Lack of imagination in the Pakistani banking sector

SBP and its mandate is analogous to ARY and ARY Laguna project respectively

It says a lot about the lack of imagination in our banking sector that the central bank is threatening to execute on its threat of imposing a penalty on commercial banks for not meeting their construction and mortgage financing targets. The running joke is, with the banks making record profits, the banks have already provided for the penalty in their forecasts to their board of directors i.e., banks would rather pay the penalty than provide construction financing or mortgages.

If the SBP really wants the penalty to make a difference, it needs to be in the range of at least Rs.1 billion per bank per month.

SBP Gaming the system

The irony here is that SBP itself is providing banks opportunities and loopholes to achieve the mandate. I have covered them in detail earlier so only summarizing those here with a touch of snark.

From the lack of progress of the banks, one may presume that the SBP’s mandate is for mortgages for low-cost housing only. It is not. A bank can meet the target by providing mortgages to only ultra-high-income individuals. The mandate is not even limited to mortgages. It is for mortgages and residential construction financing i.e., a bank can finance residential construction only, provide zero mortgage and still meet the mandate. Oops. I just re-read the circular. Construction financing is not restricted to residential. All manners of construction is included. Thus a bank can provide zero mortgages, zero financings to residential construction, and just finance non-residential construction (a factory, a banquet hall, or a shopping plaza) and it can still meet the target.

The only thing left is for the SBP to allow car financing to be counted towards achievement of mandate.

This is not all. SBP subsequently issued a circular stating that if banks provide loans to REITs or invest in shares or bonds/sukuk of REITs, this will also be counted towards meeting the mandate. If the commercial banks are purchasing these instruments from the secondary market, then the banks are not actually financing construction. But SBP doesn't care.

Taking it to the extreme, SBP is even allowing investing in PMRC's sukuk/bonds to be counted towards meeting the mandate as long as the same bank is not availing financing from PMRC. To wit, say Bank Al Falah provides Rs. 1 billion of mortgages. PMRC refinances these mortgages by issuing Rs. 1 billion bonds. If Habib Bank invests Rs.1 billion in buying these bonds, SBP will be counting Rs.2 billion towards meeting the target: Rs.1 billion for Bank Al Falah for providing the mortgages and Rs.1 billion for Habib Bank for investing PMRC's bond.

There is more. To further entice the banks to invest in REITs (as clearly banks aren't inclined in investing towards mortgages or construction financing), in June 2021, SBP issued another circular stating that if the bank's investment is in shares of REITs, the risk weight will be 100% versus a risk weight of 200% for investment in shares of all other entities. Moreover, investment in REIT shares will be classified in "Banking book" and not "Trading Book" i.e. banks will not have to mark-to-market the investment in REIT shares daily.

SBP is acting like ARY, and the mandate is like ARY Laguna project

In the Laguna project, ARY is interested in selling forms and not the Laguna apartments. Similarly, here SBP is interested in, by hook or crook, reporting that the mandate has been achieved regardless of zero progress made towards the housing objective. The mandate was introduced to help the government achieve its aim of 5 million homes under Naya Pakistan Housing to get the banks to finance residential construction or provide mortgages. Now it appears that the purpose of the mandate is to help the banks to achieve the mandate (whatever that means).

Window dressing by SBP

This is my favorite anecdote and I can’t get tired of reposting it in full every time I get a chance. In Dec 2020, the SBP governor made a statement to PM that "banks have almost met their quarterly targets" by doling out mortgages as verified by SBP officials’ "mystery shopping". This statement was contradicted by Pakistan Banking Association (PBA) which around the same time sent an email to all the commercial banks that their performance in this regard is not encouraging.

Now SBP and PBA at least appear to be on the same page as they are engaging in chart crimes and number fudging together (click on the picture to enlarge).

If you want more details on all the aforementioned shenanigans, you can read my below post.

The penalty

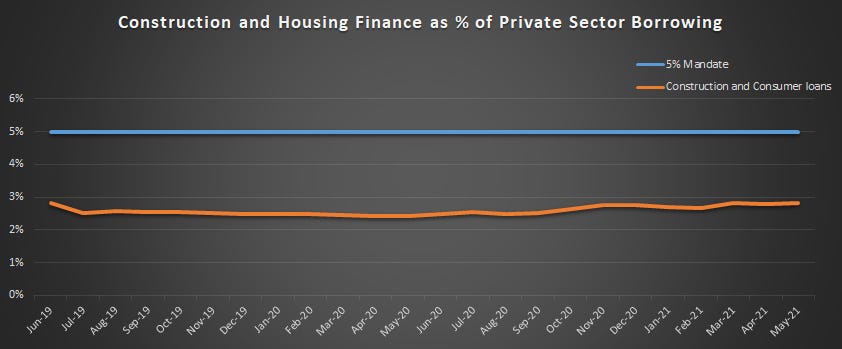

The housing mandate is SBP acting as an arm of the government in helping realize its housing manifesto. It appears SBP’s dream of being an independent central bank through the SBP Amendment Act has now been consigned to the dustbin of history. After giving all sorts of incentives and relaxations, the performance of the banks is unsatisfactory as shown by the below chart.

It makes you wonder that how and why did Reza Baqir claim before the PM in December 2020 that banks are meeting their quarterly targets when SBP has to finally resort to following through on its threat vide its IH&SMEFD Circular No. 08 of 2021

Please refer to IH&SMEFD Circular No. 03 of 2021, whereby Government's Mark-up Subsidy Scheme (G-MSS) for Housing Finance was issued.

Banks are expected to make all-out efforts to harness full potential of Scheme. Accordingly, in April 2021, SBP assigned monthly mandatory targets of number of housing units and amount of disbursements (G-MSS targets) to banks in proportion to share in total banking assets.

In view of foregoing, it has been decided that penalty will be imposed on banks falling short of their G-MSS targets w.e.f July 31, 2021 on both targets of number of housing units and amount of disbursements. A baseline penalty will be charged on shortfall from cumulative targets till July 31, 2021 while higher penalty will be charged on shortfall from targets of subsequent months.

The penalty charged on a bank will be adjusted after review of bank’s efforts in terms of logins of applications, approvals of housing finance, results of SBP’s latest mystery shopping surveys, involvement of bank’s management, evidence of board information and support, sale and marketing efforts, innovation in delivery channels, capacity building of staff and human resource (headcount) involved in G-MSS. To assess efforts, State Bank will, if required, collect information from banks which fail to meet their targets.

The penalty should be substantial

HBL’s full-year profit before tax (PBT) in 2020 was Rs.53 billion. The Q12021 PBT of HBL is Rs.16 billion. A penalty running into hundreds of millions of rupees won’t make much of a difference to HBL's bottom line.

A penalty less than Rs.1 billion per month would be a rounding error in HBL’s profitability.

But does SBP have the courage to impose such a high fine? I don't have anything against HBL. I just used it as an example here. The profitability of other banks won’t be much different.

Imagination limited to MoUs and signing ceremonies

Regardless of the penalty and the gamification, the point is that carrots and sticks are not working. Banks are simply not interested and not even trying. All they have are MoUs and ceremonies.

Check the hyperbole in the below press release. The first bank in the country to have entered this relationship. Working towards tirelessly. To provide international best practices. High-level support. National presence, largest distribution network, strategic national importance. Is HBL talking about financing houses or financing a nuclear power plant?

HBL is the first bank in the country to have entered into this relationship with NAPHDA. This project uplifts the lives of millions of people and provides them affordable housing- an objective that NAPHDA and HBL Islamic Banking are working towards tirelessly.

Under the MOU, HBL’s Islamic Banking team will act as a facilitator for providing consultancy services to NAPHDA. These services will include, but no limited to providing recommendations as and when required to the NAPHDA on models and prevalent best international practices with respect to low income housing schemes that may be suitable for the Project. HBL may also provide high level support and recommendations to make the Project bankable.

NAPHDA is a special body formed by the Government of Pakistan to construct over 5 million affordable housing units. HBL is Pakistan’s largest bank. The Bank’s national presence, largest distribution network, effective Islamic Banking arm and investment in technology and talent, enables the Bank to undertake this task of strategic national importance.

The need for low cost housing in Pakistan is a result of rapid urbanization, which has resulted in a growing number of people without access to affordable housing. The government has pledged to make over 5 million homes in the next five years and is the biggest government-backed housing program ever attempted.

Lt. Gen. Anwar Ali Hyder, (Rtd.) Chairman NAPHDA stated, “Pakistan faces a housing crisis. There is overall housing backlog of more than 10 – 12 million housing units. NAPHDA aims to provide affordable, dignified housing solutions to the citizens of Pakistan regardless of income level. Our agreement with HBL will enable us to avail their technical and financial expertise as we embark on this project of national importance with a direct impact on the economic rejuvenation of the country.”

Commenting on this strategic partnership, Muhammad Aurangzeb, President & CEO – HBL said, “This agreement will enable HBL’s Islamic banking arm to assist NAPHDA to build cost effective, sustainable housing units that will bring about financial and societal inclusion of the country. This initiative taken by the Government is commendable and will help uplift the lives of millions of people. We look forward to working with the dynamic NAPHDA team to play our part in the economic development of Pakistan.”

More than a year has passed since the MoU was signed talking about working tirelessly for achieving this task of strategic national importance. What does HBL Islamic Banking and NAPHDA have to show so far? Zilch. Now SBP is talking about imposing a penalty. The only thing that has made it to the press is the below project where apartments are starting from Rs.3.75 crore. I wonder if it is also considered a project of national importance and if NAPHDA is involved in this project of national importance with a direct impact on the economic rejuvenation of the country.

On the other hand, UBL held a huge signing ceremony with repeat scammer Salman Iqbal for ARY Laguna for opening an…. wait for it…. an escrow account!!!

The project is a scam as I have covered in my earlier posts. Each day new details are revealed about this scam. See the latest one below.

Is this the extent of the imagination of Pakistani banks i.e. signing MoUs and opening escrow accounts? Can't their investment banking teams cajole the reputable builders to build apartments for working professionals that they can finance through mortgages?

NAPHDA Chairman following in the footsteps of the SBP governor?

Even the General Anwar Ali Hyder of NAPHDA has nothing to show for his time at NAPHDA. He appears to be waiting on the builders to throw a bone in the form of a few low-cost plots/houses that he can claim as progress towards the vision. I would love know what briefing the NAPHDA chairman provided to the PM when banks aren’t by mortgages to middle classes much less to low-income groups.

PM satisfied over boom in construction sector

The prime minister, in a meeting with Naya Pakistan Housing Development Authority (NAPHDA) Chairman Lt Gen Anwar Ali Haider (retd), appreciated the pace of development work that continued despite the coronavirus pandemic.

The NAPHDA chairman briefed the prime minister about the projects particularly related to the low-cost housing.

Negligible role of PMRC

One can attribute, partially, the reluctance of commercial banks to provide mortgages to the fact that mortgages are for a term of 15 to 20 years and banks don't have such sources of financing. This is where Pakistan Mortgage Refinance Company (PMRC) comes in. If PMRC can provide long-term financing to banks, banks can offer mortgages. But PMRC’s targets are so minuscule that it can’t play a meaningful role in helping the banks achieve the mandate.

As of May 31, 2021, banks are short of Rs.147 billion from achieving the mandated target.

Meanwhile, PMRC is targeting a securitization portfolio of Rs.1 billion in 3 years and that too in a portfolio of mortgages extended to government employees.

Mr Khan said a stringent legal framework with standardised loan application and approval processes will accompany the securitisation of mortgages. “We won’t securitise low-income housing loans. We’ll securitise other loans but use the proceeds to promote low-income mortgages. We’ll ensure that people trust the paper issued by PMRC. We won’t sell anything that’s prone to default,” he said.

For its first securitisation-related transaction, PMRC is looking for a “safe” portfolio of at least Rs1 billion that ideally has home loans extended to government employees. “The risk will be smaller. It’ll be easier for investors to assess and take exposure. But if I take a low-income loan portfolio, people won’t understand the risk and pricing will go up. That won’t serve our purpose. The money we’ll raise will then be deployed again in home financing,” he said.

Lack of imagination

At least HBL is working with Dolmen for Grove Residency. After the initial announcement of the project earlier this year, the project had gone quiet. I have been told that Grove Residency is again aggressively marketing the project on social media. Maybe it is the SBP penalty that is pushing HBL to push for this project. This project in district Korangi read Qayyumabad (or "Defence ke baghal mein") isn't for everyone. Assuming 400 apartments at an average price of Rs. 4 crore, the total project sell out value comes to around Rs.16 billion. At 70% to be financed by mortgages, HBL Islamic can provide Rs.11 billion of aggregate mortgage financing.

In addition, if assume a 75% margin for the developer, the project cost comes to around Rs. 12 billion. HBL may also be providing construction finacing of around 50% (for simplicity I have included the land cost in project cost) which is another Rs. 6 billion of construction financing.

Thus HBL may end up provide Rs.17 billion of financing for this project which may help HBL achieve its mandate. People who can afford Rs.4 crore apartments aren't exactly the ones for whom the SBP mandate or PTI's Naya Pakistan Housing was introduced but you can't really blame HBL for financing a project that qualifies for the mandate. However, there has been no progress from the other banks. I believe they will try to qualify by financing office buildings and plants/factories.

Banks would rather lose money lending to Hascol __ reportedly Hascol's bank borrowings stand at Rs.60 billion at the time of default __ than work with developers to come up with projects and provide construction financing and mortgages.

Living in a fool’s paradise

Despite SBP giving every incentive that it can possibly give short of a refinancing facility, and GoP providing the longest-running state-sanctioned money-laundering scheme aka construction amnesty along with subsidizing the interest rate on the mortgages of up to Rs. 1 crore, the banks aren't falling over each other to either finance construction or to provide mortgages. (FYI, Grove Residency is also registered under construction amnesty thus providing both the developer as well as the buyer an opportunity to whiten the money).

If the banks aren’t willing to finance a project even in the Rs. 1 crore range (where white-collar workers can come up with a minimum downpayment of 30%), then

the SBP Governor, SBP management, NAPHDA Chairman, and rest of the housing task force are living in a fool’s paradise

if they think mortgages will be offered to the low-income segment (Tier I/ Tier 0) or the middle-income segment (Tier II) especially when even PMRC doesn't want to securitize it either.