR multiplied by Rs.660 billion ERF). As ERF balance increases or KIBOR increases, GoP needs to increase the subsidy allocation.

Option 3: SBP shifts the smaller refinancing (SMEs, renewable, etc.) to another entity such as Pakistan Credit Guarantee Company and says to IMF that SBP is working towards that goal.

Option 4: Do nothing and business continues as usual, as BRR says in its latest piece:

Nonetheless, the amended SBP Act allows refinancing schemes to be roll out by the central bank if it’s not compromising long term price stability and in pursuit of SBP’s mandate.

In the same paragraph, BRR also states that these refinance are cannibalizing bank credit.

Right now, it’s money creation while being rolled by the SBP. Then these schemes are cannibalizing banks’ credit to private sector – especially long-term credit in the backdrop of TERF. If the government is to roll out mere credit subsidies, banks would be able to deploy their capital.

I am not intelligent enough to know what the aforementioned sentences are implying.

Deep Dive

If you want to really understand why IMF doesn’t like QFAs, I did a deep dive earlier. You won’t read a more comprehensive post. If you don’t get anything in the below post, ask me in the comments or on Twitter.

SBP knew it all along

My guess is, and the many people I discussed the latest development with agree with me on this, and this is pure SPECULATION, SBP knew and intended for the SBP Act to lay the groundwork for the prohibition of QFAs and DFAs but didn’t want to say it outright as it will cause a “stir” in the market. Now that the bill has cleared the two houses of the parliament, SBP is allowing IMF to show its true colors. SBP and IMF negotiations, if there were any, were just theater.

If you need evidence that SBP knows exactly what it is doing then look no further than this latest statement by the Deputy Governor of SBP as per SDPI:

"The language in the act may be informal, however, if needed, SBP may come up with a formal language for the public"

This is his statement about SBP Act, which was under discussion since March 2021, and has just cleared the houses of parliament. It is shocking to me that this is how SBP thinks legislation works in the country —> Get informal language approved by the parliament in an Act, and if the public demands it, issue a formal document.

Someone should tell Razak Dawood and GoP

As I had said earlier, if SBP doesn’t want to refinance because it distorts the budget or cannibalizes bank credit as per BRR, then SBP shouldn’t. It would be perfectly in line with the new SBP Act. But someone should tell the government. Razak Dawood, in an interview with BRR, a couple of weeks ago, was talking about enhancing and expanding the SBP’s refinance offerings:

Export growth strategy and tariff rationalisation are our two key objectives this year. The third is a sectoral financing facility. Temporary Economic Refinance Facility (TERF) was a brilliant incentive scheme for the exporters by the central bank, but the disadvantage was that it had no sector restrictions and 50 percent benefit of the scheme was taken by the textile sector. I am now talking with the State Bank that let’s have a sectoral refinance scheme.

Victory Lap

I will end the post here. There was no other purpose of this post than for me to take a victory lap for something that I said almost a year ago, and everybody else ignoring and claiming otherwise, finally turning out to be true.

I believe that QFAs and DFAs belong in a central bank’s toolkit.

Thank you for reading.