This post is based on certain assumptions. If those assumptions aren’t valid, then the conclusion isn’t valid either.

“Ye to banks nay blackmail Kia hay [government ko]. Riasat kyun khamosh baithi hai”

— Kamran Khan

“Hum chahtay to open market operations cancel kar daytay. Jab MoF paisay nahin uthata to SBP OMO mein utha layta hai. OMO nahin hoga to paisay banks k pass interest free parhay rahain gay. Banks ka koonda ho jayega”

— Shaukat Tarin

The above quotes are from the below interview of Shaukat Tarin conducted by Kamran Khan yesterday.

I was having a Twitter discussion over this interview. Rasheed wondered what if MoF calls the banks’ bluff and cancels the open market operations (OMO) as suggested by Shaukat Tarin.

In my opinion, the banks can sit on idle cash for some time and this will not be the end of the world for them. Banks are earning record profits. In three quarters of 2021, UBL has made a profit of Rs.22 billion (37% higher than the same period last year).

This is more than the Rs.20 billion profit made by UBL in the full year 2020. Sitting on idle cash will be akin to, as the memon saying goes, “Nafay mein nuqsaan ho jana” for UBL.

I replied to Rasheed that Meezan Bank also sits on idle cash as I covered in my earlier post quoted below

I am using HBL, UBL, Bank Al Habib (BAH) and Habib Metro (HMB) for comparison, i.e. two large banks and two medium-sized banks.

The vertical analysis in the lower table shows that while the conventional banks have 50-60% of their total assets in Investments (primarily government securities), Meezan Bank has only 28% of its assets in Investments as it can’t find sufficient sharia-compliant government securities to invest in.

When we look at the next line i.e. Advances, conventional banks have around 30%+ of their total assets in Advances i.e private sector credit. For conventional banks, we can hypothesize that 60% of government borrowing is crowding out the private sector. But the hypothesis fails when we look at Meezan Bank's balance sheet. Meezan Bank also has 30%+ of its assets in private sector Advances when clearly no crowding out is taking place at Meezan Bank.

If we look at the first three line items, which I have summed up as Subtotal Liquid Assets as the returns on these assets is de minimis compared to Advances and Investments, we see that conventional banks have around 10% of their assets in cash, and Meezan Bank has 30% of its assets in cash. Despite the fact that government borrowing isn't sucking up liquidity at Meezan Bank, Meezan Bank would rather prefer to keep the money idle in liquid assets rather than lend it to the private sector. The quantum of funds in liquid assets at Meezan Bank is half a trillion rupees, almost equivalent to the balance held by HBL which is almost three times the size of Meezan Bank in asset size.

(I have bolded the phrase in the above paragraph, where I was completely wrong in my post). To which Rasheed replied

This forced me to look at the financial statement of Meezan Bank with a fresh eyes.

This time I have highlighted the row which shows lending to other financial institutions. (Click on the image to enlarge)

Whereas the conventional banks lending to other banks is close to zero, the figure for Meezan Bank stands at 23%. I should have looked deeper into this the first time, but I didn’t because it was confirming the hypothesis that I was trying to prove in that post.

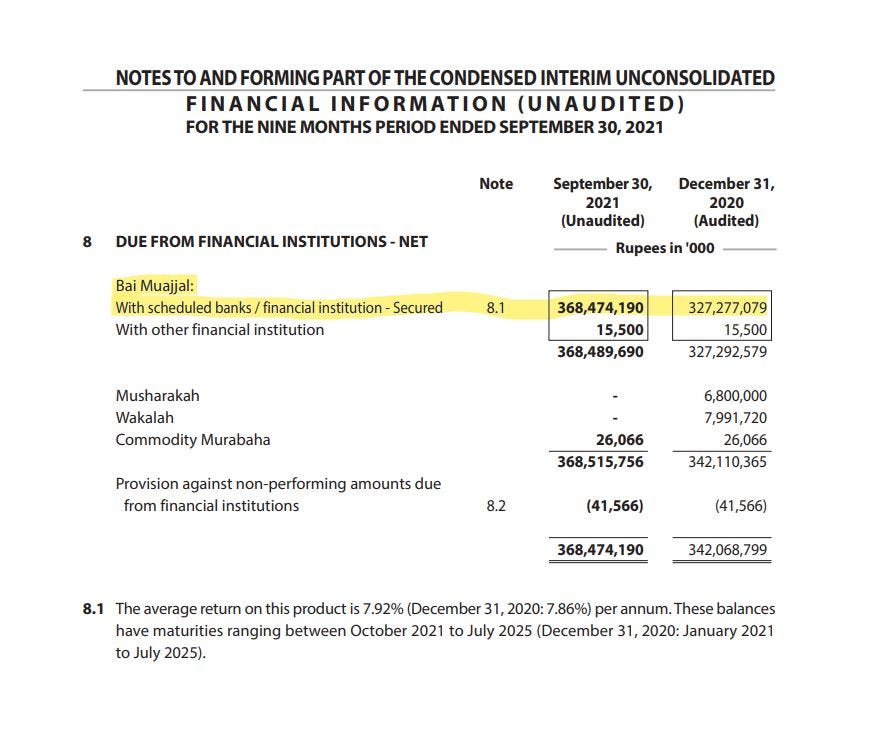

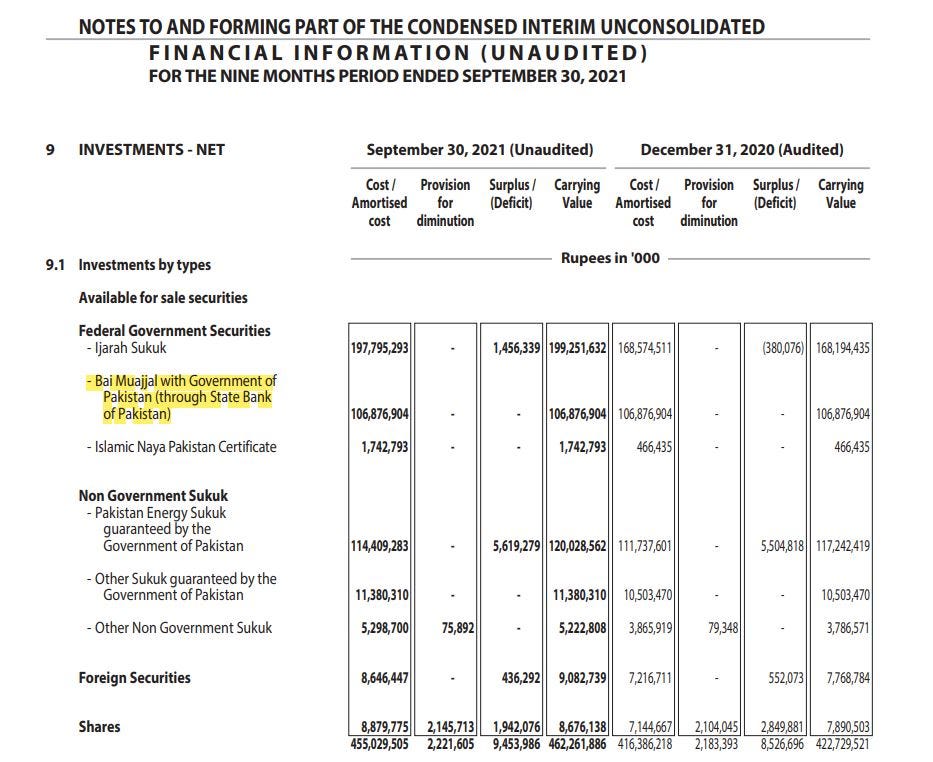

Looking at the notes of Meezan’s 2020 Financial Statements, we see that it is a repo transaction, which Meezan calls Bai Muajjal i.e., Meezan is lending to commercial banks against a collateral of federal government securities.

The repo continues to increase in 2021 rising to Rs.368M at the end 3Q 2021.

I am assuming Meezan Bank is carrying out repo transactions with conventional banks due to the size of the loan. Conventional banks are using the funds raised from Meezan Bank to invest in federal government securities, earning a spread between the rate paid to Meezan Bank and the rate earned on the newly issued federal government securities. Nice little income stream for conventional banks.

Meezan Bank is disadvantaged compared to conventional banks:

The rate of profit on sharia compliant federal government securities in which Meezan Bank is allowed to invest in is lower than the rate of interest on conventional federal government securities.

There aren’t enough sharia compliant securities so

Meezan Bank provides “sharia compliant” bai muajjal funding to conventional banks, against a collateral of government securities.

The conventional banks use the funds borrowed relatively cheaply from Meezan Bank to further invest in relatively higher return paying conventional GoP securities.

The Rs.368 billion of repo lending outstanding at the end of Q3 2021 in Meezan Bank’s books is more than three times the amount that Meezan Bank has directly invested in Bai Muajjal GoP securities. No wonder Irfan Siddiqui is upset.

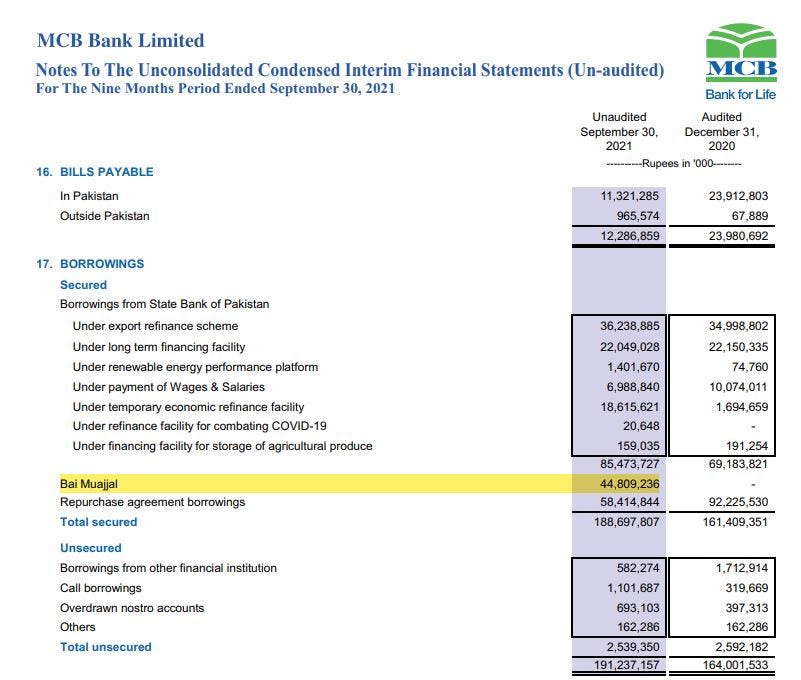

It would be interesting to know which banks are milking this situation to make the maximum amount from GoP securities, i.e. borrowing from Meezan Bank relatively cheaply and then investing the proceeds into GoP securities. Unfortunately, the secured borrowing section of the major banks does not show borrowing against Bai Muajjal except for MCB and Bank Al Falah (both conventional banks) in 3Q 2021. The amount appearing in their financial statements isn’t big enough to correspond with the amount appearing in Meezan Bank’s financials.

MCB has Rs.45M borrowed against Bai Muajjal.

Bank Al Falah has Rs.45 million outstanding against Bai Muajjal at the end of 3Q 2021.

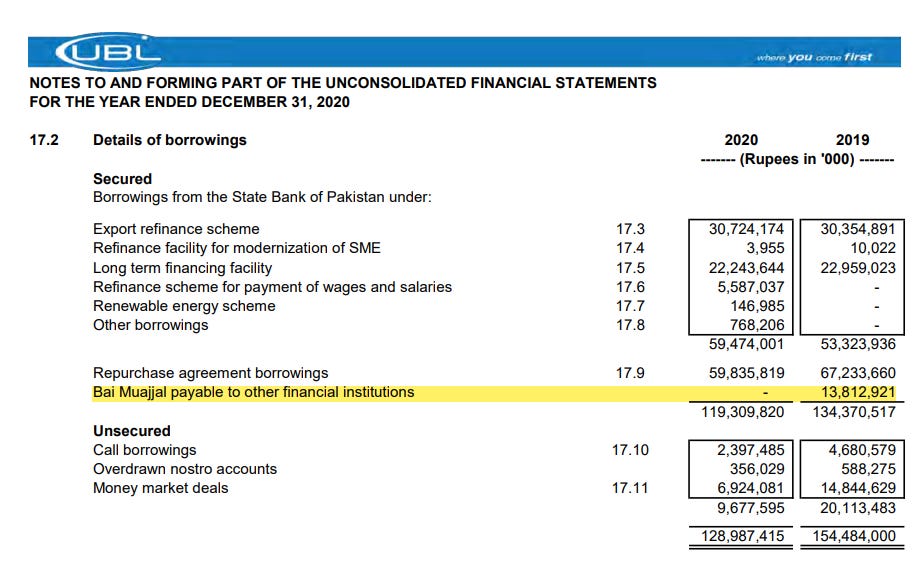

UBL had the figure in 2019 financials, but it isn’t appearing in any of the financials since

Going through 3Q financials of other banks, I confirmed that borrowings against Bai Muajjal is not present in the 3Q 2021 financial statements of UBL, HBL, ABL, Habib Metropolitan Bank, Faysal Bank, Bank Al Habib, Standard Chartered Bank or Bank Islami. Assuming the Bai Muajjal borrowing appearing in MCB and Bank Al Falah financial statements are borrowings only from Meezan Bank,

we still can’t account for more than Rs.300 million of Meezan bank’s repo lending to other financial statements from the financial statements of the major banks.

As the borrowing from Meezan Bank is similar to a repo transaction, I am assuming, the banks aren’t reporting it separately, and it is reported as a repo borrowing.

If that is the case,

We know that conventional bank use the money borrowed under repo to invest in conventional GoP securities. Meezan is squaring the circle by lending to conventional banks using a sharia compliant structure of Bai Muajjal. This allows Meezan Bank to pretend that it doesn’t know what the funds are being used for.