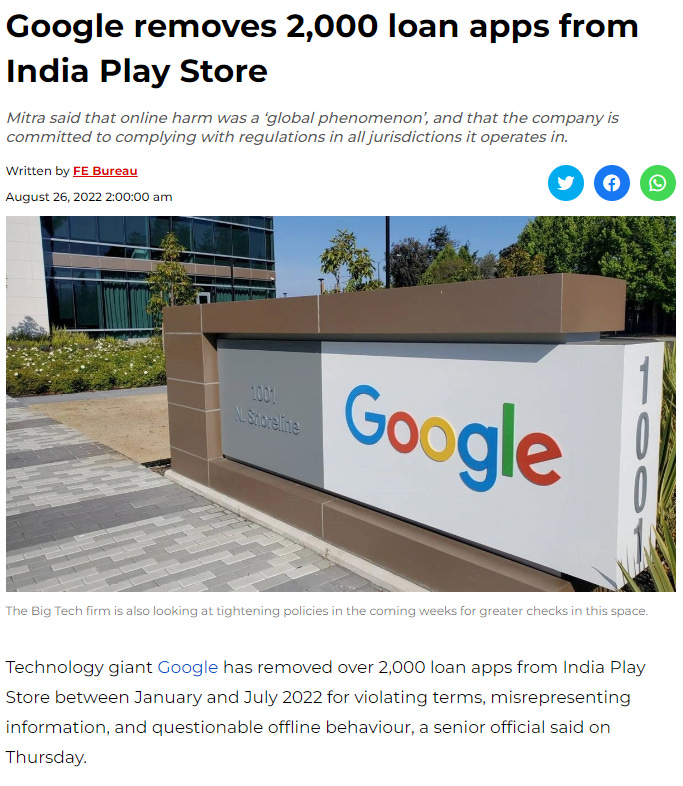

Instant Loan Apps violating Google Playstore guidelines

Meanwhile SECP declares its impotency in replying to The Profit

Let’s start with the Google app store policy on personal loan apps

Lets take a few statements

1. Google Playstore does not allow apps that promote personal loans which require repayment in full in 60 days or less from the date the loan is issued.

Turns out the almost all of the instant loan apps are in violation of Google Playstore policies. As they may show 60+ day loans in their advertisements, most of their loans are for smaller period. The CEO of Barwaqt explicitly stated this in his interview to The Profit

In our conversation with Abrar Ameen, the CEO of SeedCred Financial Services, annualizing a monthly interest rate and calling it predatory is a mistake because their lending cycle is not on an annual basis.

“Our product ends in 30 days. No one is giving or taking out a loan for a year. If we were giving out a loan for a year, we would also have set our rates based on 6-month or 1-year KIBOR and some spread,” says Abrar.

Thus, the Barwaqt instant loan is a clear violation of Google Playstore policy.

2. Google Playstore requires apps in US to display their maximum APR. APR should be calculated including all fee.

We have seen above the Barwaqt CEO doesn’t even want to calculate the APR because he thinks it is misleading. None of the apps in Pakistan display APR, neither in their apps nor in their advertising. Let’s take the EasyCash1 which is a product of easyPaisa.

What can we see here?

The loan is for 59 days which is a violation of Google Playstore policies

No APR is mentioned

EasyCash tries to hide the interest rate by calling it a weekly fee which is misleading. The weekly fee translates into an interest rate of 5% per week and translates into APR of 264%. No wonder easypaisa is hiding behind calling it a weekly fee.

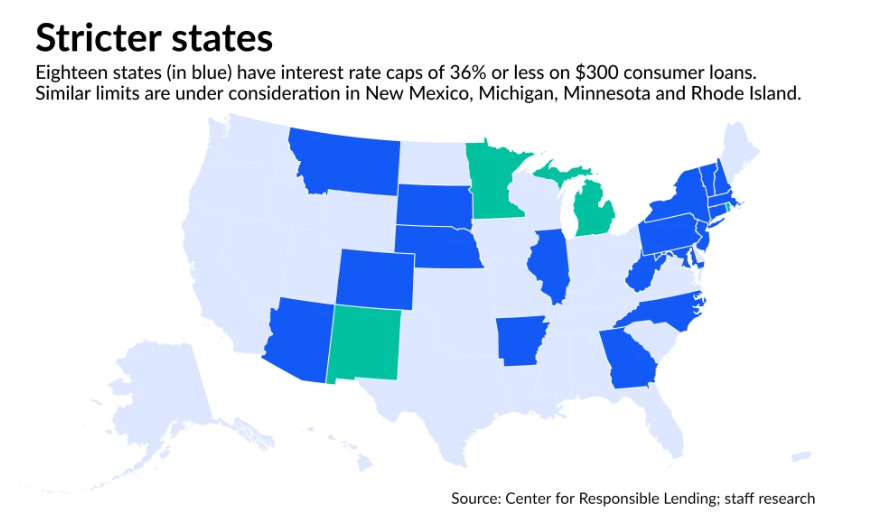

3. In US, Google Playstore does not allow for instant loan apps with APR higher than 36% and requires clearly mentioning APR in the apps.

There is a concerted movement in US towards capping the interest rate on short term personal loans

More states look to cap consumer interest rates at 36% | American Banker

Lawmakers in New Mexico recently approved a 36% rate cap, which would slash the state’s current maximum APR from 175%. It now awaits the governor’s signature. Legislators in Rhode Island and Minnesota are considering similar restrictions, and consumer advocates in Michigan are gathering signatures for a ballot initiative on the same issue.

The state-level action comes as congressional efforts to institute a national APR cap of 36% remain stuck. The federal legislation, championed by Democratic lawmakers, is similar to the limit Congress put in place for military members in 2006, though it would apply to all borrowers.

Consumer advocates still hope lawmakers will give all consumers “the same kind of protection that Congress thought was needed” for military members, said Yasmin Farahi, senior policy counsel at the Center for Responsible Lending.

We are talking about United States here. The leader of the free world and promoter of laissez faire policies world over. But any talk of such interest rate caps in Pakistan would invite claims of interference in the free market working from economists and bankers. The lowest rates are claimed by easyPaisa and Mobilink microfinance bank which we can see is in the range of 264%. Sarmaya Microfinance claims to be in the same range. Barwaqt’s rate are in the range of 400%.

None of these apps show APR hiding behind such terms as weekly fee. Sarmaya Microfinance claims to be providing interest fee loan when the APR is in 280% range.

4. Copy of License / Registration is required from apps in India, Indonesia and Philippines

What is preventing SECP from reaching out to Google and having similar sort of guidelines incorporated for Pakistan? From the Profit piece

The curious case of nano lending apps - Profit by Pakistan Today

While actions have been taken against the registered lenders to tone down their supposed predatoriness, no substantial action has been taken by the SECP against the illegal apps which we earlier categorized as actual loan sharks because they operate completely outside the ambit of the law.

The SECP has only said that they can not directly take down these apps. Instead, it has sent requests to relative authorities to take them down, without specifying who these authorities were.

So far, only two of the 17 illegal apps have been taken down. This means the majority of the actual loan sharks are still operational.

So far what we have seen is that Google Playstore policies are more consumer friendly than what SECP is doing and almost all the instant loan apps are in violation of Google Playstore policies. All it will take SECP or the consumers is to reach out to Google to get them to close down all the apps both regulated and unregulated. From the playstore policies, it is clear that SECP is backward than Indian, Indonesia and Philippines if they haven’t reached out Google for only allowing regulated entities to be listed on playstore. It is not that SECP can’t do anything, it is just that SECP doesn’t want to do anything.

I wasn’t wrong in this tweet

Comatose Competition Commission

(the alliteration is unintended)

While SECP is laying down the red carpet for such , Competition Commission of Pakistan is in vegetative state.

From the February 2009 order of Competition Commission of Pakistan

Office of Fair Trading (OFT) in Competition Commission of Pakistan (CCP) has been established to create a business environment in Pakistan that is based on healthy competition in order to protect consumers from anti-competitive practices. OFT has been established with the aim of enhancing the link between CCP and the consumers and to establish a focal point for identifying and providing solutions to issues which pose or may potentially pose problems for the consumers arising out of deceptive marketing practices. The OFT’s mandate is to oversee and act as a watch dog for misleading and deceptive marketing practices as enumerated in Section 10 of the Ordinance. It aims at paving the way to create consumer awareness with the objective of making markets function better for consumers and to ensure fair dealing in businesses. The focus is on the protection of consumers from deceptive marketing practices to ensure provision of adequate information to enable informed consumer choices.

Section 10 of the Ordinance prohibits deceptive marketing practices, which is reproduced herein below:

10. Deceptive marketing practices. (1) No undertaking shall enter into deceptive marketing practices. (2) The deceptive marketing practices shall be deemed to have been resorted to or continued if an undertaking resorts to: - 16 - (a) the distribution of false or misleading information that it is capable of harming the business interests of another undertaking; (b) the distribution of false or misleading information to consumers, including the distribution of information lacking a reasonable basis, related to the price, character, method or place of production, properties, suitability for use, or quality of goods; (c) false or misleading comparison of goods in the process of advertising; or (d) fraudulent use of another’s trademark, firm name, or product labelling or packaging.

In my considered view Section 10 of the Ordinance talks of deceptive marketing practices which without prejudice to the generality of the provision broadly includes distribution:

(a) of ‘false information’, or

(b) of ‘misleading information’;

(c) to consumers, or

(d) fraudulent use of another’s trade mark, firm name or product labelling or packaging.

‘False information’ can be said to include: oral or written statements or representations that are; (a) contrary to truth or fact and not in accordance with the reality or actuality; (b) usually implies either conscious wrong or culpable negligence, (c) has a stricter and stronger connotation, and (d) is not readily open to interpretation.

Whereas ‘misleading information’ may essentially include oral or written statements or representations that are; (a) capable of giving wrong impression or idea, (b) likely to lead into error of conduct, thought, or judgment, (c) tends to misinform or misguide owing to vagueness or any omission, (d) may or may not be deliberate or conscious and (e) in contrast to false information, it

In purview of the aforementioned, all the apps whether regulated or unregulated are engaged in in false or misleading information by not mentioning the interest rates when all of them are charging interest directly or indirectly in the form of fees and not including all the fees and expenses when calculating APRs, if they do mention it.

Barwaqt Microfinance went a step further by providing a misleading comparison. This is a straightforward case for Competition Commission of Pakistan to heavily penalize them. Barwaqt is charging 0.8% per day which is an APR of 292%. It doesn’t mention anywhere in their app that this is a daily interest rate.

As I have shown in the Bancassurance case, that both SBP and SECP are impotent when it comes to consumer welfare and consumers have to approach Insurance Ombudsman for relief.

I believe we have a similar challenge here. SECP is on the side of predatory lenders here. We will have to reach out to OFT at CCP and see if they can get the consumers some relief.

Ms. Rahat Kaunain Hassan is the author of the CCP order above and Ms. Kishwar Khan is the head of OFT. It behooves everyone of us to reach out to them and tell them about false and misleading marketing practices of these apps. Their email addresses are

rhassan@cc.gov.pk - For Ms. Rahat Kaunain Hassan

kkhan@cc.gov.pk - For Ms. Kishwar Khan

Also, as most of these apps are in breach of Google Playstore guidelines, use the following methodology to report these apps.

If SECP won’t get these apps to improve their product offering and transparency, may be by reaching out to Google and CCP, we can force their hand.

Zaki Khalid doing God’s work

The below made it to the newspaper

Tension within SECP escalates as it tries to downplay data breach (thenews.com.pk)

The relevant commissioner, Sadia Khan, claims she was not informed. She would only come to know three weeks later when a citizen, Zaki Khalid, who works on open-source intelligence, brought this matter to the attention of the government through the Prime Minister portal. A hacker from Estonia has claimed the responsibility of stealing the data. This coincides with an ongoing training on cyber security of SECP officials being conducted by Estonian trainers. The SECP said there was no correlation between the two.

Upset at this breach, Sadia Khan, not only lodged a protest within the SECP, she has written a letter to Finance Minister Miftah Ismail. “It is with a sense of deep concern that I am writing to you to inform you about a serious case of data leakage… I was informed about the incident in the afternoon of August 18, 2022, through a junior officer… even though the leakage of data took place on July 27, 2022… I requested a Commission meeting which though convened [it] was cancelled at the request of the Chairman.”

If the information being conveyed, she writes further, about the extent of the data leakage is correct, “the damage done from this incident is unprecedented.” She has demanded an independent investigation of the incident before the damage is irreversible, both in terms of the sanctity of the data entrusted to us as well as the reputation of the Commission, reads her letter. At present, there are only two commissioners, Chairman Amir Khan and Sadia Khan. Three seats are lying vacant.

Amir Khan was appointed chairman by the PTI government in 2019. Sources within SECP claim Mubashir Sadozai, the current head of information security, doesn’t have requisite IT qualification and was given this charge thanks to his closeness with the chairman. Chairman Amir Khan, however. replied that the said IT person is acting in charge only and was given this charge after the incumbent resigned a year ago. Amir Khan said the acting charge is given to someone who has the most relevant background from existing pool within the SECP as said person looks after e-services also. “I didn’t know the said gentlemen until three years ago”, Amir said, refuting the allegation of any personal bias. The chairman also added, “I was informed of the breach on the 18th of August, which is 10-12 working days after it took place. This is unfortunate. The same day, however, Sadia Khan who is also head of the information security, secretary finance and policy board chairman were informed. Same day press release was issued.” However, The News understands through documentary evidence that the matter had been brought to the attention of the Chairman Secretariat on July 27 through Musarrat Jabeen, Executive Director of Chairman Secretariat. The chairman may not have been informed.

Sadozai is not only the head of information security; he holds several other charges. He is registrar of companies as well as the head of administration, finance and compliance departments. Neither any inquiry has been ordered against him or any other official.

Meanwhile, once again in India

SECP expressed impotency on going against these apps. Once again, I recommend everyone to reach out to CCP and Google to get these apps to improve their transparency.