This is a long post and most likely would have been clipped if you are reading it over email. If that is the case, click on the title above to read it in full on the website.

Whenever retirement approaches for someone who is considered a “savior” by a section of the population, Pakistanis go into a “please don’t go” mode.

When Pervez Musharraf was supposed to retire, a purely “organic” movement named “Pervez Musharraf Himayat Tehreek” was born and graffiti (read wall chalking) could be seen all over Karachi asking him not to leave.

When Raheel Sharif was about to retire, banners were put up by “Move On Pakistan” (a political party?) all over Karachi asking him not to leave.

When COAS Bajwa’s was due to retire, former PM Imran Khan extended his term for three years. The matter landed in court and this is what the Chief Justice said about it

the CJP said the stated purpose for the proposed re-appointment/extension “regional security environment” was "quite vague". "If at all there is any regional security threat, then it is the gallant armed forces of the country as an institution which are to meet the said threat and an individual’s role in that regard may be minimal. If the said reason is held to be correct and valid then every person serving in the armed forces would claim re-appointment/extension in his service on the basis of the said reason."

Anyway, I am sure all those, who were in the government at the time but are in opposition now, and had recommended and approved the COAS’s extension, along with their entire social media brigade, would be trying very hard to remember if the “regional security environment” was really such that an extension was needed in the tenure of COAS. Too late now, ha! If anything, the regional as well as internal security environment is more volatile and dangerous now. All the more reason for an experienced hand to continue to be at the helm. Yet no one is talking about another extension. Hmm…

The court made a good point. It wasn’t the COAS as an individual who has to face the threat but the army as an institution. Was there no one in the army’s roster of three and two-star generals who can step up to the plate when a COAS retires during what one would normally describe as a “peacetime”? Did no one from the social media team recommending his extension remember how Umar RA removed Khalid RA from the command or how Churchill changed commanders in the middle of World War II? But I digress.

We are again at a similar stage. This time the person of interest is a civilian heading a civilian institution.

جی ہاں۔ میری، آپ کی بلکہ ہم سب کی پسندیدہ شخصیت

جی صحیح پہچانا

ہردلعزیز گورنر اسٹیٹ بنک

محترم جناب رضا باقر صاحب

As the 3-year term of Reza Baqir is coming to an end, a section of the population is making noises to renew the term of Reza Baqir due to “prevailing economic uncertainty”.

Unlike the extensions of the military and bureaucratic officers approaching retirement, Reza Baqir isn’t approaching retirement. His initial appointment was for three years. Under the SBP Act, he can be appointed for one more term of five years if the government of the time decides. It is for the government to make a decision if they want to retain him or bring someone else to the job. Isn’t there anyone in the country or the diaspora that is talented enough to take over the position? If the government is planning to bring a retired docile babu to replace him which I hope they don’t then it’s preferable to retain him. Otherwise, the government should carry out interviews of suitable candidates to at least see if a better person is available. If there isn’t a better replacement or he/she is unwilling to take the risk of leaving their existing employment in such challenging times, then yes renew RB’s terms. It is ironic that in a country where “ٹیلنٹ کی کمی نہیں” we are always short of suitable candidates.

This is my summary of his time at SBP most of which was covered in this substack. It is neither unbiased nor it is comprehensive. It is in no particular order.

Roshan Digital Account - Naya Pakistan Certificate

GoP launched the Pakistan Banao Certificate under the leadership of Asad Umar. I had written a post at the time on PBC titled How not to launch a diaspora bond. The product failed to take off. Reza Baqir joined SBP a month later. The product was redesigned and launched as Naya Pakistan Certificate under Roshan Digital Account. It has been a very successful product as Miftah acknowledges.

I wrote a few posts about how the NPC is hot money, with the last one where I criticized Reza Baqir for literally pushing the bank presidents to actively court hot money.

SBP is aggressively courting hot money in RDAs and doesn’t care if the funds are leveraged.

SBP is pushing the overseas branches of banks to borrow from interbank market (most likely on short term basis) to offer higher leverage to overseas Pakistanis to invest in relatively longer term RDAs.

SBP is asking Islamic banks to take lead from DIB to offer higher leverage on Islamic products which may fall foul of sharia boards of those banks.

SBP is pushing CEOs of banks to unjustifiably spend higher time and resources on RDA.

SBP Governor has gotten addicted to holding prize ceremonies with the PM. The slowdown in RDA inflows is forcing him to take desperate measures.

However, it turned out that these deposits are more sticky than I anticipated. Despite the fact that overseas Pakistan tried to run a social media trend to pull out funds from RDA when Imran Khan was constitutionally removed from his position, there hasn’t been a massive outflow as far as I know.

It required a massive push from SBP, with the SBP governor holding prize ceremonies and holding regular meetings with the bank CEOs and higher-ups, but it did deliver the results.

I have to admit that I was wrong on this one.

Digital Banking, RAAST, and Startup financing

I don’t follow this space but Ariba wrote a piece for Deal Street Asia summarizing the work he did.

The SBP finalised the Digital Banking Policy in January 2022, paving the way for digital banks that can offer not only mobile wallets but also credit, investments and other products.

The SBP, which is looking at granting up to five digital banking licences, has received 20 applications from domestic banks, microfinance banks, electronic money institutions, and fintech players. The SBP is likely to announce successful applicants within the next few months.

….

Pakistan’s fintech infrastructure got a huge fillip with the launch of the micropayment gateway RAAST – which went live in February 2022. RAAST, akin to India’s United Payments Interface (UPI), enables end-to-end digital payments amongst individuals, businesses, and government entities instantaneously.

Dr Baqir says RAAST has the potential to give a tremendous boost to the fintech sector in Pakistan. “It’s free, secure and provides the enabling environment over which fintech can offer other financial services.”

…..

“I don’t think the growth in startup activity in the last 2 years, particularly in fintech, would have been possible without the support of the government and regulatory bodies such as SBP and SECP (Securities & Exchange Commission of Pakistan),” according to Misbah Naqvi, co-founder and GP, i2i Ventures.

Echoing the views, Tiger Global-backed digital ledger app CreditBook co-founder Hasib Malik said, the SBP has been a proactive stakeholder in Pakistan’s booming fintech space.

In one of the landmark reforms that boosted overseas capital inflow, the SBP allowed startups to have holding companies outside the country while the operating company was located in Pakistan.

Hot Money - PIB

Reza Baqir started with the trick with which he made a name for himself in Egypt i.e., raising the interest rates to attract hot money. Though we were told that the purpose was to fight inflation but all of us knew it was to attract hot money.

At its meeting on 16th July 2019, the Monetary Policy Committee (MPC) decided to raise the policy rate by 100 bps to 13.25 percent with effect from 17th July 2019. The decision takes into account upside inflationary pressures from exchange rate depreciation since the last MPC meeting on 20th May 2019 and the likely increase in near term inflation from the one-off impact of recent adjustments in utility prices and other measures in the FY20 budget. The decision also takes into account downside inflation pressures from softening demand indicators. Taking these factors into consideration, the MPC expects average inflation of 11 – 12 percent in FY20, higher than previously projected. Nevertheless, inflation is expected to fall considerably in FY21 as the one-off effect of some of the causes of the recent rise in inflation diminishes.

It attracted almost $4 billion. What was the result of this 13.25% interest rate on inflation and the general economy? The Business Recorder assessed it almost a year later in April 2020. My summary

Credit to private sector declined by whopping 66% in 9MFY2020 on y-o-y basis

LSM in recession for 6 quarters

Share of loans to SMEs drops from 9.3% to 8.2%

High interest rates reduced repayment capacity of borrowers: financing expense touch 80% of gross profits ← companies with thin margins are not in a position to guard against recessionary forces.

NPLs that had been consistently declining since 2011, when they were 15.7%, had fallen to 8% last year. Due to the high discount rate to attract hot money, the trend reversed with NPLs inching up to 8.6% in 2Q2020

But it definitely would have had an impact on inflation, as all the experts keep harping on how higher interest rates fight inflation. Again from Business Recorder

Urban and rural non-food was a little over 10 percent when the PTI took over power in August 2018 with head line inflation at 5.8 percent in July 2018. The next three months’ prices remained sticky at 5 percent and rose to 6.8 percent in October 2018. In April 2019, the rate was 8.8 percent. From thenceforth headline inflation rose to 10.3 percent in July 2019, 12.6 percent in September and 13.07 percent in January 2020. In short, inflation appears to have increased subsequent to the induction of the current economic team and the reason can be attributed to the conditions agreed with the Fund on 12 May 2019 when the staff level agreement was reached.

The central bank linked the discount rate to CPI instead of core inflation (which removes headline inflation components that exhibit large volatility from month to month, week to week, particularly food and energy) and the SBP report claims that “easing of underlying inflationary pressures was not sufficient to arrest climbing head line inflation which was largely food inflation….the policy makers, nonetheless, anticipated only temporary impact of these food supply shocks on the future inflation path and kept the policy rate unchanged….” Such inexplicable logic, linking the discount rate to headline inflation, and then arguing that volatility in food prices was anticipated by the ‘policy makers’ (read the Monetary Policy Committee) prompting them to leave the discount rate unchanged at a high of 13.25 percent. The report further adds that “interest rates also seemed appropriate to the MPC to bring the inflation rate down to the target range of 5–7 percent over the medium term” — yet another inexplicable claim as economic activity continues to be stifled and financing instruments (notably reduced interest rates for specific sectors) on offer by the SBP were “unsuccessful in raising private credit.”

Not many people realize it, but Covid-19 had been a godsend for SBP and the government. It provided them relief and a chance to change their ways, otherwise, SBP was on its way to deepening the recession to attract and hold on to the hot money.

Over 79 per cent of all foreign investment in the country’s capital markets — including bonds and equities — has fled the country in the last 40 days.

The State Bank of Pakistan’s (SBP) latest data issued on Thursday showed the pace of outflows from the country’s treasury bills, Pakistan Investment Bonds (PIBs) and equity markets has accelerated.

During the current fiscal year, foreign investment in domestic bonds and equity markets noted an inflow of $4.144 billion, however, that quickly turned into outflows during March. The pace has continued into April as well. As of April 8, total outflows during the current fiscal year have reached $3.274bn accounting for 79pc of the total investments.

Foreign investors had in the current fiscal year rushed to buy T-bills in the wake of high interest rates investing $3.431bn. But volatility fueled by the pandemic and investors’ risk-aversion led to sudden outflows of $2.357bn in just 40 days.

If SBP ever releases data about the inflows and outflows, my guess is we will find out that the foreign investors made around double-digit returns closer to 13.25% in dollar terms on their hot money. The lollipop we were given at the time was that the borrowing is in rupees, so 13.25% isn’t that high a cost to attract hot money.

To summarize, the hot money policy of SBP

Despite claims to the contrary, it was not introduced to bring down inflation.

Led to a recession in the private sector

Increased the government cost of borrowing significantly

Resulted in higher profits for commercial banks as they continued lending to the government at higher rates

and the hot money left very quickly, at the first sign of volatility, i.e., the onset of the Covid-19 pandemic.

I should have introduced this meme at that time, but my meme game wasn’t strong then.

SBP Amendment Act - Primary Objective

I wrote a post here, here, here,here, and quite a few more. I spend more time on it than I should have. The crux of all these posts was this

It’s a shame that in the 10 months that we know of (as the first draft was leaked in March 2021 over WhatsApp) that the draft was being discussed amongst the top technocrats of IMF, SBP, and Ministry of Finance, no one questioned the primary objective description. Apparently, they just copied and pasted it from an IMF manual.

We all know how I feel about SBP’s ability to control inflation (this time I won’t share that meme). In its brief on the SBP Amendment Bill, the Ministry of Finance states that

Focusing on price stability as the primary objective is sensible since inflation is one of the variables that the State Bank can influence directly through its tools,

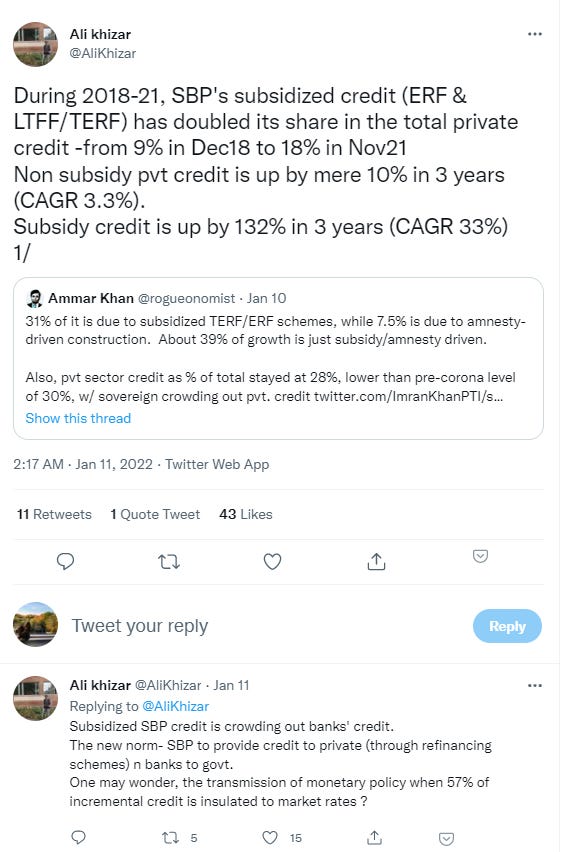

Seriously? Can SBP really influence inflation? Mortgage depth in Pakistan is one of the lowest in the world. In addition, the share of private-sector borrowing in overall borrowing is less than 30%. The majority of private sector credit growth in the last 3 years is in subsidized credit (ERF, TERF, LTFF, MPMG).

……

Should be embarrassing for those that came up with it if the first paragraph of the revised act comprises

Unclear primary objective

Allows for financial stability to be sacrificed at the altar of controlling inflation

Deletes growth as an objective yet the MoF briefs writes paragraphs on how the new objective will support growth and at one point says the growth will be prioritized over inflation.

Incoherent mumbo jumbo as the third objective.

SBP Amendment Act - Quasi Fiscal Activities and Development Finance Activities

I have spent a lot of time on this too. Under the new SBP Act, SBP cannot engage in quasi-fiscal activities (refinancing) and development finance (housing and construction financing) activities. I had harped on it quite a lot, such that reportedly it caused a stir in the market. But I was just going by what is written in the Act.

And once the SBP Act passed, we found out that what I was saying was true all along. I have no sources inside IMF, SBP, or MoF. I was just reading what was written in the Act.

IMF asking for rolling back of QFAs

The key sentences in the news report for the purpose of this post are

The IMF has also imposed the condition that by April, the Ministry of Finance and State Bank of Pakistan (SBP) will establish a Development Finance Institution to support the eventual phasing out of SBP refinance facilities.

The new institution will take responsibility for the SBP refinancing scheme, assess the Export Refinancing Scheme (EFS) by February-end and take needed actions to improve its effectiveness.

The IMF said that as of September 2021, the outstanding amount for all the SBP facilities was Rs1.22 trillion. The “staff warned that this expansion, if not temporary, would undermine the SBP’s efforts to credibly implement monetary policy, achieve its primary objective, and improve monetary policy transmission channels”.

The International Monetary Fund (IMF) has asked the State Bank of Pakistan (SBP) to “unwind” the two key measures for the promotion of housing and construction activities.

The staff report, which the IMF released along with the $1 billion tranche under the resumed loan programme, said the international lender “urged” the central bank to wind down these measures “out of concerns for financial stability”.

“Banks’ housing lending targets could present risks to financial stability and entail a misallocation of credit,” it said.

Let me again put it on record. I am all for the central bank engaging in Quasi Fiscal Activities and Development Finance Activities if the circumstances call for it. I was just pointing out that the Act that was pushed by the SBP governor did not allow for it.

As per SBP reports, the take-up of the housing finance has been phenomenal. It’s just that the SBP push for it is in violation of the SBP Act.

SBP issued a circular which allowed investment in REIT shares or providing financing to REIT to be counted towards construction finance targets. I wrote a detailed post on it. Ali Jameel of TPL Properties was about to launch the largest REIT in Pakistan and also sat on the board of SBP. This circular gave a whiff of conflict of interest.

Let’s list the steps taken by SBP in 2021 (after Ali Jameel assumed the position of director on SBP board):

Direct finance to or investment in Shares/Sukuks/TFC of REITs, by the banks, to be counted towards construction financing mandate.

Ceiling of 15% : banks can meet up to a maximum of 15% of the prescribed mandate by investing in shares/Sukuks/TFCs of REITs or providing financing to them.

Investment in REIT shares by banks to be categorized in “banking book” instead of “trading book”.

Risk weight of banks’ investment in REIT shares reduced from 200% to 100%.

As per SBP press release, Prudential Regulations revised to allow banks/DFIs to invest up to 15% of their equity (as against the earlier limit of 10% of their equity) in REIT shares.

Ceiling raised to 25% of the mandate.

Doesn’t it make you wonder if SBP is playing the role of REIT Promotion Authority?

Mystery shopping

This is my favorite anecdote where the SBP governor tries to please the PM by saying housing targets are being met when just a day before Pakistan Bank Association had sent out an email to all banks on their dismal performance in housing finance.

During the meeting of the NCC on housing, State Bank of Pakistan (SBP) Governor Reza Baqir said that banks had almost met their quarterly targets of house loan disbursement.

He said that more than 100 officials of the SBP conducted “mystery shopping” by visiting different banks on a daily basis to ascertain the on-the-ground situation and monitor the facilities being provided to house loan-seekers.

Yet when I looked at data on the SBP website on that date, all the increase is coming from banks extending loans to their staff, which makes you wonder what are the mystery shoppers of SBP reporting. Is everyone from top to bottom at SBP in on the misrepresentation? As per RB, 100 officials conducted mystery shopping. Did none of them report that banks aren’t lending to consumers? Or was RB making stuff up in front of Imran Khan?

Housing Finance Data

If you think the data is dated, I have another piece of information that confirms what I have written. This was the email sent out by Pakistan Banking Association to member banks on December 2, one day before the statement by the SBP governor.

You can feel just how much pressure the SBP governor is under. He knew a day ago that banks aren't meeting the target but conveyed otherwise to the PM the next day.

Construction Financing Statistics

I have written quite a few posts about how SBP is manipulating construction financing statistics. This is from my last post on this topic.

The reality is that there is a collusion between the banks and SBP here. Commercial banks are incentivized to report higher construction financing, and SBP has provided the banks with a number of loopholes to achieve it. SBP will not look at it too closely, as SBP wants to be in the good graces of the PM by claiming that it has achieved what it set out to do by announcing the target. No one has an incentive to verify whether actual construction financing is being financed. However, your brother isn't without resources either.

In June 2021, the Syndicated Term Finance Facility of Nishat Hotels and Properties Limited (NHPL) was closed for Rs.13.2 billion. Not a penny of Rs.13.2 billion was used towards financing new construction, rather all of it went to refinance existing long and short-term loans of NHPL.

I am not sharing the rest of the document as I believe that NHPL would want to keep it confidential as I have a soft spot for Nishat group.

Based on my “channel checks”, this Rs.13.2 billion refinancing of existing loans has been reported as construction financing by commercial banks.

Thus, when SBP claimed that the 97% target was achieved in June 2021, it was counting a transaction that is not construction financing as construction financing.

Ham-handed import compression

SBP introduced cash margin on various items to deter their imports to control the current account deficit which was increasingly looking unsustainable. The first circular imposed cash margins on 114 items and was issued in September 2021.

To summarize, SBP hopes to control current account deficit by imposing a 100% cash margin on items that comprise less than 2% of import bill. In terms of value, 25% of the items on the list comprise essential food items. Another 15% by value are such items as imported tiles, ceramics, kitchen electronics that would be a consequence of GoP’s construction amnesty and SBP’s push for construction financing and may not be affected by the cash margin at all as the end users are immune to such minor inconveniences as 100% cash margin. The rest is rubber, chemicals, paper etc. While dengue is prevalent, SBP feels that imposing a 100% cash margin on mosquito coils that comprise 0.02% of Pakistan’s import bill is beneficial.

In April 2022, SBP issued another circular listing additional 177 items for cash margin. SBP justified it in its MPS as

…widening the set of import items subject to cash margin requirements. These items are mostly finished goods including luxury items and exclude raw materials.

SBP is lying to misleading us with the last sentence. As I covered in my earlier post, almost 95% of the import items subject to cash margins comprise intermediate goods, staple food such as daal, and medicinal raw material. If there are any finished or luxury goods in the list, their share is less than 1% of the import bill.

While we can all agree that the current trade deficit is unsustainable and imports have to be compressed, using the 2021 data and SBP’s list, it appears that SBP is on the wrong path. It is deterring imports of items that lead to industrialization, electrification, and commercialization. While it is at it, it is also adding to malnutrition by making staple food expensive as well as exacerbating medicinal shortage.

COVID Stimulus

Reluctant rate reduction

As mentioned earlier Covid-19 was a godsend for SBP as it allowed SBP to change its ways. Initially, SBP wasn’t keen on reducing the policy rate. There were two reasons: 1) SBP was afraid that it will drive away hot money and 2) It went against what SBP had been saying about inflation, i.e. high-interest rates are required to bring down inflation. The first reduction was for 75bps which the SBP governor thought that it would be sufficient.

However, in a period of one month, it held two more MPCs to bring the rate down to 9%.

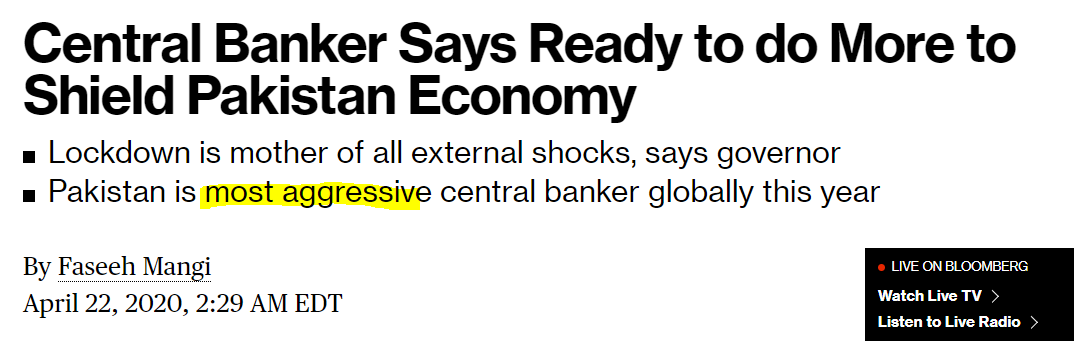

He didn’t miss a single opportunity to market himself

Even got Bloomberg to report him as the “most aggressive” central banker.

The rumor was that PM was pressurizing the SBP Governor to bring the rate down to 7%.In later March, a member of the committee Asad Zaman was asked if the rates should be lower and he thought the notion to be outrageous.

In the May meeting, when Asad was absent, the SBP governor reduced the rate to 8% by casting votes on his behalf in favor of rate reduction. Asad was surprised that a vote can be cast on his behalf when he is absent. Finally, in June 2020 MPC, the rate was brought down to 7%, a total reduction of 6.25% from the peak.

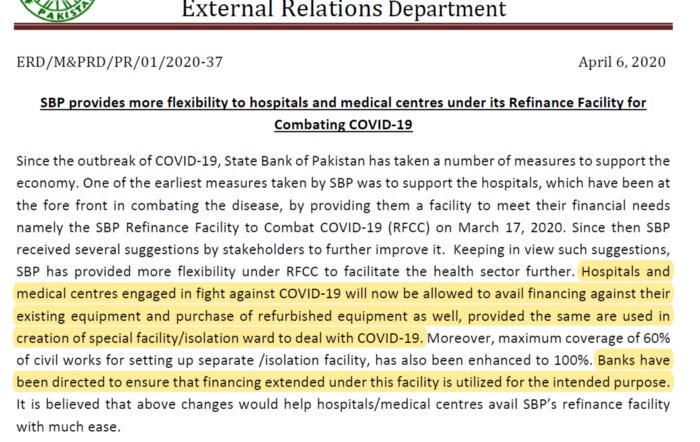

RFCC

Refinance facility for combating covid initially was a badly designed policy. The facility was revised yet even then it only allowed loans for establishing covid wards and instructed banks to ensure that the loans are used only for that purpose. Building covid wards was a loss-making proposition and banks would rather lend to known hospitals for financing expansions and upgrades.

On May 1, SBP announced that 11 hospitals have been approved for Rs.2.2 billion. In June, the restriction that the facility is restricted to Covid treatment was removed. It was open season.

Rozgar Scheme

On April 10, the SBP governor announced Rozgar scheme by putting a picture of himself on the SBP page

This was a successful scheme if we count the applications received by the banks.

As per the SBP website

It is the most popular refinance scheme of SBP which has helped to prevent layoff of 1,677,806 employees of 2,683 businesses by November, 2020. Out of these, 382,673 employees are of 1,959 SMEs and small corporates.

TERF

Who doesn’t know about TERF? Approximately Rs.435 billion have been approved under this facility for balancing, modernization, and rehabilitation of industrial units.

All in all, SBP provided Rs.2 trillion in stimuli under the various schemes.

The State Bank of Pakistan has a growing credibility problem. For the past several months, Pakistan’s central bank has been chasing an elusive inflation target.

…..Below are some quotes from the SBP’s Monetary Policy Statements with regards to its medium-term inflation outlook:

January 2020: “The MPC also viewed the current monetary policy stance as appropriate to bring inflation down to the medium-term target range of 5 – 7 percent over the next six to eight quarters.”

January 2021: “As a result, inflation is still expected to fall within the previously announced range of 7-9 percent for FY21 and trend toward the 5-7 percent target range over the medium-term.”

July 2021: “As a result, inflation is still expected to fall within the previously announced range of 7-9 percent for FY21 and trend toward the 5-7 percent target range over the medium-term.”

January 2022: “However, during FY23, inflation is expected to decline toward the medium-term target range of 5-7 percent more quickly than previously forecasted as demand-side pressures wane faster due to the Finance (Supplementary) Act.”

Personally, I don’t think raising the policy rate will deter inflation as it is not bank debt finance demand induced inflation. But that is my belief. SBP believes that raising the policy rate will hold back inflation and yet it is continuously behind the curve.

The monetary policy decision is today. The committee meeting has been preponed by a week in light of recent developments in the currency movement.

The question is: what are the unforeseen developments that could not have waited for (even) a week?

There are no visible uncertainties due to monetary policy in the capital market (both money and stock) to pressurize SBP to call the meeting earlier.

And there is no primary auction in the next week which could have enticed SBP to call the meeting earlier.

In fact, day before yesterday, a T-bill action took place and almost all market (competitive) bids were rejected.

Had the SBP not announced policy review earlier, there could have been some interest in 3M papers. The government accepted mere Rs500 million in the 3M paper at the previous auction’s cut-off yield.

The government was lucky to get Rs55 billion in non-competitive bids in 3M. Government got nothing in the 6M and 12M papers.

Reza Baqir does like his media appearances. But he really pulled out all stops in November.

The November 29 clarification is SBP complaining about op-ed writers in the newspapers

It is quite easy, in hindsight, to criticize this decision even though no tangible alternatives were proposed in the op-eds or elsewhere at the time.

Sehban had the best tweets describing the “clarification”.

Inability to restrict the import of cars

SBP tweaked the Prudential Regulations in September 2021 making it harder for consumers to borrow from commercial banks for financing cars. After the revised SBP prudential regulations, there was a significant decrease in the rate of new car loans falling down to around zero by Jan 2022. However, since then, the car loans are back and back with a vengeance. It’s as if, all of a sudden, the new prudential regulations had no impact at all.

I wrote a piece for The Profit on the recent Open Market Operations (OMOs) of SBP. The thesis of the piece was that despite SBP and the press calling the recent 63-day reverse repos as injections, they weren’t injections in the truest sense of the word as no new reserves were created by SBP. They were maturity transformations, i.e., maturing 7-day reverse repos were converted into 63-day reverse repos.

In a later piece, I summarized what these OMOs are

This caused quite a stir in WhatsApp groups. Now if he really wanted to make some noise, he could have said that the SBP backdoor lending to the government through RRPs is at the highest level. It didn’t reach this level overnight. It has been steadily increasing over the last 2 years.

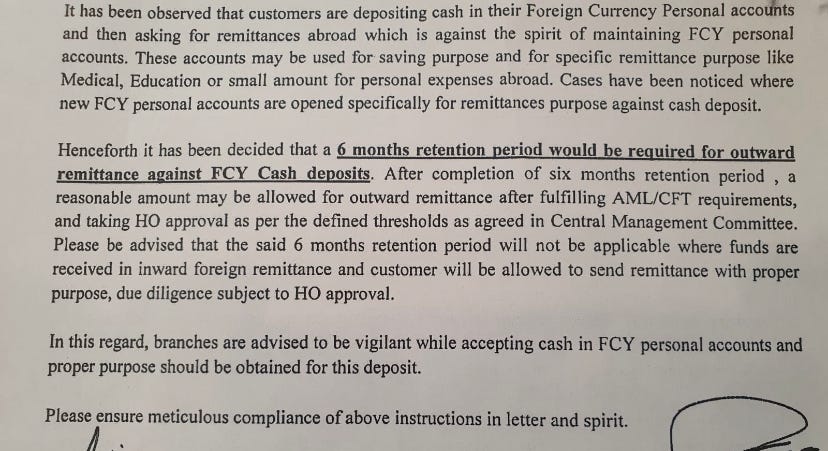

On October 6, SBP imposed curbs on the outflow of foreign exchange. Later it advised banks to restrict outflow of cash without issuing a circular

Below is a internal circular from Habib Meteopolitan Bank (HMB).

As per the circular, remitting from FCY accounts is against the “spirit of maintaining FCY personal accounts”. This is news to me that banks presume a certain spirit when opening personal FCY accounts.

The unusual thing here is that HMB isn’t the only bank doing it. Quite a few banks have imposed similar limitations of three months or six months ie FCY funds should remain in the account for a certain period before the money could be remitted abroad. As all the banks are doing it, without any formal notification from SBP and without sharing any circular or notification with the customer, this indicates that the instructions have come from above most likely SBP. Moreover, such instructions aren’t in writing as SBP doesn’t want to show that it’s panicking. But panicking it is.

And it continues to make it hard for resident Pakistanis to buy foreign currency and/or remit it.

As Motasim reminded me in the comments, SBP also engaged in chart crimes in the construction and housing finance where there was pressure from PM to show growth.

Below is the chart in the SBP press release, alongside the chart created by me using the same figures as in the SBP chart. A 75% growth is nothing to sneer at. That’s why I find it intriguing that SBP felt the need to engage in chart crime to make the point.

Chart Crime

If SBP is saying that targets have been achieved, then we will have to believe it. However, it is disconcerting that SBP is claiming the 97% of target achieved on July 15, 2021, when only a week ago, on July 7, SBP was threatening the banks with a penalty.

The State Bank of Pakistan (SBP) has decided to impose penalty on banks if they fail to meet the mandatory targets for the number of houses and disbursement, said a circular issued on Tuesday.

It appears that the banks are still reluctant to extend loans for the low-income housing projects or houses creating frustration among the government’s top ranks. The government’s prime agenda was to provide 10 million jobs and 5 million low-income houses but after three years, there is no visible sign in this direction.

Outlasted 3 finance ministers and 4 finance secretaries

Like any central banker, he got things quite a few things right and and some of the things wrong. Unlike other central bankers, he is a populist. However, it wouldn’t be the end of the world if the government renews his term for another 5 years.

A friend asked me few days ago, when news was circulating that his term won’t be renewed, how do I feel about it. I replied that I am ambivalent, people come, people go. This substack, however, exists because of him.