US Government in Pinstripes : Housing

The role of the US government-sponsored Federal Housing Agency (FHA) in increasing the homeownership rate in the US

This post is atypical of the kind of stuff I post here.

I had written this post soon after Asad Umar was fired as finance minister. At that time, I was keenly following housing developments in Pakistan. It was continuously being mentioned that Pakistan has one of the lowest mortgage depths in the world at 0.2% as banks do not step into this space. Being a finance person, I wanted to research what makes the US financing markets such a large player in housing. Is it just the foreclosure law? The general perception is that the US is the most sophisticated housing market in the world where deep and liquid financial markets comprising of the private sector players are financing the homeownership, a pillar of the American Dream. I learned that the private players may be big in slicing and dicing the mortgages into MBS, and then buying and selling those securities, but the foundation of mortgage finance in the US rests on the US federal government-sponsored Federal Housing Agency (FHA). Now that the original blog does not exist, I am copying this post from my drafts here. This post is about FHA and its role in increasing homeownership in the US.

The government of Pakistan launched the Naya Pakistan Housing Program (NPHP) with the intention to build 5 million housing units. The government is having a hard time delivering on it as the government bureaucracy does not have the capacity to deliver on the housing promises. The job has become more difficult for the government after it agreed to the latest IMF program as one, a significant slowdown is expected in the rate of growth of the economy, two, construction costs of material and interest rates have risen significantly, and three, soaring inflation has reduced the capability of low-income buyers to afford the housing units.

Furthermore, the carrot and stick approach that the government is employing with the banks to encourage them to offer mortgages to low-income groups to buy these so far unbuilt housing units is not showing any signs of working. The government dangled, in front of the banks, a carrot of low regulatory reserve requirements and lower taxes on interest income derived from mortgages offered to low-income borrowers. The banks refused to bite. The stick of imposition of fine, which the now sacked finance minister (I am talking about Asad Umar here when the original post was written) jokingly threatened the banks with, didn’t make them budge either. A clear case of market failure.

While continuing to read up on affordable housing, I came across Devon Zuegel’s post Subsidizing Suburbia (recommended reading) on the US Federal Housing Agency (FHA) and I went down a rabbit hole of books, papers, and blogpost to research FHA further. It is a common misperception that the factors behind the depth and vibrancy of the US housing market are Fannie Mae, Freddie Mac, securitization, and MBS (mortgage-backed securities, not Mohammed Bin Salman). In fact, it is FHA that laid the foundation of US housing and US housing finance and it was the continued involvement of FHA that led to its growth and sophistication. This post summarizes my research into the history and workings of FHA. The post does not consider if an FHA-like agency is replicable in Pakistan or what are the legal/constitutional/financial pre-requisites of creating such an agency in Pakistan.

Hoover’s FHLB

From 1928 to 1933, during the Great Depression, residential property construction in the United States fell by 95%. In 1930, there were 150,000 non-farm foreclosures, followed by an additional 200,000 non-farm foreclosures in 1931.

President Herbert Hoover convened President’s National Conference on Homebuilding and Homeownership in 1931. Over 40 specialists attended the conference and joined its various working committees. The conference made four recommendations:

Creation of long term amortized mortgages

Reduction of interest rates on mortgages

Government aid to the private sector for creating housing for low-income households

Reduction of construction costs for housing

Liberal economist Richard Eby tried to mollify businessmen that members in his committee (one of several working committees at the conference) were “unanimous in their opposition to the construction of homes with public funds”. But those in the real estate business were more worried about their own survival than with any particular political ideology. Republican Secretary of Interior, Ray Lyman Wilbur went as far as to say that if private capital did not invest in technically innovative large-scale residential building operations to take on the housing challenge then “housing by a public authority is inevitable”. Such a heretical statement from the Republican administration in 1931 yet it didn’t cause a ripple, is an indication of how low the confidence was in the private sector and its capability to make it through the crisis. National Association of Home Builders (NAHB) took the position that private builders cannot build affordable homes without government support.

Hoover was ready to experiment. On July 22, 1932, Hoover signed into law the Federal Home Loan Bank Act which created Federal Home Loan Bank (FHLB). FHLB established a credit reserve for mortgage lenders to increase the supply of credit in the housing market. FHLB received 41,000 applications from homeowners but due to bureaucratic red tape, only 3 were approved. The economic conditions continued to worsen with additional 250,000 non-farm foreclosures in 1932. By the spring of 1933, half of all mortgages in the United State were underwater with the foreclosure rate reaching 1,000 per day. The act and the bank had failed to revive the housing market.

FDR’s New Deal

HOLC

Unlike Hoover’s short-lived FHLB, two innovations of FDR’s New Deal, Home Owner’s Loan Corporation (HOLC) and the Federal Housing Authority (FHA) have had a permanent and lasting impact on the housing market. HOLC was created on June 13, 1933, through the Home Owners’ Loan Act of 1933. HOLC refinanced tens of thousands of mortgages in danger of defaults and/or foreclosure. It even gave low-interest loans to permit homeowners to recover homes lost to foreclosure. Between July 1933 and June 1935, HOLC provided $3 billion for over a million mortgages.

“Probably no single measure consolidated so much middle-class support for a new deal [than the creation of HOLC]”.

HOLC is important because it introduced, perfected, and proved in practice the feasibility of self-amortizing mortgages with equal payments throughout the life of the mortgage. HOLC used long-term bonds to acquire mortgages in default and then rewrote these mortgages on more affordable terms. Before 1929 in the US, the typical term of a mortgage loan was between 2 to 11 years. Saving and Loans (S&Ls) provided mortgages for 11 years. Mortgages issued by insurance companies had a term of 6 to 8 years and commercial banks 2 to 3 years. Naturally, when the loan matured, the loan had not fully amortized forcing the homeowner to arrange a renewal/refinance. Thus every few years, the homeowners would be scrambling to renew/refinance their mortgage. Under HOLC, loans were fully amortized and the repayment period was extended to 15 years thereby reducing monthly payments. What is now a norm in housing finance i.e., fixed-rate, long-term, self-amortizing, and low down payment mortgages was virtually non-existent before the mid-1930s and HOLC.

Aside from the large number of mortgages that HOLC refinanced for the long term at low-interest rates, HOLC systematized appraisal methods across the country using questionnaires relating to income, occupation, age, ethnicity, type of construction, price range, and sales demand, etc. Appraisals were being carried out before HOLC too but HOLC created a formal uniform system that was implemented by individuals only after intensive training. It single-handedly improved the appraisal methodology in the US.

Federal Housing Agency

No agency has had a more lasting impact on homeowners, builders, and mortgage lenders than the FHA. It was created as FDR wanted at least one program that stimulated the private sector to build without government spending. FHA was established through the National Housing Act on June 27, 1934. The primary purpose of the legislation, however, was the alleviation of unemployment which stood at about a quarter of the total workforce in 1934 and particularly high in construction industries as “the fundamental purpose of this [FHA] bill, is an effort to get the people back to work”. It was intended “to encourage improvement in housing standards and conditions, to facilitate sound home financing at reasonable terms, and to exert stabilizing influence on the housing market” as per Mariner Eccles, special assistant to Treasury Secretary Henry Morgenthau Jr. who drafted the National Housing Act 1934 that led to the creation of FHA.

Title II of the National Housing Act 1934 authorized FHA to “provide a system of mutual insurance” by creating Mutual Mortgage Insurance Fund (MMIF) for both mortgages on single-family homes and on apartment projects having at least 5 units.

FHA is a government-run mortgage insurer. It doesn’t actually lend money to home buyers but insures the mortgages made by private lenders as long as the loan meets the strict size and underwriting standards. In exchange for this protection, the agency charges upfront and annual fees, the cost of which is passed on to the borrower. FHA induces lenders who have money to invest it in residential mortgages by insuring them against losses on such loans with the full weight of the US Treasury behind the contract. With FHA insurance, mortgage lenders were protected from default; if the borrowers failed to keep up with their mortgage payments, the FHA would cover the unpaid balance of the loan.

FHA runs at no cost to the government using insurance fees as its sole source of revenue. In the event of a severe market downturn, FHA has an unlimited line of credit from the US Treasury though it never has to draw on these funds.

The underwriting criteria for financing single-family homes were following

A fully amortizing mortgage with a fixed rate of 5.5%

Minimum down payment of 20% appraised value

Maximum term of 20 years

Maximum mortgage amount $16,000

Insurance premium of 0.5%

Eccles described the mechanism of federal guarantees for private loans as a device that “avoided any direct encroachment by the government on the domain of private business, but which used the power of government to establish conditions under which private initiative could feed itself, and multiply its benefits”. Evidence for FHA’s success was that private capital started moving back into residential housing construction. In 1934, housing starts were up for the first time in 8 years. Steagall National Housing Act of 1938 further eased the underwriting criteria

For homes costing no more than $6,000, maximum LTV increased to 90% from 80%

For loans between $6,000 and $10,000, maximum LTV increased to 90% for first $6,000 and 80% for remainder

The mortgage term increased to 25 years

Insurance premium reduced from 0.5% to 0.25%

Interest rate reduced from 5.5% to 5%

This led to a revolution in housing finance by:

Allowing higher LTV loans. In the 1920s, Savings and Loans (S&Ls) held one-half of US mortgages and required almost 20% down payment. FHA allowed lenders to lend at an LTV of 90%.

Reducing foreclosures. From a high of 250,000 non-farm units in 1932, foreclosures went down to only 18,000 in 1951.

Establishing minimum standards of home construction.

Reducing interest rates. The bankers did not face the risk of loan default. As a result, interest rates on the mortgages fell by two or three percentage points by freeing the lender from the costs of default and foreclosure.

FHA's Underwriting

Mortgage loan limits rather than borrower income limits have been the principal method of targeting FHA insurance activities during its history. This has the effect of focusing FHA insurance on specific segments of the market. The design standards such as a requirement that bathrooms not be accessed through bedrooms tended to limit FHA insurance to the existing dwellings but that was fine for New Deal administrators who were more interested in stimulating new construction.

FHA did much more than issue mortgage insurance. FHA required that the mortgage, the property, and the borrower meet certain requirements to receive insurance. The agency insisted that all mortgages meet its requirements of physical quality. FHA developed strict standards towards the type of properties on which it would insure mortgages. The agency also applied standards based on the location, ethnic and racial composition of the community in which the property was located. The underwriting standards included the mandate that the neighborhood be “homogenous” (racially segregated).

Many features of FHA were designed to introduce greater prudence rather than more liberal standards to broaden the base of homeownership. FHA required strict appraisal, new standards of construction and design, and escrow of tax and insurance payments.

FHA's Impact on construction and construction finance industry

FHA revolutionized the scale at which suburban developers worked. Home loans become so desirable that lenders actively sought bigger and bigger projects to bankroll. As soon as the development was approved by FHA for mortgage insurance, lenders eagerly advanced cash to builders to get the housing units built. Savvy developers found themselves commanding virtually unlimited capital, very little of which they had to supply themselves, which enabled construction in the US at a scale previously unknown. Where a typical builder in the 1920s would have only one or two homes under construction at a given moment, a post-WWII firm would enact 100 at a time.

Once able to secure working capital, builders increased the size of their operations. Growth brought more profits. Medium size builders tended to expand while large builders grew larger still. These results weren’t coincidental. FHA “made a commitment to provide moderate cost housing production through large scale build operations”. FHA believed that mass construction leads to efficiencies, thus actively directed away federal loans from small builders and explicitly favored gigantic “operative builders” who “assume responsibility for the product from plotting and development of land to the disposal of completed units”.

Another way FHA helped modernize and subsidize the industry was by providing builders with research services, something which even the largest builder could rarely afford on their own. Thus FHA established design standards, projected demand in different areas, and undertook planning studies to make sure that proposed housing was coordinated with utilities, transportation, and schools.

Costs decreased as a result of FHA coordination by 13% in 1940 compared to 3 years earlier. “Probably the most important factor in this decline was a shift of FHA financing from houses catering to high-income classes to medium-priced dwellings”.

Secondary Mortgage Market

FHA-insured mortgages led to the creation of a secondary market in mortgages. Whereas S&Ls financed mortgages out of their deposits, FHA mortgages were also financed by non-depository institutions. Individual brokers and independent mortgage companies would use borrowed funds to finance FHA-insured mortgages. They would then sell these mortgages to other institutions mostly insurance companies and Fannie Mae (from the 1930s to 1940s, life insurance companies were dominant investors in FHA mortgages. Thereafter, Fannie Mae became more important).

FHA's Impact on suburban design

FHA’s minimum construction standards reduced the statistical probability that the unit will suffer from structural and mechanical defects. The standards were innovative in two respects. One, these standards were objective, uniform, and in writing, and two, they were enforced by actual on-site inspection at various fixed stages of the new housing units. Since WWII, many private builders have built housing to FHA standards even if they don’t take FHA loans. This is because many buyers will not buy a house if it does not meet FHA standards. A developer might sell just a few houses in subdivision through FHA but only if the whole division met federal standards. As a result, FHA ideas quickly became the standard among US housing.

FHA set up structures to reward certain activities. For example, FHA wanted to encourage a particular type of land use patterns that the agency believed would help safeguard residential property values such as uniform setback of houses from streets, cul-de-sac roads, and residential neighborhoods separated from commercial districts. Developers generally complied because those whose plan conformed to agency standards were able to get an advance commitment that FHA would insure mortgages for all the homes they built. Such a commitment made it easier and cheaper for developers to secure funding since lenders were sure beforehand that such sales will be quick and profitable. In this way, the agency was able to influence planning standards throughout the country.

Even the most modest of FHA insured tracts supplied shelter that met or exceeded standards of adequate ventilation, running water, and flush toilet which seemed impossible at mass level in the 1920s at an affordable price. This was possible only because of massive federal support of road construction and financial market reorganization.

Construction starts and homeownership

The above changes resulted in a significant increase in the number of families that could qualify for and afford a mortgage and be on a pathway to homeownership. Starting from 93,000 housing units in 1933, starts rose to 332,000 in 1937, 399,000 in 1938, 458,000 in 1939, 530,000 in 1940 and 619,000 in 1941. After WWII, the numbers became even larger. By 1972, FHA had helped around 11 million families to own houses and another 22 million to improve their properties. From 1934 to 1972, the homeownership rate went from 44% to 63%. Almost one-fourth of new houses in the US during 1940-the 1960s received FHA subsidy with a high point of 40.7% of households in 1955.

Despite steps to make the FHA program accessible to home buyers of more modest means, for the first two decades, it was oriented towards new construction and only a small proportion of loans were given to low-priced properties and high-risk borrowers. However, by the 1970s, the prices of FHA insured loans and incomes of homeowners with those loans were below the overall median.

DOWNSIDE (redlining)

There was a downside to FHA too. FHA led to the decay of inner cities. This happened because one, FHA preferred single-family homes as opposed to multifamily buildings, two, the loans for the repair of existing structures were small and for a short duration and three, FHA instituted a neighborhood rating mechanism which rated houses located in existing racially or ethnically diverse neighborhood negatively compared to new suburban subdivisions. The result was a move of white middle-class homeowners to the suburbs. So on one side, FHA helped millions of white middle-class and low middle-class households to become owners in racially homogenous cookie-cutter suburban neighborhoods, and on the other hand, it led to the death of inner cities and limited funding to multi-family or mixed-use or non-standard house financing. To put it bluntly, FHA deemed properties located in predominantly black neighborhoods too risky to warrant mortgage insurance.

Profitability

From its inception till 1954, FHA insured 2.9 million mortgages with an aggregate principal of $18.3 billion or an average of $6,300 per property. Through Dec 31, 1954, FHA foreclosed on 9,253 properties. FHA acquired 5,712 of these properties and paid insurance claims on them. Of the 5,712, 5,282 had been sold by Dec 31, 1954, with a net loss of $3 million or an average of $562 per property acquired and sold. From its inception till June 30, 1954, MMIF had an income of $494 million and expenses of $246 million.

FHA in 21st Century

During economic downturns in an area, conventional lenders not only increase prices (interest rates) they also engage in credit rationing i.e. reduce the number of mortgages underwritten. FHA by maintaining positions in all markets provides liquidity and stability in markets experiencing a recession. Credit rationing in conventional lending is considered a market failure in economic parlance. FHA’s ability to address this failure is a key justification for FHA’s historical and current role in the market.

During normal economic times, FHA focuses on borrowers with low down-payment loans namely first-time home buyers and low and middle-income families. During market downturns, lenders rely on FHA to keep mortgage credit flowing, meaning the agency’s business tends to increase. Through this countercyclical support, the agency is critical to providing stability to the US housing market.

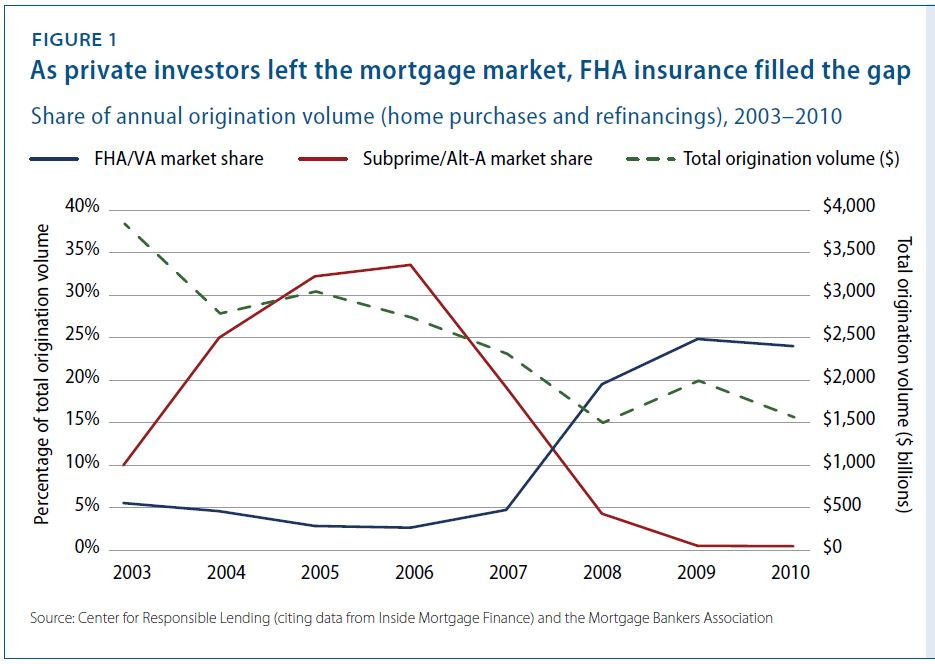

In the late 1990s and early 2000s, the mortgage market changed considerably. New subprime mortgage products backed by Wall Street capital emerged, many of which competed with standard mortgages insured by FHA. These products were poorly underwritten and were easier to process than FHA-backed loans often translating into far better compensation for the originators. This gave lenders the motivation to steer borrowers toward higher risk and higher cost products even when they qualified for safer FHA loans.

As the private subprime market took over the market for low down payment borrowers in the mid-2000s, the agency saw its market share plummet. In 2001, FHA insured 14% of home purchase loans. By 2005, that number had decreased to 3%.

We know the rest of the story. When the bubble burst in 2008, Wall Street stopped supplying mortgages. FHA picked up the slack and by 2011 backed roughly 40% of all home purchase loans in the US.

By playing a counter-cyclical role, FHA ensured middle-class families still continued to buy homes. It backed 4 million loans since 2008 and helped another 2.6 million families lower their monthly payments by refinancing.

Moody’s Analytics estimated that if FHA had stopped business in Oct 2010, by end of 2011, mortgage interest rates would have doubled, construction activity would’ve plunged by more than 60%, new and existing homes sales would have dropped by third, and home prices would have fallen another 25% from already depressed levels. A second collapse would have sent the US into a double-dip recession, GDP would’ve declined by 2%, and another 3 million job losses with an unemployment rate up to 12%.

“[Obama admin] empowered FHA to ensure that household could find mortgages at low-interest rates even during the worst phase of financial panic,” wrote Mark Zandi, chief economist at Moody’s Analytics in Washington Post.

“Without such credit [i.e. FHA], housing market would have completely shut down, taking the economy with it.”

Mark Zandi, Moody's Analytics in Washinton Post