If you have been following this substack, you know SBP has taken a number of steps to cut down on car finance. It appears that the steps so far haven’t had the intended effect as like a “fool in the shower”, SBP keeps on introducing more restrictions. The latest one introduced yesterday, on May 24, one day after the Monetary Policy Committee meeting, modifying the Prudential Regulations.

July 2021

Many of you may have forgotten it but aap ka bhai remembers. To refresh your memory, it was only in July 2021 that the PTI government was facilitating car purchases to generate consumption-fuelled growth by reducing taxes and duties on cars.

The government had cut FED on all vehicles up to 3,000cc by 2.5pc while on vehicles from 660cc to 1,000cc the FED had been abolished. The GST had been cut to 12.5pc from 17pc for cars up to 1,000cc. For 1,001cc to 2,000cc vehicles, the FED was decreased to 2.5pc from 5pc and for 2,001cc to 5pc from 7.5pc. The government has also cut ACDs on all vehicles from 7 to 2pc and its notification has been issued on June 30, 2021.

September 22, 2021

Once you read the next section of Sep 23, 2021 about SBP’s change in Prudential Regulations, come back and re-read the below news item again. As they say in Urdu, Lutf dobala ho jayega. Shaukat Tarin Uncle, Ministry of Finance, Ministry of Industries and Engineering Development Board were completely oblivious of ground realities.

“We have proposed the financing scheme by relaxing interest on loans in the auto sector especially for small cars but the SBP is yet to share its strategy about the proposed plan,” an official at the Engineering Development Board said.

It may be mentioned here that the government is also yet to finalise the Auto Industry Development and Export Policy (AIDEP) 2021-26.

Earlier, during a meeting on the new five year auto policy, Federal Minister for Finance and Revenue Shaukat Tarin had directed the Ministry of Industries and other institutions concerned to prepare a consolidated policy for car financing in the country on fast track.

Though the Ministry of Industries had suggested lowering the interest rate for car financing to five to six per cent, besides offering other facilities, the finance minister had directed to prepare a comprehensive policy keeping in view the policies in other countries of the world.

According to officials privy to the matter, Tarin had also stressed to come up with innovative products for provision of car financing at reduced mark-up rate to consumers so that everyone can afford a car at flexible terms and conditions.

Kamran Khan aka Agencies ka aadmi did a program on it the same day. The tweet promoting the program is interesting as it talks about sky tearing deficit and record car imports.

Yesterday, SBP issued revised prudential regulations for consumer financing, mainly personal loans and auto loans. As per the press release, the revised regulations ... will help to moderate demand growth in the economy, leading to slower import growth and thus supporting the balance-of-payments..

I called this mission creep.

SBP’s mission creep and politically motivated loosening of monetary and credit policies have been a matter of interest for me for a while now.

Mission Creep

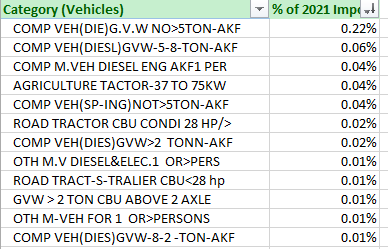

The purpose of Prudential Regulations is to restrain commercial banks from over exposing themselves to leverage and endangering the entire financial sector to systemic risk. The share of car financing is 2% in the scheduled banks’ credit portfolio. It presents no systemic risk such that a revision in Prudential Regulations is required.

I went on to say that such micromanaging of the banks isn’t healthy, neither for SBP nor for the banking sector as a whole.

Nurturing man-child banks

Prudential Regulations should give broad rules, but SBP gets a high from breathing down the neck of commercial banks. Commercial banks have risk officers, risk committees, risk policies and I presume internal risk rating metrics. For loans that comprise measly 2% of their credit portfolio, with the qualified human resources and IT systems they have acquired, the commercial banks should be able to put in place appropriate processes, controls and risk assessment criteria. It appears SBP doesn’t trust the bank’s management and systems to be capable of managing a car financing portfolio. SBP is advising the bank the maximum tenure of such loans, the maximum financing exposure to a single borrower for such loans and the minimum down payment required.

The problem with the SBP guidelines is that they are unduly restrictive, unduly detailed, and unduly prescriptive.

In that post, I wrote SBP policies are incoherent. On the one hand, SBP is discouraging car imports through these prudential regulations. While on the other hand, SBP and commercial banks continue to market Roshan Apni Car which encourages car purchases (only a portion of which is paid through remittances).

Now go back up and read what was reported a day earlier about Shaukat Tarin and the government’s plan for car financing on September 22, 2021. Maza na aaye to paisay waapis.

April 7, 2022

On April 7, 2022, in tandem with issuing the Monetary Policy Statement, SBP issued another circular imposing a 100% cash margin on 177 import items in a bid to curb their imports. Early discussions were that it restricted car imports, but that wasn’t the case as I covered in Monetary Policy 7 : SBP's misguided import compression?

The country is importing too many luxury cars when it can’t afford to. If SBP is imposing a cash margin to deter imports of luxury cars, then it is a very good thing. Wait...What? The cash margin is not on luxury cars but on import of commercial vehicles such as trucks and tractors which are required for becoming part of value chain, connecting markets and increasing commerce. Oh, well.

Mid-April 2022

I had thought that September 2022 Prudential Regulations would have killed the car financing market. I admitted in my Monetary Policy #8: Curious case of imported cars that I was wrong about that.

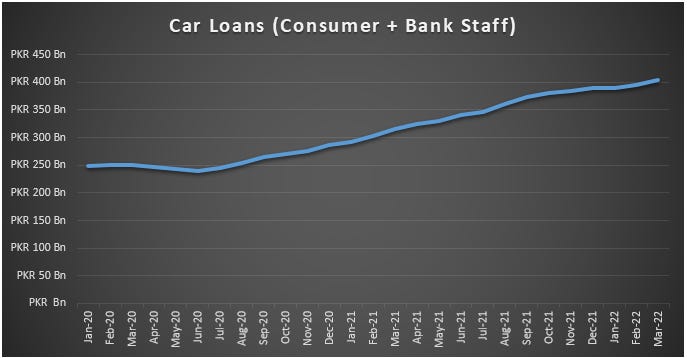

The below is from SBP’s latest CREDIT LOANS CLASSIFIED BY BORROWERS. If you squint, you can see that after September 2021 the trend of ever-increasing car loans appears to be slowing down rather stops increasing. Thus, the SBP regulations did achieve their objective. But then it appears to pick up again in January 2022.

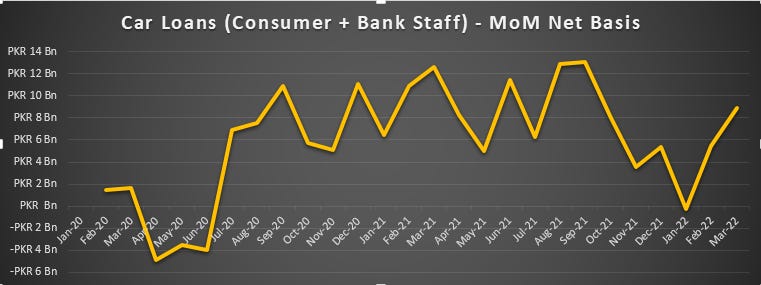

Let’s look at car loans on M-o-M net-basis. After the revised SBP prudential regulations, there was significant decrease in the rate of new car loans falling down to around zero by Jan 2022. However, since then, the car loans are back, and back with a vengeance. It’s as if, all of a sudden, the new prudential regulations had no impact at all.

What’s going on? Cars aren’t cheap. And the new regulations don’t make it easy for anyone to buy these cars.

I don’t know how true is the above theory, but I can tell you that in mid-2000s, a textile group had requested me for a financing facility that they will use to book cars for selling on “on”/”own”.

With volatile stock market and a falling rupee, the investment in cars appear as an inflation hedge. If rupee keeps falling, the dealers will increase the price every few months. This gives an investor an opportunity to book the car at pre-increase price and sell it at the post-increase price. In addition, such cars sell of “on”/”own” premium, thus providing a larger profit margin to the investor for a short term investment.

If new passenger vehicles are considered a store of value, an inflation hedge and/or an investment product, it is unlikely that any increase in regulatory duty or financing costs will deter their imports. The only option left to explore is an outright ban on import of cars, but that will have its own “distortionary” effects.

The fresh ban on the imports by the government is likely to take a heavy toll on the automotive industry as it would halt the import of completely built-up (CBU) cars which the dealers fear would strengthen the hegemony of local assemblers.

The CBUs are widely used across Pakistan especially in urban centers due to their cheap price with almost the same specifications compared to the products offered by the local assemblers.

According to auto-dealers, the restriction on the import of CBUs will affect the import of used vehicles and would result in the ‘hegemony’ of the local assemblers.

They said that the local assemblers routinely jack up the prices of vehicles arbitrarily, and now they have been given an open field by the government.

Most of the used vehicles are imported from different countries under the “gift scheme” that allows overseas Pakistanis to gift a car to their blood relative living in Pakistan or a public servant stationed abroad could also bring the vehicle-in-use upon his return to homeland.

Sources said multiple agents in Pakistan import these vehicles under the gift scheme using the documents of overseas Pakistanis. Sources added that the expats offering his or her documents for the import also receives a commission.

The auto dealers said the import of second-hand vehicles enables the citizens with low buying power to own a vehicle as they are cheaper compared to the ones assembled locally.

However, they said the import of such vehicles is halted now after the fresh ban on CBUs by the government.

The dealers feared that the measure would strengthen the hegemony of the local assemblers - who have already developed into cartels – and they would jack up the prices of their products fearing no competition.

All Pakistan Motor Dealers Association (APMDA) has appealed to the government to review its decision.

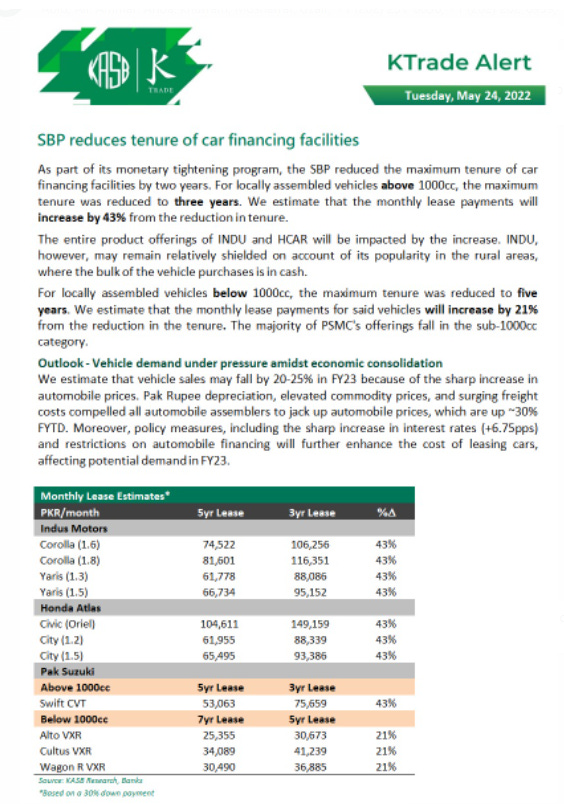

May 24, 2022

SBP issues a circular modifying the Prudential Regulations

Maximum Tenure: The maximum tenure of auto finance facility is reduced from five (5) years to three (3) years for vehicles above 1,000 cc engine displacement and from seven (7) years to five (5) years for vehicles up to 1,000 cc engine displacement.

You may have noted that changes in Prudential Regulations as per September 23, 2021, circular mentioned earlier above weren’t applicable to locally assembled cars up to 1,000cc or electric vehicles. SBP has now removed that exemption through the current circular and now those PRs are also applicable to 1000cc locally assembled cars and electric vehicles.

Moreover, other amendments issued earlier, vide BPRD Circular Letter No. 29 dated September 23, 2021, will henceforth be applicable on financing for all locally assembled / manufactured vehicles, including on financing for vehicles of up to 1,000 cc engine displacement and locally assembled / manufactured electric vehicles.

However, it still doesn’t apply to Roshan Apni Car.

However, the regulatory treatment of Roshan Apni Car product communicated earlier to RDA participant banks will continue to remain effective.

I covered it above that if we look at gross basis, the Sep 2021 circular had an impact as it tempered the rapid rise of car financing. Below is the updated chart till April 2022.

Looking at financing statistics on a net basis, we see that after a fall in the last quarter of CY2021, it started to rise again in January and February before a fall in April. My guess is that car financing was again increasing in May and that is why SBP felt the need to introduce the latest circular.

Will this latest Prudential Regulation be the straw that finally breaks the back of the car financing camel? It appears so, as you can even see the vomiting camel pattern.

The guess is further substantiated by the fact that the latest change increases the monthly installment by 43% which is a significant increase in monthly debt servicing cost. But I have been wrong before.

However, two things should be noted.

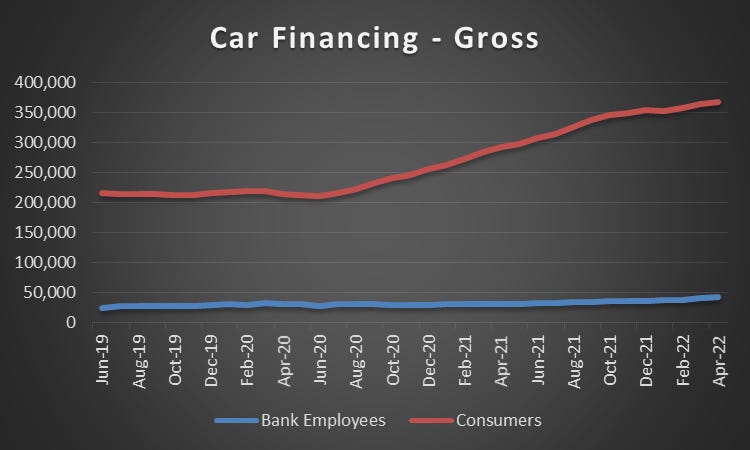

While car financing by consumers fell, car financing by bank employees is increasing. It could be that the bank employees have realized the potential of earning easy money on this facility (bank employees get easier terms than ordinary consumers) and are financing cars to sell them at a profit or on/own.

The new PRs aren’t applicable to Roshan Apni Car. While the assumption is that the Roshan Apni Car is akin to the export of cars, that assumption is only valid if someone is financing the car by placing a 100% lien on his remittances. Non-lien financing financing requires a down payment of 15%-45%. If overseas Pakistanis are financing their cars with a 15% down payment under Roshan Apni Car, then the assumption of exporting cars isn’t valid anymore. Moreover, for a savvy expat or a local investor, Roshan Apni Car provides a good arbitrage opportunity as it allows the expat to finance up to three cars at half the delivery time. He/she can then sell the car on on/own for a nice profit. This is not too farfetched. You can see from the news item about the “gift” scheme that enterprising used car dealers are experts at reaching out to “returning bureaucrats” and “returning expats” to make the most of the gift scheme.

Similar to how SBP provides a breakdown of cars financed by bank employees and consumers, it should also provide details of cars financed through Roshan Apni Car and whether it was a lien product or a non-lien one, and what was the down payment percentage. That would help us to know if Roshan Apni Car is being used to make arbitrage profits (I am using “arbitrage” very loosely here. Please don’t be pedantic about it not being arbitrage).

By the end of July (the circular is issued yesterday, it will take a month for it to have a noticeable impact and then a month for SBP to release the credit statistics), we will know if the camel really is vomiting.