I ended my earlier post on OMOs outlining the 4 upcoming events in the monetary policy calendar. One of the four was

Jan 14 and Jan 21 OMOs: Does SBP continue to add to the pool of 63-day OMOs by either transforming the maturing 7-day reverse repos or injecting new 63-day repos? Does SBP expand its balance sheet, or keep it the same, or shrink it?

Against market expectations, SBP didn’t do another 63-day reverse repo (RRP) on Jan 14. SBP rolled over the maturing 7-day RRPs and increased the size by another Rs.160 billion.

Resultantly, monetary policy assets of SBP will have increased to Rs.2.2 trillion (we can confirm once the next weekly Statement of Affairs (SoA) is released), which will reportedly be amongst the highest balances of monetary policy assets (MPAs) in recent history.

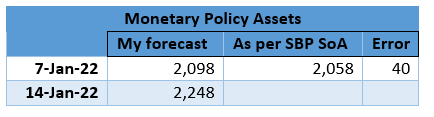

In the earlier post, I had forecasted, monetary policy assets of SBP on Jan 7 to be around Rs.2.1 trillion.

Consequently, the balance sheet size of SBP which hadn’t increased in the last three OMOs will increase by approximately Rs.350 billion after this repo. (I will update the below table with the actual number once SBP’s Statement of Affairs for January 7 becomes available).

As per SoA dated January 7, the monetary policy assets are at Rs. 2,058 billion. I was off by Rs.40 billion or 2%. Mea culpa for my forecasting abilities.

in billion of rupees

This is why I don’t give out investment advice.

Now we wait for Jan 21st OMO to see if SBP increases the amount of 7-day RRP. If it does, I think but I will have to check, it will be the highest amount of RRPs outstanding ever.

The monetary policy calendar till the end of next week looks like below:

Jan 21 - OMO: It is expected that SBP will just roll over the 7-day RRPs. No 63-day RRP is expected (see point 2 below).

Jan 24 - MPC: This is the first MPC after the “pause” statement of the SBP Governor. Naturally, the market expects that the policy rate will not be increased if SBP wants to rebuild the credibility of its “forward guidance”, which no one believes in anymore due to SBP’s earlier multiple surprise moves. SBP, however, is in a dilemma. On the one hand, it wants to maintain the “pause” because that’s what the SBP governor said SBP will do. On the other hand, every other indicator (international commodity prices, Western Central Banks planning to raise rates, exports, and travel markets opening up) is screaming for a rate rise. If SBP doesn’t raise the rate, the MPS will make for an interesting reading, as SBP will have to justify the rate pause. LSM and weak growth numbers will have to do a lot of heavy lifting to justify the pause, I think. ← I had written the bold part of the sentence before the rebased GDP was announced. With the rebased GDP numbers, there is no muted growth anymore for SBP to justify the pause in the rate. I expected SBP to build on the following statement from the Ministry of Finance brief (which MoF published in support of inflation targeting as primary objective) to justify its rate pause:

Conversely, if inflation is not because of excessive demand but because of supply shocks in the form of administrative issues that are driving food prices higher or because of increases in administered prices like electricity, growth would be prioritized and interest rates would not be raised unless these price pressures became more broad-based

(cont’d) Realistically speaking, after the rebased GDP, SBP has no choice but to raise rates in this MPC. Unfortunately, if SBP does that, this will make everyone lose all faith in SBP’s “forward guidance”. Furthermore, it will lead to higher borrowing costs for GoP in the upcoming T-bill auction (see next point), leaving Shaukat Tareen fuming once again because GoP will be Koondafied even with 63-day RRPs of 1.7 trillion outstanding. One way for SBP to satisfy all the constituencies, if it plans a rate increase at the Jan 24 MPC, is to have another 63-day or a longer RRP on Jan 21st in the hopes that the Commercial Banks, having been compensated enough with the unprecedented number of long dated RRPs, will not quote higher yields in the Jan 26 T-bill auction.

(I apologize for the length of the above point. In all the hypothesizing and game theorizing, it got away from me. Should have published this post before the rebasing).

Sorry, one more comment on the MPC and then I’ll move to the next event/point. Will the MPS following this MPC be as notorious as the last one that gave us such words as “unwarranted” and “felt”? MPC was deciding policy rates on vibes. Hahaha. Ok. I’ll stop now.

Jan 26 - T bill auction: Rs.650 billion to be auctioned, with Rs.250 billion in the 3-month category. The Jan 24 MPS will determine how it will go.

My prediction is, if SBP doesn’t do a 63-day or a longer RRP on Jan 21, then there won’t be a policy rate increase in the Jan 24 MPC. I apologize to readers who are regular money market participants and observers, as it must be just another week for them. But for an outsider like me who is just dipping his toes, this is all very exciting.

Fair Warning: This is me endeavouring to comprehend how monetary policy operations actually work in the real world. I am way out of my depth here. I am trying to extend the limits of my understanding. Just learning about stuff for the sake of learning. No other motive. Sadly, there is no investment advice here either.

I believe, and this is me speculating without any evidence, the talking points in the below newspaper report were provided by SBP. There were many interesting sentences, but these two sentences are relevant here.

By injecting enough liquidity in the money market, the SBP wants to ensure that on scheduled dates of the auctions of government treasury bills and bonds, banks do not demand unjustifiably high rates of return, making fresh government borrowing from them all the more costly.

In the absence of liquidity injection by the SBP, banks could also have taken advantage of a tight money market for making their private sector loans prohibitively pricier.

If this is how SBP feels, again I am surmising that SBP provided these talking points, the question then arises:

Why did SBP increase the policy rate at the MPC, the purpose of which, one would presume, is to increase the borrowing cost of both public and private sector, when all SBP has been doing since that memorable MPC, either by communicating through Governor’s and Deputy Governor’s media appearances or doing unprecedented OMOs, is trying to nullify the impact of the policy rate increase?