Sovereignty lies with IMF

Sovereignty lies with IMF

When the IMF asks SBP's monetary policy committee (MPC) to jump, the tendency of MPC is to ask how high.

I am supposedly on a social media break and hence haven’t been able to tweet my thoughts on the latest monetary policy development. As the information arrived in bits and pieces over WhatsApp, I noted some thoughts. Here they are.

The post may be clipped if you are receiving it over email. Please click on the title above to read it on substack.

Wherein lies Sovereignty?

I have been raised on a healthy dose Mutal'a Pakistan (Pakistan Studies). I had to memorize Objective Resolution, which forms the preamble of Pakistan's constitution and starts as

Sovereignty over the entire Universe belongs to Allah Almighty alone...

In 2003, I visited Turkey with my friends on a shoestring budget (Lonely Planet's "XYZ on a shoestring" was still a popular publication at the time). I visited a museum, don't remember exactly where, could be next to Anit Kabir in Ankara, showing the evolution of constitutional reforms in Turkey. It was mentioned there that in Republic of Turkey,

Sovereignty unconditionally belongs to the People

Wikipedia states this is the founding principle of the Republic of Turkey and is written on the wall behind the chairman of the General Assembly Hall in the Grand National Assembly.

When I read the principle the first time in that museum, the young and naive me was shocked at this "blasphemy".

Now that I know better, I believe we need to introduce a preamble for the SBP Amendment Act which should start as

Sovereignity over SBP belongs to SBP (read IMF)

Shaukat Tarin outlines five actions demanded by IMF

Adviser to the Prime Minister on Finance Shaukat Tarin has said Pakistan will have to complete about five “prior actions” before the International Monetary Fund (IMF) calls a meeting of its board of directors to approve revival of its $6 billion Extended Fund Facility suspended in April this year.

The sources said Mr Tarin had been able to convince the IMF staff to significantly alter the SBP amendment bill that former finance minister Dr Hafeez Shaikh and SBP Governor Dr Reza Baqir had committed to the IMF ahead of $500 million disbursements in March this year.

When the SBP Amendment Act initially made the news due to leaks over WhatsApp, the Ministry of Finance and SBP engaged in gaslighting. Economists and columnists spilled a lot of ink writing op-eds and tweeting why the independence of SBP is paramount. I have no objection to granting autonomy to SBP, however, no one bothered to ask who is drafting this amendment bill to provide autonomy to SBP. Is it a private member bill or is it presented by one of the standing committees of the parliament? Has it been discussed?

In the subsequent press conferences by SBP / MoF, we were also told that the draft of the bill can't be shared or discussed with hoi polloi till it has been presented in the parliament.

Yet the bill has been shown to IMF, or more realistically speaking, prepared by IMF to be rubberstamped through parliament. The bill has already been rubber-stamped by the federal cabinet without reading.

The federal cabinet approved the SBP Bill on March 9, 2021 but without reading it.

Constitutional Violation

If the new act violates the constitution, (it may very well be a negotiating tactic on part of GoP) it raises questions about who drafted the bill and where does the sovereignty lie.

Sovereignty

Sections of SBP amendment bill violate constitution, says Farogh Naseem

While briefing the International Monetary Fund officials via video link on Monday, he said the provision provides that the central bank would be consulted on any proposed legislation relatable to the SBP.

The legislative power has been conferred by the Constitution on the parliament, and the Constitution does not provide for any consultation with the SBP prior to passing of any legislation, he explained, adding the proposed section introduced a stipulation which was ultra vires of the Constitution.

The legislative power has been conferred by the Constitution on the parliament, and the Constitution does not provide for any consultation with the SBP prior to passing of any legislation, he explained, adding the proposed section introduced a stipulation which was ultra vires of the Constitution.

It appears that sovereignty doesn't lie with the people or parliament. It lies with SBP.

Immunity and equality

Likewise under the proposed Section 15(1), the governor, deputy governors, or any non-executive directors or external members of the Monetary Policy Committee cannot be removed on the grounds of misconduct unless a court of law first determines that serious misconduct has been committed, he said.

This provision is unconstitutional as it violates the equality clause contained in Article 25 (equality of Citizens) of the constitution, which, inter alia, provides for equal treatment. Even the judges of superior courts can be proceeded against under Article 209 for misconduct, without there being a prior requirement of a declaration from a court of law that the judge has committed misconduct.

Right to speak in parliament

Besides, the proposed Section 46B(5) provides that the SBP shall “interact and communicate” with the parliament when the words “interact and communicate” essentially connote the right to speak.

Article 57 of the Constitution provides that the prime minister, a federal minister, a minister of state and the attorney general shall have the right to speak and otherwise take part in the proceedings in the parliament. This categorically means that SBP or its functionaries cannot interact and communicate with the parliament, the minister said.

The SBP falling under the ministry of finance, will have to interact and communicate with the parliament through the finance minister. Therefore, the proposed insertion i.e. Section 46B(5) would be hit by Article 57 of the Constitution, he said.

Thus we see that under the new Act, SBP would essentially be a sovereign entity such that parliament cannot pass legislation affecting SBP unless SBP agrees with it, SBP senior management cannot be removed for misconduct unless the court agrees that there has been misconduct and SBP has the right to speak to the parliament bypassing Ministry of Finance as required under the constitution.

This is being pushed by IMF and has already been rubber-stamped by the cabinet.

Under the new act sovereignity lies with SBP, and as top management is steeped in IMF dogma, it follows that when it comes to SBP, sovereignity lies with IMF.

Apologies for the above digression. I know you wanted to know what I think of the latest SBP's Monetary Policy Committee (MPC) decision to increase the policy rate by 150bps. Without further ado.

Whither "forward guidance"

The MPC decision speaks volumes about SBP's non-existent forward guidance (praised to the sky on Twitter and press when SBP’s forward guidance policy was initially announced) that the entire market was surprised rather shocked at 150bps rate increase.

This unexpected decision was taken on the back of another unprofessional decision on part of SBP to "prepone" its monetary policy meeting by one week.

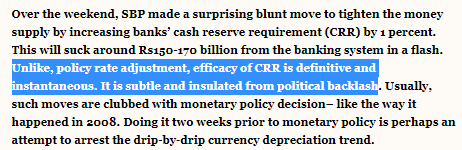

It is amusing that his preponement was coming after the unexpected increase in CRR a week ago which was supposed to be definitive, instantaneous, subtle, and insulated from the political backlash of the policy rate change.

The CRR change was following the imposition of 100% cash margin on imports of certain items that comprise less than 2% of Pakistan's import bill.

To summarize, SBP hopes to control current account deficit by imposing a 100% cash margin on items that comprise less than 2% of import bill. In terms of value, 25% of the items on the list comprise essential food items. Another 15% by value are such items as imported tiles, ceramics, kitchen electronics that would be a consequence of GoP’s construction amnesty and SBP’s push for construction financing and may not be affected by the cash margin at all as the end users are immune to such minor inconveniences as 100% cash margin. The rest is rubber, chemicals, paper etc. While dengue is prevalent, SBP feels that imposing a 100% cash margin on mosquito coils that comprise 0.02% of Pakistan’s import bill is beneficial.

Makes you wonder if some local insecticide maker had lobbied SBP to include the mosquito coil in that list.

The absurd thing about preponing the MPC meeting by one week was that a T-bill auction was supposed to be held between the announcement of the preponement and the preponed MPC.

Nov 16: SBP announced that the next MPC will be held on Nov 19 instead of Nov 26

Nov 18: SBP T-Bill auction

Nov 19: Preponed MPC was held

Unsurprisingly, the banks didn't make competitive bids in Nov 18 auction with the result that the government raised less than 10% of the auction target.

Govt raises Rs56bn against Rs600bn target

The government rejected almost all competitive bids in the auction of treasury bills held on Wednesday while it accepted only Rs0.5 billion for three-month tenor.

However, the government raised Rs55.258bn through non-competitive bids for three-month making the total as Rs55.8bn. The cut-off yield remained unchanged at 8.5 per cent.

BR Research says its best. (emphasis mine)

The monetary policy decision is today. The committee meeting has been preponed by a week in light of recent developments in the currency movement. Gauging from the press release, SBP’s forward guidance stance of being accommodative could very well change due to recent “unforeseen” events. This may rule out a measured expected increase of 0-50 bps. In fact, expect more.

The question is: what are the unforeseen developments that could not have waited for (even) a week. Certainly, inflation outlook is changing, and SBP will likely revise up its inflation forecast from 7-9 percent. Its forward guidance would be hinged upon new forecast and expectations. But this alone cannot be the reason to prepone the review.

There are no visible uncertainties due to monetary policy in the capital market (both money and stock) to pressurize SBP to call the meeting earlier. The secondary market yields in the money market have already moved up by 100-125 bps over the last policy rate change and any change in the policy rate (up to 100-125 bps) is already priced in.

And there is no primary auction in the next week which could have enticed SBP to call the meeting earlier. In fact, day before yesterday, a T-bill action took place and almost all market (competitive) bids were rejected. Had the SBP not announced policy review earlier, there could have been some interest in 3M papers. The government accepted mere Rs500 million in the 3M paper at the previous auction’s cut-off yield. The government was lucky to get Rs55 billion in non-competitive bids in 3M. Government got nothing in the 6M and 12M papers.

This argument is supported by a recent blunt and surprised decision of increasing the CRR rate by 1 percent to 6 percent (on average) and minimum of 4 percent (from 3%). Usually, such decisions are clubbed with monetary policy. Doing it in advance is perhaps to arrest the falling currency trend. It did work marginally. However, it seems SBP probably wants to send a clearer message through monetary policy communication without waiting another week.

CRR increase is supposed to reduce the growth in the real money supply – to curb the demand which is putting pressure on imports and overall current account deficit. The decision of possible higher hike in the policy rate is meant to curb the demand as well, and do inflation targeting in a better way. But as described earlier, market rates are already up by 100-125 bps from the previous policy rate and so is KIBOR. The tightening impact on demand through reduced private credit is already happening. Plus, SBP has already put curbs on consumer finance (through restrictions on auto loans).

Seeing all that, there seems to be no other reason, but to arrest the falling currency trend by calling the meeting earlier. One other reason, as per conspiracy theorists is that it’s an IMF pre-condition to increase the policy rate earlier.

SBP is throwing everything "including" the kitchen sink at a non-monetary problem

Steps by SBP so far,

Changing Prudential Regulation (Sep 23) to clamp down on car financing and personal financing.

Surprise imposition of 100% cash margin on the import of goods that comprise less than 2% of import bill.

Unexpected increase in CRR by 1%

Preponing the MPC meeting by one week when there was no reason to do so as there is no auction happening between Nov 19 and Nov 26.

Increasing policy rate by 150bps when the market was expecting a 50-75bps increase.

Increase the number of MPC meetings from 6 to 8 citing "international best practices" further adding to the uncertainty.

This is being done to arrest the depreciation in the rupee. Ironic, considering that a few days ago SBP governor had stated in Manchester that rupee depreciation is beneficial to a segment of society and we shouldn’t begrudge them.

Conspiracy Theory

The aforementioned BR editorial while on the one hand wonders why the MPC meeting was preponed by a week when there wasn’t any reason for it and, on the other hand, says that those rightfully calling it a result of an IMF pre-condition are conspiracy theorists. But are they really conspiracy theorists when on Sunday, November 21, immediately after the policy rate increase of Friday, Nov 19th, IMF publishes the Staff Statement?

I don't know about you but I am firmly in the camp of conspiracy theorists.

Whither data-driven approach

Earlier SBP pretended to use a data-driven approach to justify its actions by citing credit metrics and output gap (without releasing any data etc of how the output gap is calculated).

The recent 150bps increase considering that it is following the increase in cash margin on imports and 1% increase in CRR has no data justifying it. Aap ka bhai to kehta hi rehta hai but Anjum Ibrahim in BR has been asking for a long time where is the SBP research that shows changing the policy rate affects inflation.

Let me again quote from BR's recent editorial (emphasis mine). This is a long editorial so please bear with me.

Monetary Policy Statement - Editorials - Business Recorder

Critics of the monetary policy decisions during the ongoing International Monetary Fund (IMF) programme have **consistently accused the SBP and the MPC of following the Fund’s dictates without providing an appropriate in-house context (including the fact that before May 2019 the discount rate was linked to core inflation as opposed to the Consumer Price Index)**. It is important to note that the market perception was that the rate would be raised from between 75 and 100 basis points in view of the raise of 1 percent in CRR (cash reserve ratio) just a week earlier, and the rise of 150 basis points, they argue, reflects the tendency of the MPC to ask how high when the Fund says jump.

Wow!!! Color me impressed BR! I didn't know that this is what the market participants think. Let me quote it again.

the tendency of the MPC to ask how high when the IMF says jump.

If this is the perception and BR tends to agree here (I think), SBP needs to work on its credibility if the impression has shifted from SBP being a tool of Ishaq Dar to a tool of IMF.

The editorial goes on to say

1. MPS is stretching the truth.

the MPS argues that “inflation is not only due to across the world Covid-induced disruptions to supply chains and higher energy prices but emerging signs of demand side pressures on inflation and inflation expectations of businesses have risen on account of further upside risks from domestic administered prices. The burden of adjusting to these external pressures has largely fallen on the rupee.” Administered prices are a reference to the IMF (International Monetary Fund) condition to raise base electricity tariffs (implemented last month), and to meet the budgeted petroleum levy target of 610 billion rupees (not yet implemented as only around 23 billion rupees has so far been collected under this head); however, the claim that the burden of adjusting to external pressures has largely fallen on the rupee is stretching the truth because the rupee is also burdened by two other factors: (i) Pakistan’s inflation rate is higher than those of other regional countries (India under 5 percent, Bangladesh 6.4 percent and Sri Lanka 7.6 percent last month) as well as our trading partners (the EU 4.1 percent and the US 5.1 percent); and (ii) Pakistan’s higher interest rates vis-a-vis the rest of the world are not attracting foreign investment or portfolio investment (negative 948 million dollars in the first quarter of this year against plus 179 million dollars in the comparable period of last year) because of not only the stalled sixth review but also the massive rise in public debt with net incurrence of liabilities, as a component of current account, rising to 4.521 billion dollars in the first quarter of Fiscal Year 2022 as opposed to 4.104 million dollars during the entire 2021 fiscal year.

2. MPS is relying on unreliable agriculture data to offset the impact of the slowdown in industrial growth

perhaps to assuage the supporters of higher growth rate within the government, the MPS states that the reduction in industrial output would be more than offset by the improved outlook for agriculture that would mitigate the risks of adverse impact on the growth forecast of 4-5 percent in FY22. The SBP needs reminding of a recent report published by this newspaper in which a senior official of the Ministry of National Food Security and Research has been quoted as saying that not only is it too early to project whether production targets for wheat, sugarcane, maize and other products would be achieved as data is not yet available but also that the country is unlikely to achieve the 3.5 percent projected growth target set for the current year after revising the cotton output target from 10.5 million bales to 8.46 million bales.

3. Increase in the interest rate will fuel inflation

And finally, the MPS notes that the “real money supply growth has accelerated in recent months...with economic recovery on a sound footing, there is a need to pare back this growth...the recent rise in banks’ cash reserve requirements would help in this regard.” Domestic borrowing largely through issuance of Pakistan Investment Bonds to fund the over a trillion rupee rise in outlay in the current year compared to the year before at a higher rate now would fuel not reduce inflation.

There you have it. SBP has increased the policy rates on IMF dictates and as per BR editorial, SBP is justifying the increase using unreliable statistics and there is a likelihood that a higher policy rate will fuel inflation by increasing the cost of GoP borrowing.

Ideology, Not Economics

We have talked a lot in this substack that how the monetary policy as applied in Pakistan and later justified by economists in opeds and tweets is ideological. On the one hand, we continue to push the narrative that inflation is cost-push inflation caused by mafias, international commodity prices, increase in prices of fuel and electricity as demanded by IMF, and structural problems in the economy. On the other hand, we support the central bank fighting it by increasing the policy rate because in Econ101 we were taught that when inflation increases, the central bank should increase the interest rate to fight it.

One of the weaker arguments in support of increasing the interest rate is that it will increase the cost of borrowing of the federal government forcing it to pay more interest and leaving little fiscal space for the government to make expenditures. Thus, the suggested solution isn’t to put brakes on the fiscal spending but rather line the pockets of banks (who have two-thirds to three-quarters of all their assets invested in government bonds) with interest income from government borrowings.

On a related note, Michael Pettis is talking about tax cut here (bonus points if you can also relate this to Art Laffer meeting Ministry of Finance recently) but this also holds for our monetary policy committee members and IMF

The same is happening in Pakistan. Monetary policy steps that are being taken are based on ideology, and that too, a defunct one.

I love this paragraph in an article by James Galbraith published two days ago. The article is about the US Federal Reserve.

Whipping Up America's Inflation Bogeyman by James K. Galbraith - Project Syndicate (project-syndicate.org)

Furman goes on to insist that “it’s the Fed’s job to keep [inflation] under control.” That also is not true. The US Federal Reserve operates under the Full Employment and Balanced Growth Act of 1978, which stipulates that full employment and reasonably stable prices are goals for the US government as a whole.

The drafters of that law – I was among them – did not buy the dogma that inflation “is always and everywhere a monetary phenomenon,” as Milton Friedman had argued. Rather, we believed, and the law states, that all of the economic objectives had to be pursued with all of the available tools, and by all of the agencies.

What I find interesting above is that economists and lawmakers were involved in drafting the Federal Reserve law. This brings me back to the original question that I asked

Do we know who was involved in drafting the SBP Amendment Act that is rubber stamped by the federal cabinet, pushed by IMF and will be rushed through the parliament?

And since economics and monetary policy touches all corners of the economy, why isn't the new SBP Act being discussed anywhere? Why is it that all the opeds are about justifying what has already been included in the act? When it was rightly pointed out by me that the new SBP Act doesn’t allow for refinancing, how could MoF and SBP blatantly lie about it without any repercussions?

Galbraith goes on to add

More to the point, none of America’s price problems would be helped by higher interest rates. Tighter credit would get in the way of the business investment that the US economy needs to expand capacity and keep costs down. Interest is a cost, and therefore will get passed on to consumers.

Similary, in Pakistan, private sector borrowing is a small component and SBP already cracked down on consumer financing on September 23, 2021 stating

This targeted step will help to moderate demand growth in the economy, leading to slower import growth and thus supporting the balance-of-payments. The changes in the PRs effectively prohibit financing for imported vehicles, and tighten regulatory requirements for financing of domestically manufactured/ assembled vehicles of more than 1000 cc engine capacity and other Consumer Finance facilities like personal loans and credit cards.

And yet inflation isn’t slowing. SBP should realize that may be, just may be, inflation isn't a monetary phenomenon here.

For those who can afford Audi e tron, which I presume along with other vehicles is affecting the current account deficit, they arent affected by these measures.

On the other hand, we have this statement by Pakistan Business Council

Policy rate hike to slow economy

“Consumer products make up nearly 8% of imports while 1% share is occupied by vehicles (ready to drive),” Pakistan Business Council (PBC) CEO Ehsan Malik said while talking to The Express Tribune. “Curbing them to some extent may not directly hurt economic activities in the country.”

The remaining 91% of imports consist of industrial machinery, petroleum products, industrial and agricultural inputs (raw material) and food items (like wheat, sugar and cooking oil). Making them expensive and monetary tightening will definitely hit investment activities in industries.

This would, in turn, make exports expensive and uncompetitive as well as contribute to food inflation, he said.

According to him, nearly two-thirds of the surge in import bill during the current fiscal year to date (July-October) came in the wake of rise in global prices of commodities, which Pakistan imports to meet its domestic requirement.

Coming back to James Galbraith, he ends his piece with

Back in the 1970s, the leading voice on economics in Congress was my boss, the chairman of the House Banking Committee, Henry Reuss of Wisconsin. He liked to say that we need a “rifle-shot” anti-inflation policy, not a “blunderbuss.” The focus should be on stabilizing energy prices, cracking down on speculators, cutting the Pentagon budget, unclogging the ports, and ensuring that sorely needed wage increases go mainly to the lowest-paid workers.

What most certainly should not be done is to turn a manageable problem into a big crisis by handing it off to the Fed.

And yet this is exactly what we are doing:

Trying to solve a problem, which isn’t monetary in nature, with monetary tools regardless of the other repercussions of that decision, if any.

If I were to summarize this post,

SBP is trying to use monetary tools to solve problems that are fiscal and structural in nature and failing at it.

Not that anyone cares but SBP has sacrificed its credibility of forward guidance by sudden moves such as suddent changes in Prudential regulations, 100% cash margins, increase in CRR, preponing MPC and increasing the frequency of MPC and finally increasing the policy rate by 150bps when market expected the rate increase to be in the range of 50-75bps trying to solve a problem which isn't monetary in nature.

No more data driven approach. Data to be cherry-picked to justify the decision that has already decided to be taken.

Last but not least, sovereignty lies with IMF. The below tweet speaks volumes about how low we have fallen that below isn’t scandalous at all.

Lest it is misconstrued, I am not stating here that IMF has ill intentions. Rather SBP Act is a piece of legislation that is drafted and being pushed by IMF and accepted by us without any debate.

While there is a dual mandate for Federal Reserve as Galbraith stated above, IMF is pushing for inflation targeting for SBP regardless of economic growth or whether inflation is monetary phenomenon at all. The Act I presumed will be a long lived one and affect everyone for a long time to come and yet it will be pushed through the parliament without any discussion or debate. Need I say more about wherein sovereignty lies.

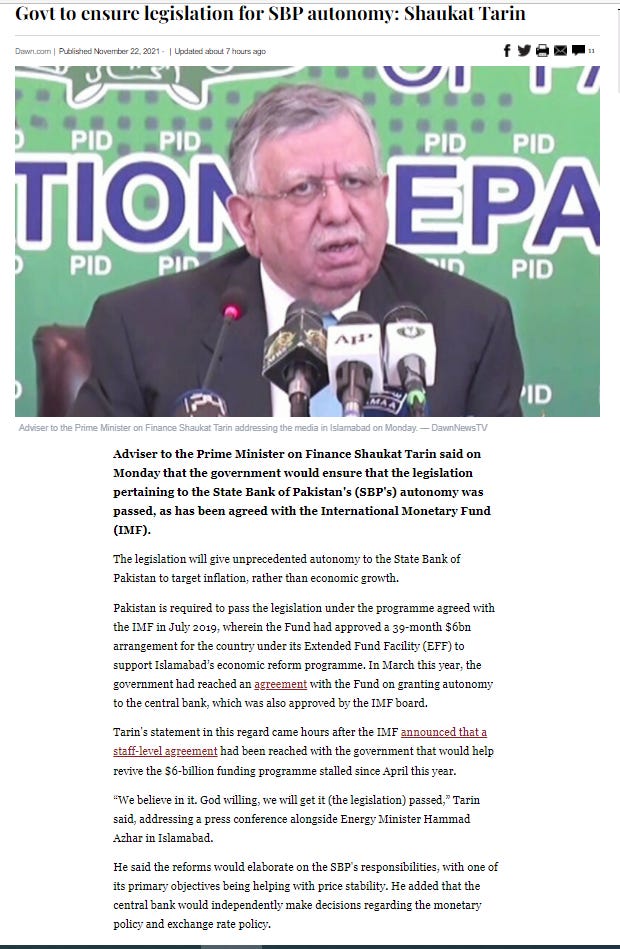

Govt to ensure legislation for SBP autonomy: Shaukat Tarin - Pakistan - DAWN.COM

Rate Hike, Masses Rise

In the end, I leave you with this.

I just hope that the masses don’t drown when the rates are decreased.