I had a few minutes to spare and logged into the Twitter spaces session that PMLN was holding over the SBP Amendment Bill. I joined late and left early, not because the discussion wasn’t interesting, rather I was busy elsewhere, and a few minutes was all I could spare. Ahsan Iqbal was talking when I joined, and he made three comments that pricked my ears.

The first one was about the five-year tenure of the SBP governor. Ahsan Iqbal said something along the lines of what I said in my tweet yesterday, which made me wonder if Ahsan Iqbal reads my tweets.

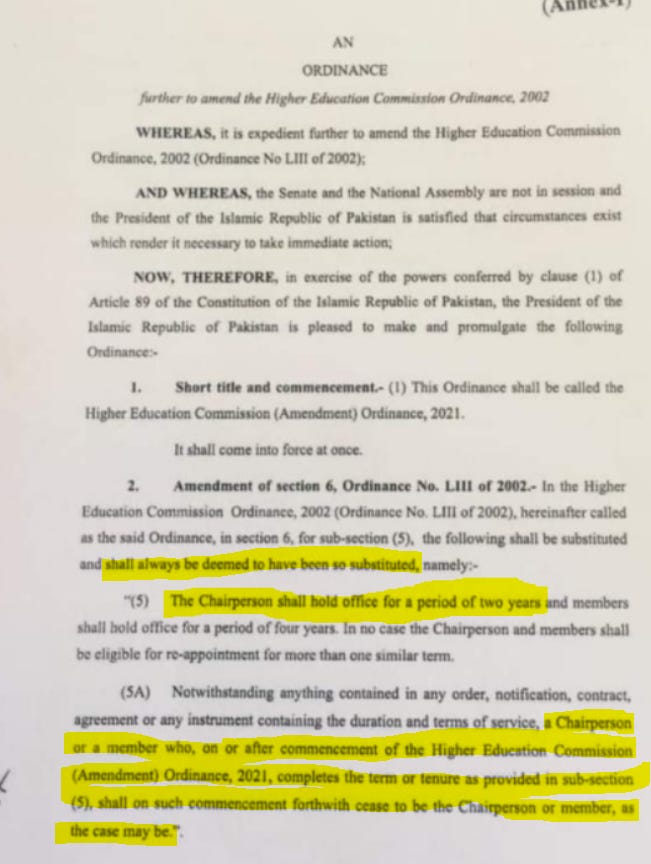

A few months ago, I wrote this about the SBP amendment.

Most of the editorials and op-eds are focused on the independence of the central bank and the "security of tenure" of the SBP governor. A noble cause indeed. However, if people think that this amendment can provide security to the SBP governor, they are sadly mistaken. Just this month, the ordinance factory i.e. the president, was pleased to promulgate the amendment to the HEC Ordinance where he, with retrospective effect, reduced the tenure of HEC Chairman from 4 years to 2 years. Government can take a similar step with SBP governor if it so pleases.

The ordinance reads that

…the President of the Islamic Republic of Pakistan is satisfied that circumstances exist which render it necessary to take immediate effect…

The president could have asked that aisi bhi kia aafat aa gayi ha ke HEC Ordinance change karna parh gaya HEC Chairman ko hataanay k liay with retrospective effect. No wonder he is known as Ordinance Factory for rubber-stamping every ordinance that comes his way.

Subsequently, a notification was issued, the Chairman was removed, the matter went to court, and yesterday, the court restored the previous Chairman to his position stating the notifications for his removal were issued without lawful authority.

The reason for my tweet at the top of this post is the answer that Shaukat Tareen gave to Babar Nizami justifying the five-year tenure of SBP Governor.:

Speaking about extending the SBP governor’s tenure from three to five years, one of the topics that has been continuously disagreed on between the federal government and the opposition, Tarin said that it was a non-issue and rather a simple logical step to make the SPB’s functioning more effective.

“Three years are not enough for successful execution of strategies devised by the head of an organisation. Jobs of this nature, of senior posts in any important organisation, require at least five years to make fruitful changes,” he said.

On the one hand, SBP Governor needs five years to make fruitful changes in an institution that is considered one of the best run in the country i.e. SBP, while on the other hand, the tenure of HEC Chairman, who will lead the organization which requires major revamp, was reduced to two years.

Kia ye Khula tazaad nahin

The court decision made me question if the door to removing the SBP Governor through an ordinance is now closed. I will let the legal experts comment on that.

Lest I am misunderstood, I am with Shaukat Tareen on this one i.e., three years is too short a time. But considering that SBP is already a well-oiled machine, I can live with SBP Governor tenure being three years than HEC Chaiman’s for the same period. Not that anyone cares what I think.

The second comment Ahsan Iqbal made was when he said IMF and SBP sat on the Amendment for 10 months and then got it approved by the standing committee in less than two hours. The “10 months” made me think that he also read my last substack as I made that point three times in that post, once in the subtitle and twice in the post as

It is a shame that in a period of 10 months, the top technocratic minds of SBP, MoF and IMF can't get the first paragraph of the SBP Amendment Bill right.

It’s a shame that in the 10 months (that we know of as the first draft was leaked in March 2021 over WhatsApp) that the draft was being discussed amongst the top technocrats of IMF, SBP, and Ministry of Finance, no one questioned the primary objective description. Apparently, they just copied and pasted it from an IMF manual.

Can you believe that the top technocratic minds at SBP, MoF and IMF came up with these objectives and didn’t feel a need to clarify them in the 10 months that we know they were discussing it amongst themselves? Quite a display of incompetence if you ask me. Should be embarrassing for those that came up with it

I know. I have a tendency to get carried away.

Reportedly, the bill was approved by National Assembly in 48 minutes by suspending the assembly rules. This is a piece of legislation that will be in place for at least half a decade, and the people’s representatives didn’t get to discuss it.

The government approved the SBP amendment Bill in haste in just 48 minutes by suspending the assembly rules.

The finance minister had moved the bill at 10.06pm and the NA speaker announced its approval at 10.54pm.

The PML-N and PPP first pleaded the National Assembly speaker to let the debate take place and then in sheer frustration gathered in front of his desk to stop him from bulldozing the parliament’s proceedings.

However, nothing could stop the PTI-led government from handing over absolute autonomy to the central bank, which PPP’s Syed Naveed Qamar said would “compromise national security”.

“I beg you… please do not suspend the rules and allow the house to debate on the most important bill in the country’s history for at least two days”, said PML-N’s Ahsan Iqbal.

Aren’t you amused that SBP Governor requires 5 years to bring about fruitful changes in the banking system yet the Act that authorizes him to bring about those changes can’t be discussed on the floor of the National Assembly for even an hour?

The final comment Ahsan Iqbal made was with respect to SBP not being a lender of last resort for the government. I wish we had a transcript, so I am not putting words in his mouth, but he said something along the lines of

If the government cannot borrow from SBP as a last resort, then the government will be forced to borrow from the commercial banks and the latter will make a cartel and charge an arm and a leg (ok, he didn’t use “an arm and a leg” but I think that is what he implied). However, if a commercial bank is going kaput, the SBP will lend to it. How can this be fair that the government of the country cannot be lent to but a private bank owned by private shareholders can be (he didn’t use the “private bank owned by private shareholders” but I think this is what he was driving at).

I am going out on a limb here, but I believe lender of the last resort is a specific term that is used for central bank’s lending to commercial banks. The purpose of the lender of last resort is to prevent a liquidity crisis at one commercial bank from becoming a solvency crisis of that bank, thereby threatening the stability of the financial system by causing bank runs spreading the liquidity crunch across the whole system, and threatening the financial stability. Fair warning: the aforementioned definition of lender of last resort is what I have learned over the years, and you may not find it in so many words in economic textbooks.

Reading legal documents for most of us is tedious and boring but a necessary and thankless part of the job, unless you are a lawyer or tax accountant then not only do you find it as the most riveting piece of non-fiction but also get paid to read it and suggest more unnecessary verbiage. One has to keep track of all the keywords used in the document to ensure that they are defined correctly to mean what we think they mean. I had highlighted in my earlier posts that “quasi-fiscal operations” or “medium-term” or “guided by” have not been defined anywhere in the amendment, leaving us and the interpreters guessing what does that mean and how does it affect the legality of various operations of SBP. “Development Finance” is defined in the amendment, which prohibits all the activities that SBP is celebrating through its Twitter account.

Such points haven’t been raised in various op-eds as unlike a new piece of legislation, which is usually self-contained when it comes to amendments, it has such language as “insert clause 4C after the clause 4B in the original Act” or “delete clause 20(C)” or “substitute clause 56 with the following:..” that requires the reader to have the two documents open on his or her computer and to read them side by side to see what is changing. Reading one document is mind-numbing, comparing two such documents side by side is akin to sending any sane person barring lawyers and tax accountants into an induced coma.

The reason for all this digression was to show that when one only reads the Amended document, one may not truly realize what is going on. Let’s go through the clause as per the original Act and the Amended bill.

SBP Act 1956

17G. Lender of last resort. –

Where the circumstances so warrant and a scheduled bank approaches the Bank for financial facility to improve its liquidity and where the bank in the opinion of the Bank, is solvent and can provide adequate collateral to support the financial facility, the Bank may provide the financial facility, in accordance with the regulations made by the Bank in relation thereto.

SBP Amendment Bill 2021

- In the said Act, for section 17G, the following shall be substituted, namely: —

"17G. Lender of last resort.-

(1) Where the circumstances so warrant and a scheduled bank approaches the Bank for a financial facility to improve its liquidity and where the scheduled bank in the opinion of the Bank is solvent and can provide adequate collateral to support the financial facility, the Bank may provide short-term financial facility in accordance with the regulations made by the Bank in relation thereto, notwithstanding the provisions of sub-sections (2), (3) and (3A) of section 20.

(2) Where in the opinion of the Bank, the aforesaid financial facility to a scheduled bank is necessary to preserve the stability of the financial system and where the bank does not fulfill the requirements specified under sub-section (1) of this section, the Bank may, provided that it determined the scheduled bank is viable in the medium term, provide such financial facility on such terms and conditions as the Bank specifies, provided that a written irrevocable guarantee of the Federal Government is received in favour of the Bank, securing the repayment of the facility, notwithstanding the provisions of sub-section (2), (3) and (3A) of section 20.

(3) For the purposes of this section, a financial facility shall not include participation in the capital of a scheduled bank: “Provided that any outstanding holding by the Bank of equity or right to equity in any scheduled bank shall be liquidated within ten years from the commencement of the State Bank of Pakistan (Amendment) Act, 2021.

If you have followed my writings, I have said earlier that “what Section 17 giveth, Section 20 taketh away” implying that Section 17 mentions the activities that SBP is allowed to engage in, and Section 20 mentions the actions that SBP is prohibited from. The above clause is 17G which means it is part of Section 17 and is an activity that SBP is allowed to do.

The first thing to notice in the current Act is that the lender of last resort facility is only available to the scheduled banks. SBP was never acting as a lender of last resort to the federal government, over which Ahsan Iqbal is making a fuss as if the Amendment is taking away this privilege of the government.

Now that we have peeked into the rabbit hole, might as well jump in and go over the whole amendment clause.

The original Act states that SBP can act as a lender of last resort by lending to a scheduled bank for liquidity against a collateral security if SBP deems the bank to be solvent. The entire clause is a single paragraph.

In contrast, the Amendment has three subsections (1), (2) and (3). Subsection (1) is similar to the original Act, with the addition that the facility offered to a scheduled bank for liquidity can only be short term in nature. I don’t think “short term” is defined in the Act or Amendment, but I can be wrong.

Subsection (2) states that if the scheduled bank is insolvent (the word “insolvent” doesn’t appear anywhere, but this is what the language is implying— that’s legalese for you) and thus cannot borrow under Section (1) above, then SBP can still act as a lender of last resort if SBP thinks that the bank will be solvent in a medium-term, the lending is necessary for the financial stability and the Federal Government provides a guarantee that the scheduled bank will repay the facility.

Three comments on this:

a. How long is the “medium term”, a period in which the scheduled bank has to become viable?

b. The tenor of the financial facility isn’t mentioned but should be assumed to be medium-term. An insolvent bank cannot be expected to repay the facility before it is viable.

c. Why should the Federal Government provide a guarantee? SBP is the regulator that has been responsible for auditing, assessing and, regulating the bank and the financial system. If the scheduled bank is going belly up under SBP’s watch, SBP should be responsible for assessing the repayment capacity and viability of the scheduled bank and lend accordingly against good collateral. Why should the Federal Government backstop SBP here?

The last sentence of both subsection (1) and subsection (2) of the amendment states “notwithstanding the provisions of subsections (2), (3) and (3A) of section 20.” For this, we will have to read the original Act, as these subsections do not exist in the Amendment. That is what I was referring to when I said that when dealing with amendments, you have to keep the original Act open as a number of clauses will refer to the original Act.

The provisions are part of Section 20 and you know by now that Section 20 lists the prohibited activities. From the original Act:

2) purchase its own shares or the share of any other bank or of any company, or grant advances or loans upon the security of any such shares;

(3) advance money on the mortgage, or otherwise on the security, of immovable property or documents of title relating thereto, except where such advance is made to any of its officers or servants for building a house for his personal use against the security of the said house;

(3A) become the owner of any immovable property except where ownership is necessary for the use of such property by the Bank, or for the purposes of use for Shariah compliant instruments, for the residence, recreation or welfare of its officers or servants];

(cont’d) This means the security offered by scheduled bank as collateral to the lender of last resort cannot be shares or mortgage over immovable assets or even ownership of the land.

Finally, Subsection (3) reads that SBP cannot acquire a shareholding in a scheduled bank. The lender of last resort facility is to provide liquidity to a scheduled bank when other banks aren’t extending liquidity to it. When SBP acquires shareholding in that bank, the other banks automatically get confidence in the subject bank’s viability and start extending liquidity to it. This subsection prohibits such acts by SBP.

It further adds that if SBP currently holds shareholding in any scheduled bank, SBP has to get rid of it within 10 years of the amendment coming into effect.

Now if you read the whole amendment in plain English, it is saying

SBP can act as a lender of last resort to a scheduled bank for a short term if it is solvent and for a medium-term if it is insolvent but can become solvent in a medium-term provided it is necessary for the financial stability of the system and the federal government provides a guarantee for its repayment. The security offered by the scheduled bank in both cases cannot be shares, a mortgage over immovable property, or ownership of immovable property. In no event, SBP will take shareholding in the scheduled bank under this clause and any shareholding that SBP has right now in any bank will have to be liquidated within 10 years of passage of this bill.

The questions to ask are: 1. what is short term? 2. What is medium term? 3. Why should the federal government backstop an independent SBP that can’t do its job properly?

Fascinating stuff if you can get it but can be brain-damaging if you are not into it.

I am appreciative that there is someone like Ahsan Iqbal who cares enough to read about the Amendment and actually wanted to discuss it in the assembly clause by clause. I was half-joking when I said he reads my tweets and substack. Most of us were focused on the clauses that are close to us, i.e. I focused on the Objective section, quasi-fiscal activities, and development finance activities. I didn’t read the 17G clause till today, as I didn’t care much about it. Others focused on the independence of SBP or the relationship between the finance minister and the SBP governor. Ahsan Iqbal’s dissent note shows that he read it cover to cover. One is bound to get stuff wrong, especially if it’s drafted in legalese. That is why we have debates and discussions to correct misunderstandings and rectify contradictory clauses. But as I said earlier

It’s a shame that best technocrats at SBP, MoF and, IMF sat on it for 10 months and now want to bulldoze it through parliament in a few hours.

There is a clause 9C in the SBP Amendment Bill that prohibits SBP from lending to Government and Ahsan Iqbal may have been referring to it but that’s not about SBP acting as a lender of last resort unless my understanding of lender of last resort is wrong. I may take up that clause later if it strikes my fancy.

Despite appearance to the contrary, I have respect for Ahsan Iqbal for raising these issues as rarely anyone else did. All I want is that the Amendment is discussed/debated and if, after the discussions/debates, it is felt that this Amendment, as is, is in the best interest of the country, then this is what the country gets.

I do hope that this brings home the point that it is criminal that an Amendment that has such far-reaching consequences is rushed through the parliament leaving many questions in its wake.

Disclaimer: I was tuned in for quarter of hour. It may be that these issues were barely touched upon while I was tuned in and dealt with comprehensively after I signed off.