Pak Kuwait Investment Company and State Bank of Pakistan: Backdoor lending to Government of Pakistan

"Out of the box" government borrowing

In case you missed them, I shared bylines on three pieces in The Profit in May 2023. Do read.

Pretty outside, ugly inside: How Pakistani banks window dressed their books to avoid new taxes

Khushhali bank to force convert its hybrid debt into equity. But is it fair?

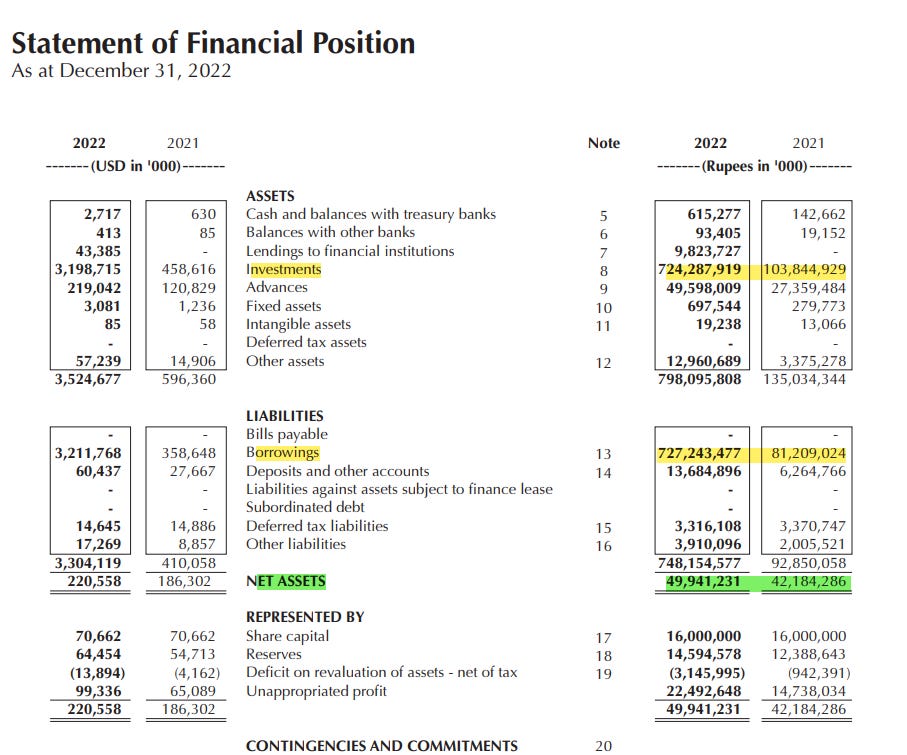

This piece will be slightly on the nerdy side and follows from the first two links above. The balance sheet of PKIC increased by 6-fold in 7 months.

If you have read the above pieces, you know that it was achieved through a circular Ponzi scheme i.e., purchasing TBills/PIBs, pledging those with Bank/SBP to borrow money, using the borrowed money to buy more TBills/PIBs and continuing with this cycle.

Are you wondering what happened in 2022 that made PKIC go on this borrowing binge?

It was SBP’s DMMD (Domestic Market & Monetary Management) Circular No. 11 of 2022

June 7, 2022

Please refer to DMMD Circular No. 12 of 2017 in terms of which all Schedule Banks and Primary Dealers are allowed to participate in Open Market Operations (OMOs).

It has been decided to allow Development Finance Institutions (DFIs) to participate in OMOs with a view to facilitate them in their liquidity management. Accordingly, DFIs would also be eligible to participate in OMOs as per instructions and procedure for OMOs stipulated in above referred master circular.

All other instructions on the subject will remain unchanged.

The circular clearly mentions (I have put it in bold font in case you missed it at first glance) that the DFIs are allowed to participate in OMOs for liquidity management.

The circular was issued on Jun 7, 2022, and by December 31, 2022, PKIC had increased its balance sheet by 6x. All this increase is the circular Ponzi OMO as evident from the balance sheet. The equity/Net Assets (in green) of PKIC barely increased in 2022 while the Investments and Borrowings (in yellow) increased by 6+ times.

Did no one, and I mean no one, at SBP thought to question PKIC what sort of “liquidity management” is this that PKIC’s borrowing went from 2x of net assets in 2021 to 15x of net assets? Did no one at SBP’s money market desk raise an eyebrow when a DFI was at their borrowing window every week borrowing larger and larger sums?

It was hinted at in the Profit piece but I want to be explicit here:

The purpose of this DFI “liquidity management” circular, DMMD Circular No.11 of 2022, is to open a backdoor for SBP to lend to the Government of Pakistan.

There is no “liquidity management” here. SBP is lending money to PKIC to lend to the Government of Pakistan by purchasing GoP securities. This is not the first time SBP is resorting to such backdoor tactics but the magnitude this time is eye-popping.

On the nerdy side, this raises an interesting question. If DFIs are allowed to participate in open market operations for “liquidity management”, can other corporates and even individuals also participate in OMOs?

There are two prerequisites.

One, the corporate or an individual be allowed to open an account at SBP. Section 17 of the SBP Act defines the business that the bank can transact and subsection 1 says that SBP can accept deposits of “other persons” which I would presume to mean both a legal person (a company) and a natural person (an individual).

The accepting of money on deposit from, and the collection of money for the Federal Government, the Provincial Governments , Local Authorities, banks and other persons: Provided that no interest shall be paid on deposit received from the Federal Government, a Provincial Government, or a Local Authority.

Two, SBP should not be restricted to scheduled banks for carrying out open market operations. As we have seen in the case of PKIC, all that was needed was a circular to allow SBP to start dealing with DFI and voila, PKIC and SBP went on a Ponzi binge. Section 18 defines how SBP can engage in OMOs

Open Market and Credit Operations

[SBP] may operate in the financial markets by — (a) buying and selling outright (spot or forward) and conducting repurchase agreements of Government securities purchased in the secondary market

Thus, if SBP wishes, it can engage with corporates as well as individuals for OMOs for their “liquidity management”.

So in a few years, if things continue like this, don’t be surprised when you see a circular from SBP allowing non-financial corporates to participate in open market operations for their “liquidity management” when in essence it will be just another backdoor for SBP to lend to Government of Pakistan.