The auction that all of us have been waiting for

The Jan 12 T-Bill auction will let us know if the unorthodox monetary policy actions of SBP will bear fruit.

Ok. It was only me who was waiting for the January 12 auction.

Forward guidance is just guidance, and this (OMO injection), on the other hand, is a concrete step

— Fahad Rauf, Ismail Iqbal Securities

This isn’t really the SBP striking back, instead it’s the SBP falling to the whims of the market. Essentially the equivalent of saying “please take our money and lend it back to us, but hey, hold back on the yields, will you?”

— Ariba Shahid, The Profit

SBP’s monetary policy actions are more thrilling than Netflix’s Money Heist

— aap ka bhai (kehnay main kia jaata hai)

“Ye to banks nay blackmail Kia hay [government ko]. Riasat kyun khamosh baithi hai”

— Kamran Khan

“Hum chahtay to open market operations cancel kar daytay. Jab MoF [T-bill auction mein] paisay nahin uthata to SBP OMO mein utha layta hai. OMO nahin hoga to paisay banks k pass interest free parhay rahain gay. Banks ka koonda ho jayega”

— Shaukat Tarin

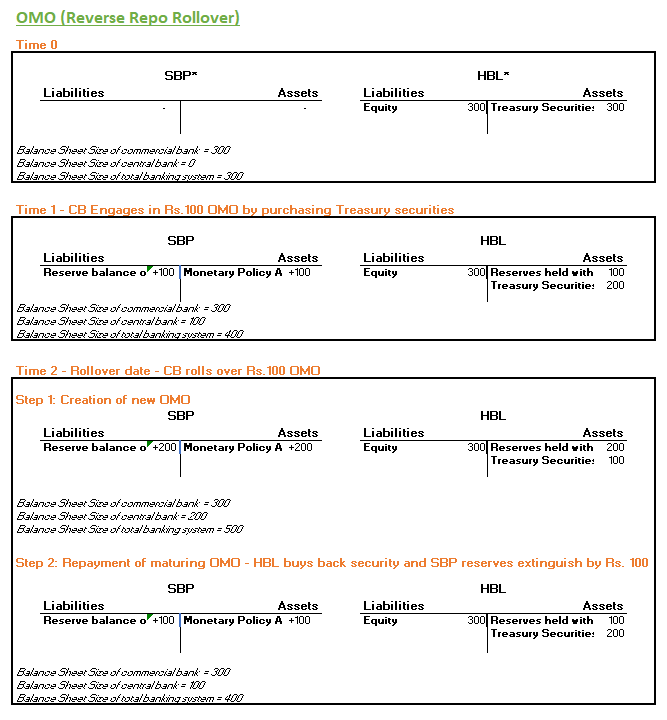

I wrote a piece for The Profit on the recent Open Market Operations (OMOs) of SBP (you can visit the page by clicking on the image below). The thesis of the piece was that despite SBP and the press calling the recent 63-day reverse repos as injections, they weren’t injections in the truest sense of the word as no new reserves were created by SBP. They were maturity transformations, i.e., maturing 7-day reverse repos were converted into 63-day reverse repos. 1

Three 63-day reverse repos were carried out till December 31. The media covered them excitedly using terms such as unprecedented. On January 7, SBP carried out another 63-day reverse repo, the 4th one in a row. The 4th OMO was such a non-event that none of the newspapers covered it. Words like “unprecedented” and “first time in the history of the nation” lose their meaning if liquidity injection by way of 63-day reverse repo has become a habit. Personally, I would have preferred the over-the-top statement such as “SBP has become addicted to 63-day reverse repo”, but that would be overdoing it. Plus it would have been followed by a rebuttal/clarification from SBP as “any student of monetary economics would know….”

My guess for the non-coverage of the Jan 7 OMO is that novelty has died and the size of the reverse repo isn’t large anymore. I explained in The Profit article that as more of the reverse repos are rolled over into 63-day maturities, the amount of 7-day reverse repos coming up for rollover becomes small. Small OMO isn’t breaking news stuff.

But what is interesting about the January 7 OMO, in contrast to the previous three 7 day OMOs, was that an actual injection took place. On Dec 31, Rs.330 billion of 7-day reverse repo was carried out. Based on the previous three OMO patterns, on January 7, SBP would have rolled over part of the maturing reverse repos to 7-day and the remaining transformed into 63-day. However, SBP rolled over almost all the 7-day (Rs.320 billion) and, in addition, injected fresh liquidity of Rs.424 billion in the 63-day reverse repo.

Consequently, the balance sheet size of SBP which hadn’t increased in the last three OMOs will increase by approximately Rs.350 billion after this repo. (I will update the below table with the actual number once SBP’s Statement of Affairs for January 7 becomes available).

Another thing to notice is that through these four OMOs, SBP has converted all its outstanding balance of 7-day repos as of Dec 10, 2021, into 63-day reverse repos by Jan 7, 2022 (see the yellow highlighted cells in the first table).

Four interesting things to look forward to

January 12, T-bill auction: To see if this unconventional and unorthodox policy of SBP results in lower 3M T-bill yields. Does it have any effect on the 6M and 1Y yields? SBP is providing 2-month money at 9.9%. What’re the spreads banks making on this?

Jan 14 and Jan 21 OMOs: Does SBP continue to add to the pool of 63-day OMOs by either transforming the maturing 7-day reverse repos or injecting new 63-day repos? Does SBP expand its balance sheet, or keep it the same, or shrink it?

Jan 26, T-Bill Auction: Based on what SBP does on Jan 14 and Jan 21 OMOs, we will find out if the 3M rates remain subdued or start rising as the market again wants its pound of flesh.

Feb 18, OMO: What SBP does to the maturing 63-day OMO: let it mature, roll it over into 7-day or roll it over into another 63-day OMO?

SBP has Rs.1.8 trillion of T-Bill auction target before Feb 18 and Rs.2.6 trillion auction target afterward till March 22.

Unless SBP reverts to conventional policy, these monetary policy actions will continue to provide considerable entertainment.

FOOTNOTES

Technically, rollover is a liquidity injection if you follow the chain. On the rollover date, SBP first creates new reserves i.e., injection by carrying out an OMO (see step 1 below on rollover date. CB reserves and the balance sheet size of the banking system increase on that date). Immediately, the reserves created from the new OMO are used to pay down the maturing OMO (step 2). The net effect is that the central bank reserves, as well as the balance sheet size of the banking system, do not increase between Time 1 and Time 2. That is why I was saying that on a net basis, these rollovers aren’t an injection.

(Click on the image to enlarge)