The State Bank of Pakistan (SBP) has granted approval to MCB to commence the due diligence process as it eyes to acquire 55% sponsor shares in Telenor Microfinance Bank (TMB).

The development comes days after the central bank also granted in-principle approval to the United Bank Limited (UBL) to commence the due diligence of Telenor Microfinance Bank Limited for the proposed acquisition of 55% sponsor shares in TMB.

Introduced as branchless banking, being a pioneer with the brand of Easypaisa, Telenor Bank has expanded its businesses countrywide with innovative services. According to the financial statement, the bank earned a gross profit of Rs 1.245 billion by the end of September 2021.

BR states (bolded above) TMB earned a gross profit of Rs.1.245B by end of September 2021. It must be a typo as Net Interest Income is Rs.1.327B. The net interest income, however, doesn’t depict a true picture if the bank incurred a loss of Rs.7.5 billion.

The loss is huge. It wiped out the equity of the bank. TMB had to issue the right shares of Rs.6 billion to keep its equity positive.

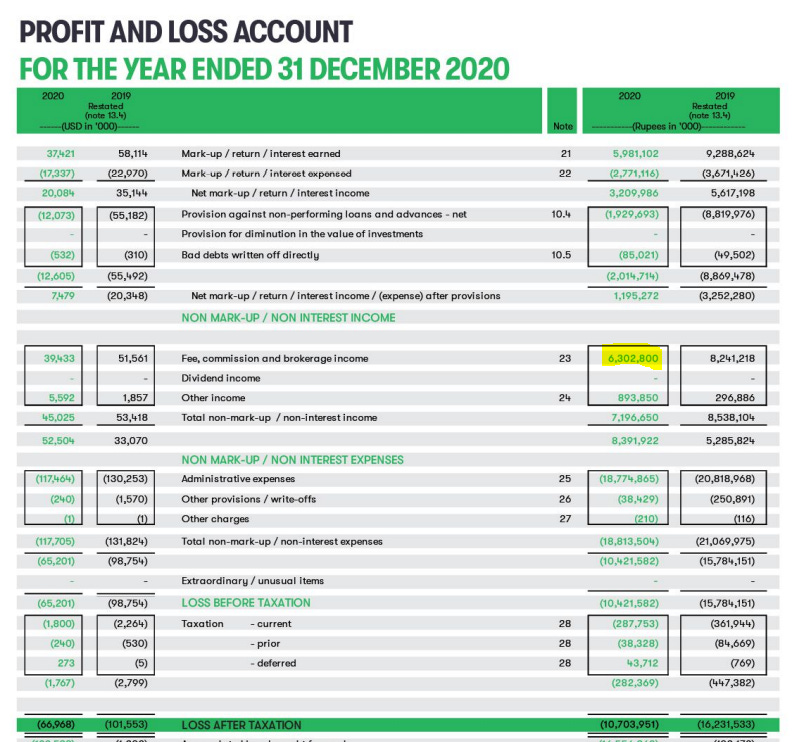

But those are unaudited accounts for 3Q 2021. Let’s look at the audited accounts of 2020 and earlier. TMB has been incurring significant losses. Rs.10 billion in 2020, Rs. 16 billion in 2019 and Rs.2.5 billion in 2018.

The Balance Sheet shows that equity of TMB was wiped out in 2020 as well and remained positive only due to Advance against Right Issue of Rs.7 billion.

After an advance against the right issue of Rs.7 billion, the total net assets come to around Rs.5 billion, i.e. without the injection, the net assets would have been negative Rs.2 billion.

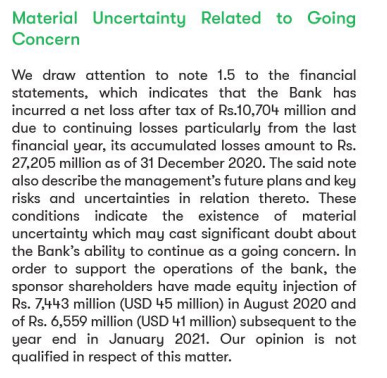

In the 2020 report, after TMB incurred Rs.10 billion losses, the Auditors raised the going concern issue.

In 2021, TMB is on track to again incur the same amount of losses. We can easily predict that the 2021 Auditor’s report will again question the going concern nature of the business.

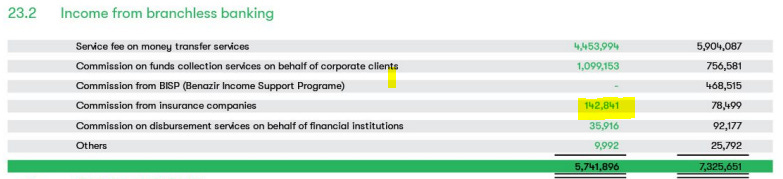

Looking again at the 2020 income statement, TMB earned Rs.6 billion from fees and commissions.

Almost 70% of this income comprises income from money transfers. However, after the introduction of RAAST free transfers, this income will go down to zero.

The 3Q 2021 financials don’t provide a breakdown of the fee income, but we can presume a similar proportion in 2021.

Thus, in the absence of money transfer income, the loss of TMB would have been Rs.14 billion in 2020 and most likely, will be the same amount for 2021.

With such a bleak outlook of TMB business, it is surprising that both UBL and MCB are interested in this business. UBL can’t even claim that it has expertise in the microfinance lending sphere. I highlighted in my earlier post, that among the major banks, UBL has the least expertise in making advances and the smallest proportion of its assets in advances.

On an unrelated note, UBL should get out of banking business and become a mutual fund (fixed income or money market) if 75% of its assets comprise investments and liquid assets

Both MCB and UBL are micromanaged by their owners, Mian Mansha in case of MCB and Zameer Chaudhary in case of UBL. There is no reason why UBL/MCB should be considering buying a loss-making entity that is also losing access to its largest source of fee income to RAAST.

The only reason MCB and UBL are considering the acquisition of the stake in TMB, this is pure speculation on my part, is that SBP may be putting pressure on them to acquire TMB otherwise TMB will have to be liquidated as their current sponsors aren’t interested in plowing in more money in this business.

There is an opportunity to increase bancassurance income. I wrote in the previous post that both MCB and UBL are most aggressive with respect to questionable practices of selling bancassurance. However, I don’t know if there is enough income in the bancassurance business to justify for UBL/MCB to enter this business. If MCB/UBL does buy it to push bancassurance, it will be a tragedy for the microfinance borrowers that a wealth-destroying product will be shoved down their throats in the name of financial inclusion.