Roshan Digital Accounts: The dollars never left the US

Understanding the foreign exchange reserve balances of SBP and commercial banks

In this post, we will be building on what we learned about commercial and central bank accounting in local currency contexts in earlier posts to see how bank accounting works in the case of foreign remittances. This will help us understand the statistics of foreign currency reserves when they are reported.

In case this is your first time reading this blog and you are having a hard time following the T-accounts, I recommend you start with Issuing and managing Central Bank Digital Currencies (CBDCs) where I introduce the T-accounts for the first time. Understanding T-accounts there will make it easier to follow the transactions here.

If the T-accounts appear too small to read, click on the image and it will enlarge.

Remittance to a foreign currency account

When Asma in New York sends money from her Citibank NY (Citi NY) account to Allied Bank Limited (ABL) Foreign Currency Account (FCA) in Pakistan, dollars are not being airlifted to Pakistan in suitcases from New York to Pakistan to settle the transfer. The dollars never leave the US shores.

ABL will have a correspondent relationship with JP Morgan Bank New York (JPM NY) where it maintains a deposit/reserve/settlement account. The deposit is transferred from Asma's account at Citibank NY to ABL's account at JPM NY. ABL in Pakistan will report an increase in its dollar deposits in New York and record an accounting entry crediting Asma’s foreign currency account with an equal amount.

While Asma’s account at ABL Pakistan will show a US dollar balance of $10,000, the actual dollars are in the US in the JPM account rather in the form of reserves at the Federal Reserve.

For foreign currency transactions, all local banks maintain correspondent relationships with banks in foreign countries. The correspondent bank maintains an account with the central bank of the country. In the aforementioned example, JPM NY is acting as a correspondent bank of ABL Pakistan and maintains an account with the Federal Reserve which is the central bank of US. In the forthcoming examples, different NY-based banks will be acting as correspondent banks.

Pakistan Banao Certificate (PBC)

In April 2019, Pakistan Banao Certificates (PBCs) __ predecessor to Naya Pakistan Certificates (NPCs) __ were launched. The product was so badly designed that I had quickly turned out a post How not to launch a diaspora bond identifying the impediments that why it will not work despite lucrative returns and also suggested some improvements such as abstracting the complexities i.e. make it simple for NRPs to remit money and make the commercial banks do all the background work.

The PBC effort was being spearheaded by Zulfi Bukhari and Asad Umar and therefore its performance was disappointing. More than the product, it appeared Zulfi Bukhari was marketing himself.

I am bringing PBC up here as it was clear the dollars will remain in the US. Investors were required to register on the PBC website and generate a unique ID and ensure that a unique ID is included in data field 70/72 of the SWIFT message when they transfer the funds to SBP's account maintained at NBP New York.

National Bank of Pakistan (NBP) is the government's treasury. SBP maintains its US dollar correspondent account at NBP NY, which acts as a correspondent bank for SBP. The PBC deposit was mainly for a fixed term thus akin to a loan. SBP, however, does not recognize the loan liability. SBP credits the equivalent balance in the federal government's deposit account and it is the federal government that recognizes the liability. Reason: it is the federal government that pays the interest on these instruments.

The funds remained within Federal Reserve yet it resulted in at least three accounting entries i.e. NBP NY crediting the increase in reserves to the SBP account, SBP crediting the GoP account, and GoP recognizing the debt liability of PBC. The increase in the SBP account balance at NBP NY will be reported as an increase in the foreign currency reserves of the country.

Naya Pakistan Certificate (NPC

The NPC is being spearheaded by Reza Baqir and the performance speaks for itself.

Roshan Digital Accounts (RDA) crossed billion-dollar mark in less than eight months since its launch. The number is growing at an increasing rate. It took around eighteen weeks to get to the first $500 million, and nine for the next $500 million. It may not be too optimistic to assume that the figure may cross $2 billion within this calendar year.

Around two third of the flows are in the Naya Pakistan Certificates (NPC). These are reported in the financial account (not current account) within balance of payment as government’s debt; and within foreign reserves, these are recorded under SBP reserves.

Remaining one third is mainly used for local consumption or parked in RDAs as foreign currency – these are recorded in the current account. The amount being used locally is marked in remittances and is not repatriable, while the amount parked in RDAs is recorded as other current transfers in secondary income account. These flows are part of banks’ foreign reserves. A small portion of Rs1.5 billion ($10 mn) is deployed in the stock market.

The difference between NPC/RDA now and the earlier PBC is that the investor is transferring money to his commercial bank account in Pakistan instead of remitting money to the SBP account in NBP NY.

In the sentences that I have bolded above, the report states that when money is invested in RDA, it is commercial banks' foreign reserves. When NPCs are purchased, it becomes SBP's foreign reserves. I don't have access to operational details of how RDAs work, but based on what we have learned so far, we can try to work it out.

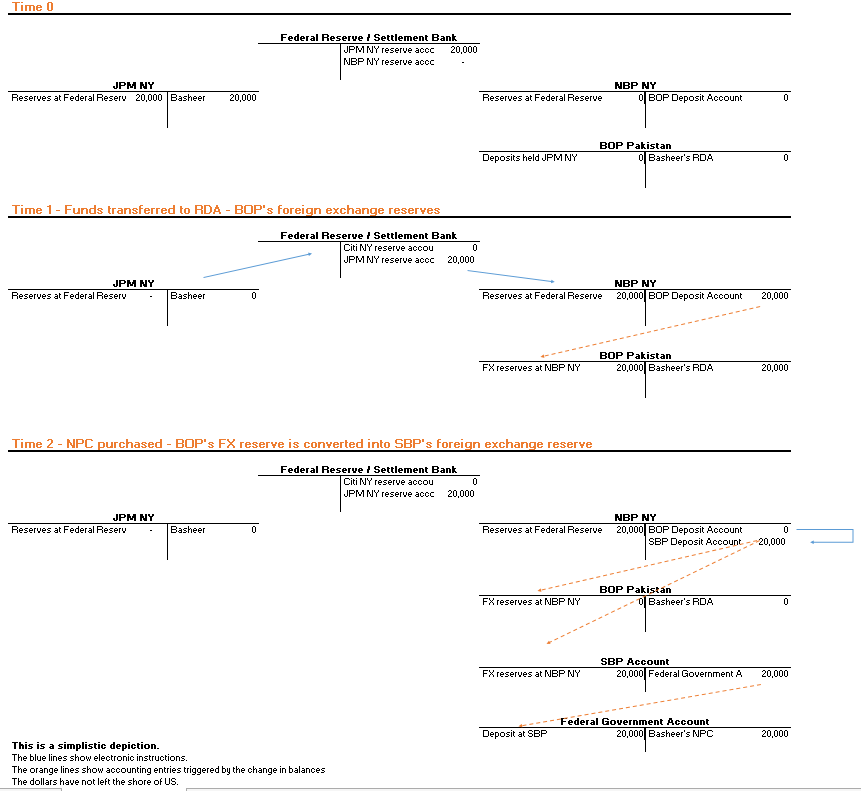

Let's assume Basheer is transferring money from his JPMorgan (JPM) account in New York to Bank of Punjab (BOP) RDA and subsequently investing in NPC. For simplicity, we will assume that BOP also uses NBP NY as its correspondent bank. It will make it easy to remit money to SBP for purchasing NPCs as both BOP and SBP now have accounts in NBP NY and the transfer can be instantaneous and costless.

When Basheer remits to BOP RDA, the funds are deposited in the BOP account maintained at NBP NY. Next Basheer purchases NPCs and the funds are transferred to the SBP account at NBP NY. When Basheer purchases NPCs, the foreign exchange reserves cease to be part of BOP’s reserves and become SBP’s foreign exchange reserves. Basheer’s RDA account balance at BOP goes to zero and federal government accounts now reflect a liability of NPC outstanding to the benefit of Basheer. As far as federal government accounts are concerned, there is no difference between PBCs and NPCs are accounted for.

Export proceeds

When export proceeds are received, the exporter is provided the funds in his local currency account by converting them to rupees at the prevailing exchange rate. The foreign exchange remains in the NY account of commercial banks whereas rupees are credited into exporters' accounts in Pakistan. The foreign exchange balance comprises the commercial bank's foreign exchange reserve.

Assume Gul Ahmed Textiles exports to Walmart. This is how the payment will flow. In this example, Deutsche Bank (DB) is acting as a correspondent bank for MCB.

When compared to the lucrative dollar returns that RDA investors in NPCs are getting, exporters are just getting rupee equivalent. No wonder exporters are asking that they should also be allowed to earn such lucrative returns. The bolded sentence hints that exporters are keeping significant dollar balances outside, away from the prying eyes of FBR and SBP, ready to bring it in if the government allows them to invest export proceeds in NPCs.

An interview with Mohammed Zaki Bashir, CEO of Gul Ahmed Textiles Limited

One example of shifting policy focus is successful launch of Roshan Digital Account. However, we must ask if these incentives are offered to expats why have similar incentives not been extended to promote the industrial and exporting base of the country?

Given RDA’s success in bringing in dollars, we advise that similar incentives and rates of returns be offered to exporters, which may help build forex reserves manifold. It may be worth emphasizing that deposits by expats into RDA can flow out any time, just like hot money. Same will not be the case for dollars received against exports.

Understandably, it may not be possible to offer these returns on all existing exports, but in order to achieve long term growth of exports and their diversification, RDA-like incentives should be offered at least to export by new sectors or to new markets.

Remittances

Remittances work exactly the same way as export proceeds. In the above chart, replace Walmart with the expat husband and Gul Ahmed with the resident wife. The husband sends the money in foreign currency. The wife gets rupees in her accounts. The foreign currency reserves of commercial banks go up.

Loan proceeds

For completeness, putting in how the loan proceeds will flow to GoP. The assumption here is that Blackrock purchases the Eurobond issued by the government of Pakistan.

Putting it all to work

SBP Reserves

Now that we understand how foreign currency accounting works, we can understand what the below press release is saying when it talks about SBP’s reserves and reserves of commercial banks.

We can also understand where and how it is reflected in SBP's accounts. The proceeds from the $2.5 billion Eurodollar bond were received in the week ending on April 9, 2021. Below is the snapshot of the weekly statement of affairs from the SBP website. The foreign currency balance on the asset side on April 9th went up by Rs.383 billion which is equal to US$2.5 billion compared to an earlier week. This is reciprocated by an increase in federal government deposits maintained with SBP on the liability side.

Commercial Bank reserves

In the first article that I quoted in this post, BR says that two-thirds are going to Naya Pakistan Certificates (SBP reserves) and one-third remains with commercial banks.

Remaining one third is mainly used for local consumption or parked in RDAs as foreign currency – these are recorded in the current account. The amount being used locally is marked in remittances and is not repatriable, while the amount parked in RDAs is recorded as other current transfers in secondary income account. These flows are part of [commercial] banks’ foreign reserves. A small portion of Rs1.5 billion ($10 mn) is deployed in the stock market.

RDA accounts are opened under SBP's FE-02 circular as Foreign Currency Value Accounts

In order to facilitate the non-resident Pakistanis as well as resident Pakistanis, who have assets abroad duly declared with Federal Board of Revenue (FBR), for investment in foreign currency denominated government registered debt securities on repatriable basis, it has been decided to introduce a separate category of foreign currency account. Accordingly, a new para 8A has been inserted after para 8 in the Chapter 6 of the FE Manual as under:

8A. Foreign Currency Value Account (FCVA)

i) Authorized Dealers may open ‘ Foreign Currency Value Account’ of the following:

A non-resident individual Pakistani;

A resident individual Pakistani who has duly declared assets held abroad, as per wealth statement declared in latest tax return with Federal Board of Revenue (FBR).

Below is the position of Commercial Banks' foreign currency deposits and borrowings from abroad. The balance in FCVAs (in green) is $86 million as of March 21. Thus these are the deposits in RDA accounts that have not been converted to rupees or used to purchase NPCs.

Bonus Feature: More leverage for investing in NPCs

Roshan Digital Accounts are so lucrative deal that both Pakistani and international banks are offering leverage to deposit holders abroad to invest in RDA. SAMBA went to the extreme of offering a 10x leverage that I had to wonder if it is hot money as masquerading as trust reposed by overseas Pakistanis in the economy of the country. I shared a few slides from HBL Asset Management’s slide deck that HBL sent out to High Net Worth Individuals. Below is a copy of an email that UBL is sending out to its valued clients.

The below is a tip I received with respect to HBL Bahrain. The scheme follows what was there in the HBL slide deck.

If you live abroad, have an account with UBL, HBL, or SAMBA, and have not received one of the aforementioned communications, I hate to break it to you, but they do not deem your networth worthy of these offers.