Monetary Policy #9: Policy rate and bank debt statistics

Real world is not an Econ101 textbook. Human beings, including central bank governors, are not infallible.

Quite a few tweeps jumped on my yesterday’s post, inquiring if the increase in car financing made me realize the error of my ways. They were really upset with the above meme. The answer is No. The meme holds and I am starting the post with it to rub it in their faces.

The economic theory says that increasing the interest rate reduces demand-pull inflation. The underlying assumption is that the demand-pull inflation is bank-debt financed i.e., a large segment of the population borrows from the banks and when the rates rise, the debt-servicing capacity of the population decreases and they either start paying down their debt or at least, don’t borrow anymore thus leading to drop in consumption.

In developed countries, one of the biggest channels for the transmission of interest rates is mortgages. In contrast, the mortgage depth in Pakistan is less than 1% which is among the lowest in the region and the world. Moreover, the mortgages that are being offered under SBP’s Mera Pakistan Mera Ghar (MPMG) scheme are fixed-rate mortgages i.e., even if the interest rates rise, the mortgage rate will not increase for the next ten years under the scheme. Thus, not only the mortgage channel for transmission of change in interest rate is very small, it has been made ineffective by fixing the rate. In Pakistan, we can completely discount this channel, which in the rest of the world is the most effective channel of interest rate transmission.

Now that we have established that the linkages between the financial sector and the real sector in Pakistan aren’t like the rest of the world or as taught in Econ 101, let’s look at the commercial banks’ credit to the non-consumers.

The chart looks a bit crowded, for which I apologize. While commercial banks increased credit to the private sector in the last 3 years, they overdosed on investment in government securities during this period. The dashed line shows that while private sector borrowing as a percentage of the total was 46% at the beginning of the period, it reduced to 35% as of March 2022. Thus, private sector loans have come down from around half of the bank’s portfolio to a third of the bank’s portfolio. Or to put it in another way, banks’ investment in government securities is almost double the banks’ loans to the private sector. This information appears worse if looked at in a table format.

Just the increase in commercial banks’ investment in government securities i.e., Rs.7.3 trillion, during this period is almost equal to the entire private sector loan outstanding i.e., Rs.7.8 trillion. This is despite the fact that SBP provided a stimulus of Rs. 2 trillion to the commercial banking sector for extending credit to the private sector.

We can establish two points:

Despite a very large stimulus including a reduction in the policy rate by 625bps, the increase in private-sector credit isn’t large compared to the increase in government borrowing. If Milton Friedman was right (I have my doubts) in saying that inflation is a monetary phenomenon, we can be sure that the increase in the private sector credit isn’t the main reason for inflation in Pakistan.

Thus we can safely conclude that if inflation in Pakistan is money-supply induced inflation, then government borrowing is the main culprit.

We know that under the present circumstances, the government sector has no capacity to reduce its borrowing, unlike the private sector. Any increase in interest rate will increase the financing cost of the government borrowing, resulting in the government printing more money to service this cost, thus further increasing the government borrowing. When the rate was increased to 9.75%, it was estimated that the financing cost of the government can increase by Rs.500 billion (yes, yes, I know, a part of it will come back to the government as tax revenue and the net impact may be less than Rs.500 billion). Now SBP has increased the rate by additional 250bps, and the federal government debt has also increased since the last estimate. It would be safe to estimate that the cumulative increase in the policy rate of 5.25% since September 2021 can increase the financing cost by Rs.1 trillion.

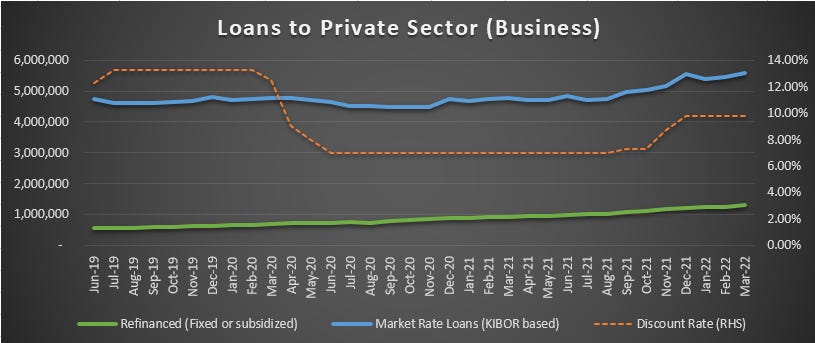

The below chart breaks out the loans to the private sector between market-rate loans and subsidized/fixed-rate loans (ERF/LTFF/TERF).

The refinance loans continued increasing gradually irrespective of the discount rate as they should. The market rate loans didn’t really increase when the discount rate decreased by 625 bps. They started increasing around the time when SBP started increasing rates in September 2021 and as SBP further increased the rates, the loans to the private sector continued increasing. Thus, an increase of 2.75% in the policy rate has had no impact on private sector borrowing.

The below table shows the same data on a net basis Y-o-Y and M-o-M. The major increase is in working capital loans. Next is LTFF/TERF which is immune to interest rate increases. Next, we have 1) ERF, which is again immune to interest rate increases, 2) Term Finance, which are term loans and are usually repaid on maturity, and 3) construction financing which SBP is itself forcing the banks to push by giving them monthly and quarterly target of disbursement.

Thus, working capital is the only sector where SBP’s increase in interest rate can have any impact. I break down the working capital borrowing by industry type and look at the net increase month over month for different industries. The list isn’t comprehensive. I have selected only those industries where the change was significant.

The largest increase in working capital is from sugar, and it appears to be seasonal as six months earlier, the sugar industry was paying down its debt. The other big items are the manufacture of chemicals, fertilizers, and power generation. These aren’t the industries that you want to reduce the activity of or increase their cost of financing. If they reduce their borrowing, it will exacerbate the food supply or lead to power shutdowns. If they pass on their interest cost to end-users, it will lead to further inflation.

The only line item that hints towards consumer items is the second last one, i.e., Whole and retail trade. If that sector/industry is contributing to inflation, wouldn’t it be better for SBP to target the specific industry directly through a circular asking for higher collateral or imposing higher risk weights rather than increasing the policy rate which will affect the entire economy? Frankly, it doesn’t matter because when SBP takes a targeted approach, it is as hamhanded as using a blunt tool e.g., when SBP targeted cash margin on imported items, it left me scratching my head as to how can SBP claim that items on the list are luxury items when they were mainly food, medicine, and intermediate goods.

It should be noted that March is quarter-end and usually, banks force their customers to borrow a maximum amount under their working capital lines even if it’s only for one night i.e., March 30th so that banks’ quarter-end results appear great. The aforementioned increase in working capital may be overstated for window-dressing purposes.

One element that gets missed in this entire discussion is inflation and devaluation. The same item that used to cost Rs.100 last year may now cost Rs.120. From SBP statistics it may appear that the commercial activity has increased, but it could be that banks are financing the same quantity of goods but as they cost more now, a higher loan amount is needed to process the same volume.

SBP also increased the interest rate on the export refinance facility (ERF) by 250bps. The textile sector is the main borrower of ERF, followed by rice and sugar. But why would SBP increase the rate of export refinance? Isn’t the purpose of export refinance to increase exports and reduce our current account deficit? When the current account is under immense pressure, it doesn’t make sense for SBP to increase the cost of exports. Unless SBP thinks that exporters are borrowing against export refinance, not to finance their exports but to invest in real estate and/or cars. If that is the case, SBP should just eliminate the export finance facility.

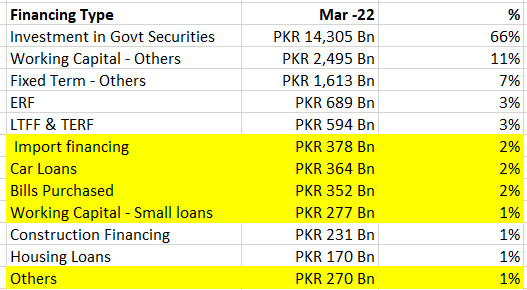

The below table summarizes the commercial banks’ credit to various sectors as of March 30, 2022.

To summarize,

Lending to the government comprises the highest proportion (66%) and it is only going to increase going forward. The increase in interest rates to date will lead to increasing the financing cost by Rs.1 trillion which will add to government debt. If SBP continues increasing the interest rate, there is a possibility that the increase in government debt reaches escape velocity.

An increase in interest rate can lead to a decrease in working capital loans, but these are industries such as food, chemical, fertilizer, and power generation where a decrease in activity may exacerbate inflation. Moreover, not all increase in the working capital loans is due to increased commercial activity. It can be due to an increase in the costs of underlying goods on account of inflation and devaluation.

Fixed-term loans and LTFF/TERF loans may not be affected by an increase in the policy rate, at least in the short term.

The rate on ERF has increased, but it is still a subsidized loan and only comprises 3% of overall borrowing.

Construction financing is a small proportion (1%) but SBP only has itself to blame if construction financing is causing inflation. SBP gave the banks mandatory targets for construction financing and banks are only following SBP’s guidance here.

Housing finance is subsidized fixed-rate loans and is a small proportion of overall financing.

This leaves us with loans highlighted in yellow, which comprise 8% of total borrowing. The total outstanding of these financings is Rs.1.6 trillion as of March 2022. An increase in interest rate may decrease their share from 8% of total borrowings, but it will not bring these down to zero. Thus, if SBP increases the policy rate to say 15%, this is where we expect it to have the largest impact. I think any reduction in the outstanding here will be negated by an increase in the financing cost of the government borrowing.

There you have it. The SBP data shows that any increase in interest will not have as large an impact on borrowing as Econ101 makes you believe. The reason

mortgage finance channel which transmits the change in the developed economies doesn’t work in Pakistan due to the small size of the sector and fixed-rate loans,

the size of government borrowing is large and an increase in interest rate will lead to higher financing costs thus forcing the government to print more money to service its debt and further adding to inflation,

reduction in working capital loans unless due to seasonality would further exacerbate inflation, and

reduction in the financings to the sectors highlighted in yellow such as car loans and import financing may not be enough to offset the increase in the financing cost of government borrowing.

No, I am not against increasing the policy rate. A higher interest rate may prevent the outflow of money, or reduce cash in circulation by encouraging people to deposit cash into high-yielding bank accounts/saving instruments, and May even attract hot money thus stabilizing the rupee against the dollar. However, based on the data presented above, I fail to see how a higher policy rate will alleviate cost-push inflation in a country where consumer financing is around 2% of the overall borrowing, the possibility of reduction in private sector borrowing is limited and government debt is at 66% of total borrowing and rapidly rising.

So for my trolls, one more time.

Also, Reza Baqir is a human and not infallible. You don’t have to fall over each other praising his every move. Just last week I covered how misguided was his LC cash margin requirement, which came on the back of an equally absurd earlier LC cash margin requirement.