I was pleasantly surprised to find out that in these times of political uncertainty, around one thousand people took their eyes off for five minutes from the minute-by-minute breaking news on the internet to read my yesterday’s post on Abhi Sukuk. A mere thousand views are good for nothing when compared to the tens of millions of views the vloggers and YouTubers are getting for their every upload, but I am glad I brought distraction in the life of a thousand people.

In the last line of yesterday’s post, I said that I will talk about PACRA soon. Let’s do it while the iron is hot and people are reading what I am putting out. I am using PACRA’s rating of Abhi but this post has nothing to do with Abhi. This is about PACRA. Without further ado….

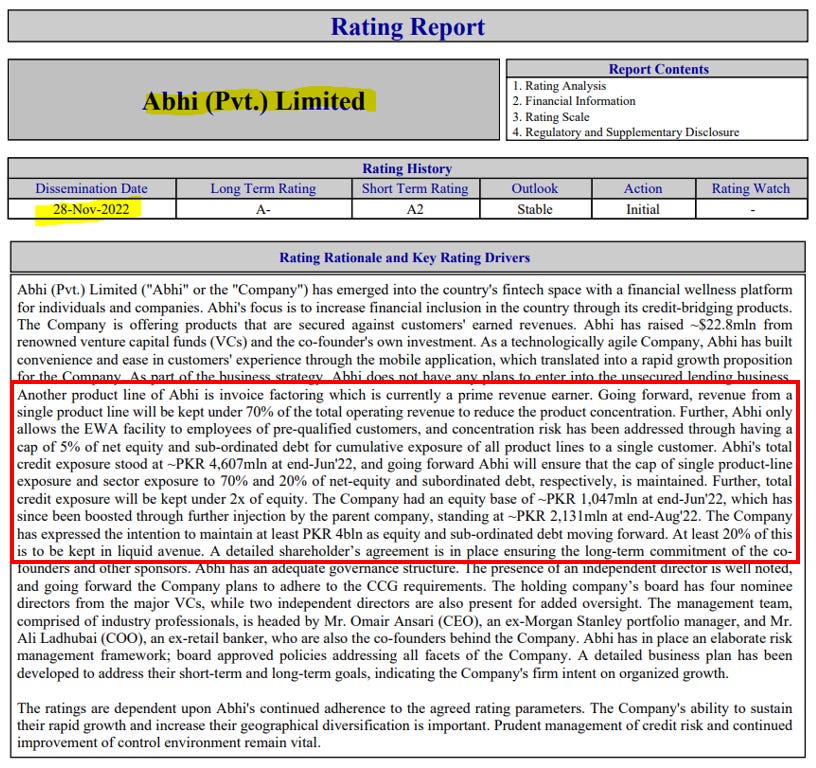

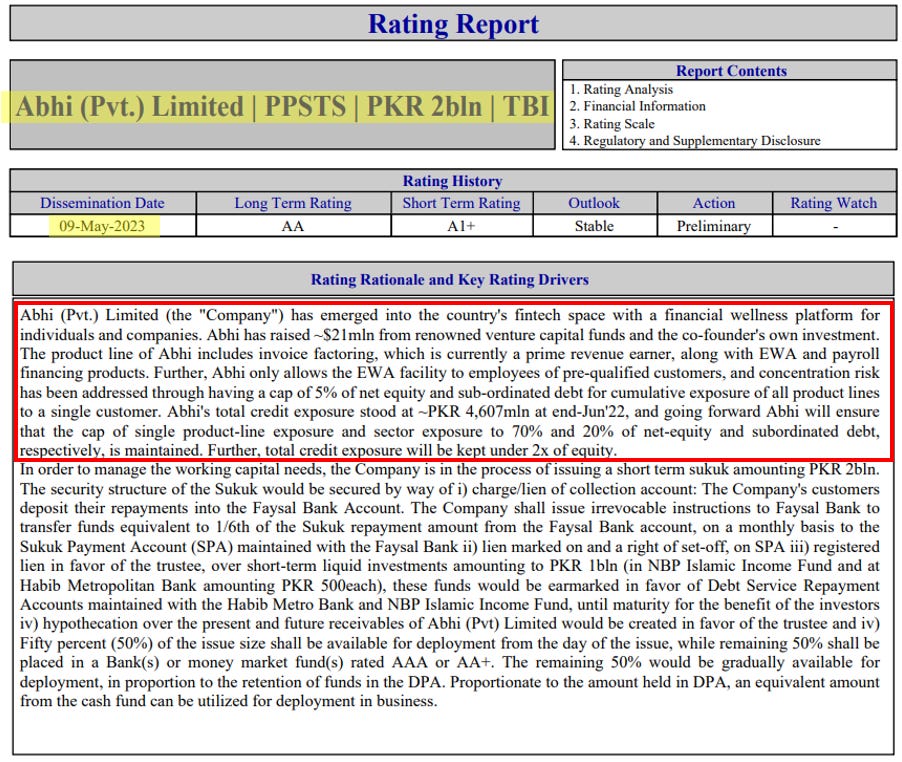

PACRA carried out a credit rating of Abhi on 28th November 2022 wherein PACRA rated the entity Abhi Private Limited and five months later, on 9th May 2023, it rated the Sukuk issued by Abhi. I have pasted the snapshot of the first page, which carried the rating rationale, of both the reports below. The rating drivers are enclosed in red boxes. There is no difference between the two reports. PACRA just copied and pasted what was written in the last report into the new report without any update.

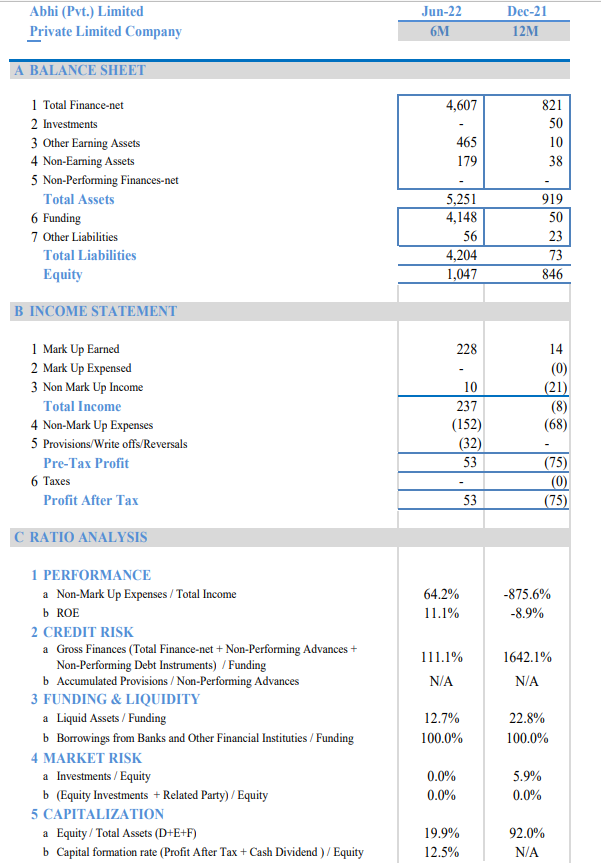

Five months have passed since the last report, is PACRA still working with the old financial data for generating a new report? The answer is a resounding yes. Both reports use the below financial statements from June 2022.

It behooves PACRA when it is issuing a rating to ask for new financials even unaudited ones. In these times of high inflation and political uncertainty using 11-month-old accounts to analyze a company (or in this case just copy-pasting the previous analysis) and that too based on half-yearly accounts is just being lazy. The company’s balance sheet grew more than 5 times during the six months i.e., total assets increased from Rs.919 million in December 2021 to Rs. 5,251 billion in June 2022. It can be safe to assume that the growth would have continued at a similar pace in the following six months. Even if it didn’t, such rapid growth is usually (but not necessarily) accompanied by higher loan losses (nature of the business) which may not have come to the surface in the June 2022 financials but would have broken the surface in the December 2022 financials. There are Rs.32M loan provisions/write-offs in the June 2022 financials. Provisions/write-offs are lagging indicators. If considering what is happening on the inflation, fx, and political front, there is a high probablity that provisions/write-offs would have been significantly higher. Using 11-month-old financial statements to issue ratings is downright incompetent.

Abhi Private Limited, I would have presumed, isn’t a very complicated and large business that auditors or accountants were having a hard time finalizing the financial statements. All PACRA to get the financials was to just ask. Not getting updated financials for a small company is a red flag.

With respect to the Sukuk, we discussed in yesterday’s post that the investors don’t care about the performance of the company as the cash flows are ring-fenced. I can now bet that none of the investors bothered to read the rating report beyond the rating assigned to the instrument.

The general perception I had about Abhi based on the PR I get was that it is in the payroll financing business. This misunderstanding is my own fault as I may have been selectively reading the PR statements. From the PACRA rating report, I find out that invoice factoring is the main revenue source of the company.

The product line of Abhi includes invoice factoring, which is currently a prime revenue earner, along with EWA and payroll financing products…. and going forward Abhi will ensure that the cap of single product-line exposure and sector exposure to 70% and 20% of net-equity and subordinated debt, respectively,

The key word is going forward, implying that the June 2022 financials that PACRA used to carry out the rating, and invoice factoring comprised in excess of the 70% threshold. Most likely, PACRA assigned the rating getting a commitment from Abhi that the exposure will be brought within these limits (I am hypothesizing here). As per PACRA, this ratio is a key rating driver. All the more reason for PACRA to ask for updated financials to see if the company is following through with the commitment.

Both November 2022 and May 2023 rating reports have the exact same phrases when it comes to risk.

Industry Dynamics: The business environment during CY22 has remained challenging so far. The high inflation has squeezed the purchasing power of consumers, and the cost of doing business has also increased. While the economy is largely suffering, Abhi has managed to onboard a significant clientele owing to the fact that the products are designed to provide relief to the users.

To give a crude analogy, the predatory lending business grows rapidly in a challenging environment. We have discussed the SECP-approved predatory lending business a few times here (predatory lending business was SECP approved under the banner of financial inclusion). We also learned that this financial inclusion was adding to the misery of the people__ while people borrow from any means possible in an emergency, many of them do not have the capacity to repay. That is why predatory lenders use unscrupulous means to collect on their debt. Similarly, if Abhi is rapidly onboarding new clients (the balance sheet grew 5 times in half a year) in this environment, PACRA should have had an in-depth discussion in the risk section describing where the clientele is coming from, why it can’t get financing from other sources, if existing clients are borrowing large amounts as due to inflation the invoice amount has grown larger, which sectors does the clientele belong to, what is the sectoral distribution, what is the product distribution of the new clientele, what is the geographic distribution, what kind of risks the portfolio is exposed to and what are this risk mitigating factors, etc?

The closest the rating comes to addressing all this is the below fluff.

MIS: Comprehensive MIS reports are generated on a daily/weekly/monthly for review by management on a regular basis. Abhi is currently implementing Turnkey Loan Management System, a best-in-class software that automates the entire lending process.

Risk Management Framework The Company has a separate Risk Management department and has also taken on board industry experts as advisors and consultants. Together, they have managed to create robust internal processes and policies for each product category which govern limits as well as help to perform in-depth customer analysis. The addition of an internal audit function has improved the risk management and control framework further.

The liquidity and funding risk section talks about the payroll advances while the ratings driver that we discussed earlier says that the revenue driver is invoice factoring. Does invoice factoring present no liquidity and funding risk?

Liquidity And Funding Abhi presently uses and will continue to do so in the future, its capital for an advance against earned emoluments which are short-term in nature and therefore liquid and carry minimal market, and liquidity risk.

Below is the entire discussion on market risk.

Market Risk: The funding from VCs has been raised in USD terms. This exposes Abhi to the risk of PKR devaluation as the repatriation of profits would be USD. Reasonable hedging measures would help to counter this risk. Abhi invests unutilized cash in low-risk financial instruments such as T-Bills and TDRs.

One can get most of the above information from the company’s press releases and management discussions. The reason analysts read rating reports is that rating agencies have access to much more detailed information with respect to the company’s asset portfolio as well as access to management. The only thing I learned in this report is that invoice factoring is the primary revenue driver. The rest of it is fluff. One can get more information from the annual reports of listed companies with respect to portfolio quality and distribution.

I am being harsh here but I think I am being fair that it’s a good thing the report is in the form of a PDF because it is not worth the paper it is written on.

As a credit analyst at the start of my banking career, I have done more in-depth analysis and due diligence for a measly secured loan than this rating analysis, if one can even call it an analysis.